Covered bond Investors - Navigating wide spreads VS swaps against higher public sector deficits

INTRODUCTION

After issuers focussed on unsecured supply early in 2025, covered bond issuance almost caught up with 2024 by end H1 producing a fourth year running with net positive supply. While covered bonds have at times been tight vs SSA sectors this year, interest in the asset class has remained high from a broad range of investors. While many of the 2023 and 2024 newcomers from credit space have been monitoring rather than buying in size this year, it has been central bank / official institutions out to 5Y as well as insurance / pension fund buyers at the long end who have become more active than in 2025.

While analysing the evolution of primary market distribution statistics is crucial to get an idea about high level shifts in demand, they only tell some of the story. Hence, as last year, we have decided to run a broader investor survey that allows us to go into more detail and to give you as complete a picture of the covered bond buyer base and their preferences as possible. After all, covered bond investors are looking at wide spreads vs swaps on the one hand but at the same time, they are faced with more public sector supply. And while discussions around de-dollarisation or a shift away from US Treasuries might prove supportive for EUR as well as USD covered bonds, higher Bund supply and possible tighter Bund-ASW spreads would prove damaging to at least covered bond spreads vs swaps. In other words, we’re living through volatile times and are looking at a number of potential structural breaks. And as covered bonds have proven over the years, they are a really good place to hide, sit and wait.

OVERVIEW OF COVERED BOND INVESTOR BASE

The strong migration of investors into covered bond markets from previous years has not been reversed as the relative attractiveness compared to both rates products and corporate bonds has still been on investors’ minds. This was especially true for last three months of 2024.

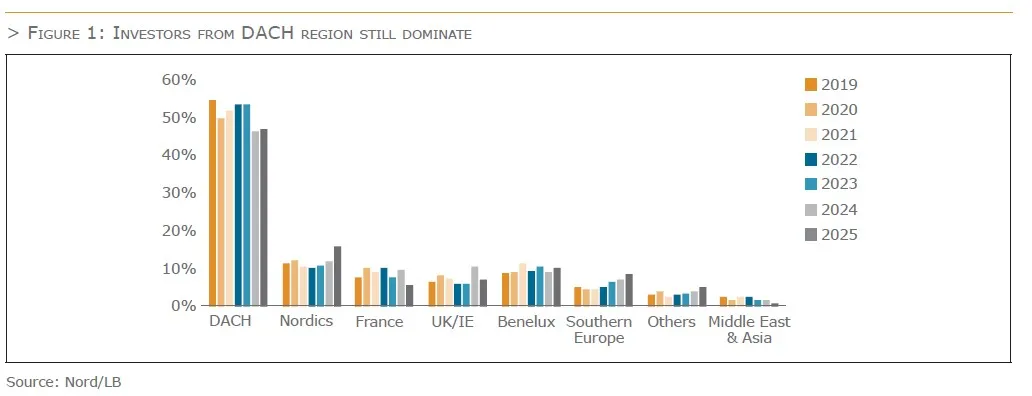

For the below, we again refer to the investor allocations of EUR benchmark primary market transactions, which are the largest segment in the covered bond universe. Especially early 2025, supply showed some weakness, which at least theoretically, gave issuers room to manoeuvre when allocating bonds. In terms of allocation by region, it is still obvious that the major share of the newly placed benchmarks goes to accounts in the DACH region (mainly Germany). As a matter of fact, the share of the DACH region has been up marginally. At 46.9% it is slightly above previous year’s figures (2024: 46.2%). In turn, growth was particularly evident in the Nordics (15.9% after 12.0% in 2024). Benelux and Southern Europe regions have been also on the rise, whereas UK and France Investors have had a smaller share so far in 2025. Having said that, it should also be borne in mind that, due to the pronounced home bias in covered bonds, a higher issue volume in individual countries also “benefits” the allocation.

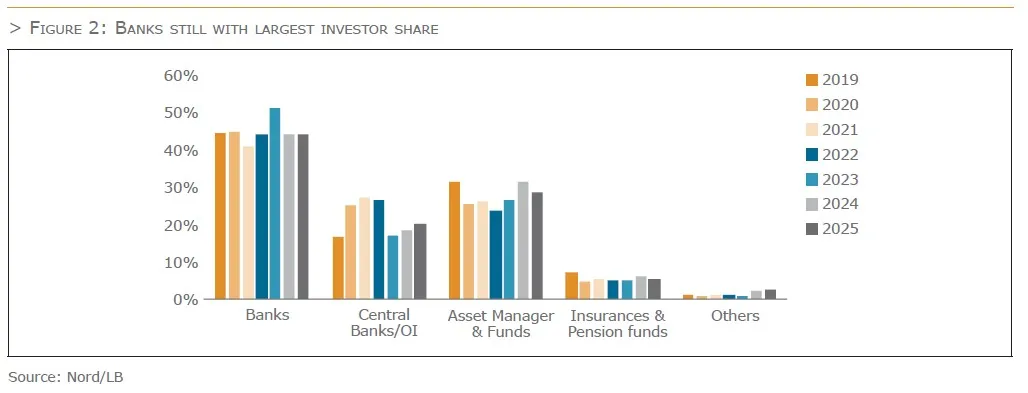

Regarding the distribution by investor type, the “Central Banks & Official Institutions” category dropped between 2022 and 2023 due to the end of the CBPP 3 (offset by more “Banks”). Their share did hold steady in 2024, though and moved up marginally in 2025. “Banks” have maintained the largest share so far this year (i.e. 44.6%) making them the most important group of buyers of covered bonds in the EUR benchmark segment. The categories “Asset Managers & Funds” as well as “Insurance & Pension Funds” come in a bit weaker in the year to date view. The real money investors have a combined share of 34.1%.

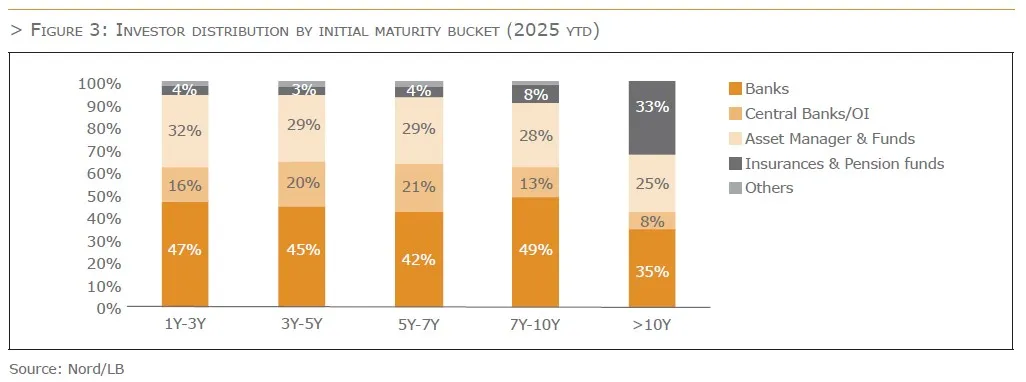

The picture by “tenor” has also not changed recently. It is relevant to emphasize the supply side again, because issuers’ interest for longer term funding has not dramatically changed in recent months with the bulk of supply coming in the belly of the curve. Still, for tenors out to 10Y, banks dominate the investor statistics across maturity buckets. However, in the >10y bucket, “Insurance and Pension Funds” have really picked up the pace driven by higher yields. They have doubled their share over the past three years to a level just above 30% and hence more or less on par with bank treasuries.

INVESTOR SURVEY

To get systematic feedback on a number of topics, we conducted an online investor survey in the second half of June. We received responses from 33 covered bond investors covering a broad range of investor types and regions. The questions focussed on (1) investors’ level of activity and motivation in covered bond markets, (2) their main concerns, (3) third country equivalence and (4) what role ESG plays in their day to day covered bond investments.

Activity levels

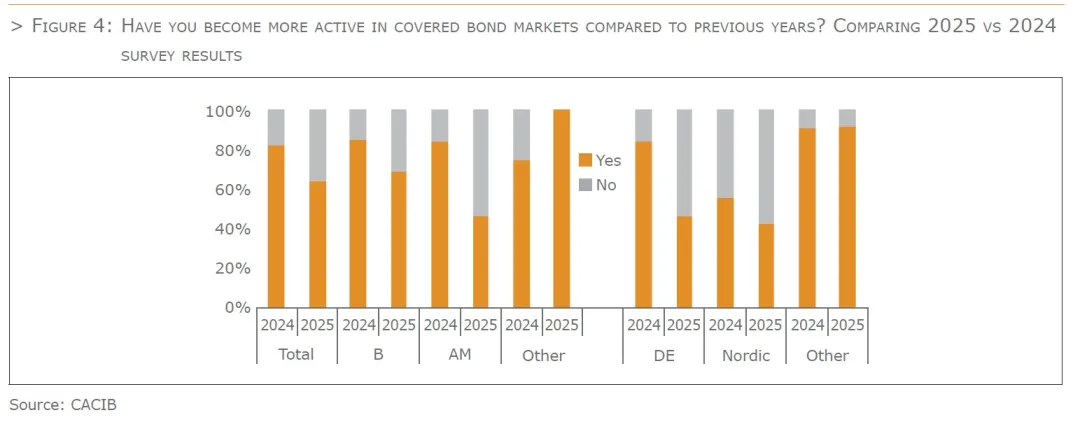

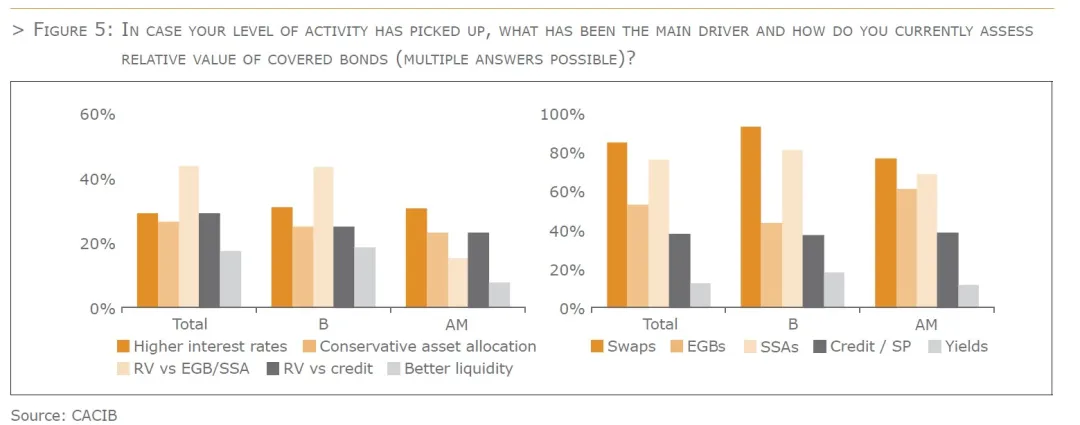

Investors have been increasing their exposure to covered bonds since 2022, first bank treasuries and just as they began to slow down into H2 2023 and again in 2024, we saw asset management buying pick up. With 2025 being the fourth year with net positive supply and valuations vs EGBs and SSAs tighter than in previous years, it is no wonder that investors are slowly starting to get to activity levels in covered bond markets that they feel comfortable with. In last year’s survey, almost 80% of all investors we surveyed stated they were still building up exposure. This number has dropped to 65% in this year’s edition. The drop has been especially pronounced on the asset management side where only half still see higher activity levels. In turn, central bank / official institutions as well as insurance / pension fund buyers are still reporting more activity than last year. While many of the investors, who have become more active, have focused on primary markets, around half have also focussed on buying in secondary markets as well (similar to last year’s survey results).

The drivers for investors’ interest in the asset class has above all been relative value vs EGBs and SSAs. In times of tightening Bund-ASW spreads, covered bonds tend to outperform sovereign bonds and this has drawn interest from investors (44%). Higher yields have played a similar role to attractive RV vs credit and a more conservative asset allocation (29%). Those investors who have slowed down slightly have mostly mentioned an increased allocation to EGBs and SSAs (35%) as well as expected covered bond spread widening vs swaps (12%).

Last but not least, with so many different investors active in covered bond markets these days, we wanted to get a feel for the most relevant benchmarks or ways to assess relative value. The most common angle still is valuations against swaps as well as SSAs, the classic approach taken by bank treasuries. Amongst asset managers, valuations against EGBs are relevant too, and especially for aggregate portfolio managers, this angle does make sense. While outright yields are relevant for insurance and some bank treasury buyers, the answer did not have any relevance in our survey.

Concerns

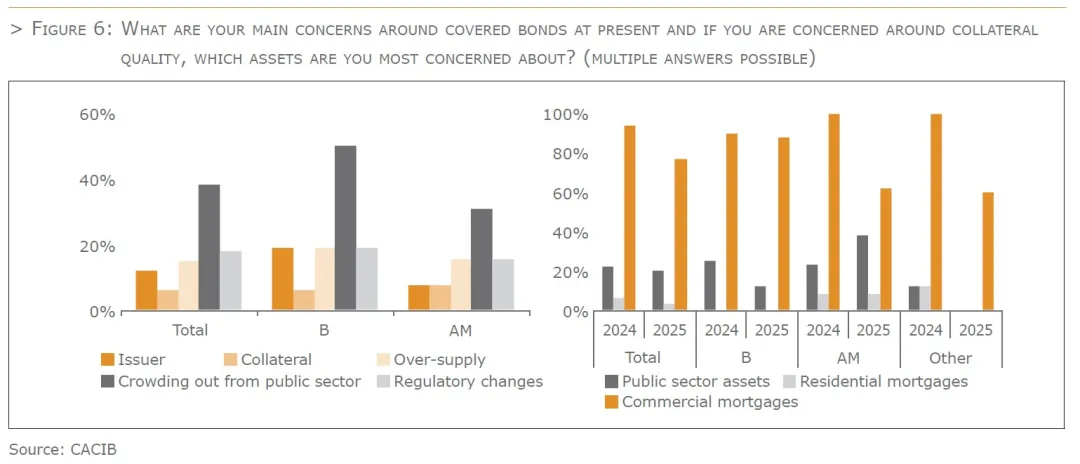

Looking at the world today, there are plenty of potential concerns that even investors in a high quality asset class such as covered bonds cannot fully ignore. The responses in our survey actually highlight both the volatile world as well as the stability of the covered bond asset class. Less than 20% see issuer quality as a concern and even less are concerned with collateral quality. The main concern, especially for bank treasuries is for covered bonds to be crowded out by public sector supply spiking on the back of additional infrastructure and military expenditures in the coming years. At the same time, slightly more than half of the investors we surveyed expect structurally tighter covered bond – sovereign bond spreads because of this potential increase in public sector supply.

If we do zoom in on cover pool quality, of course, commercial real estate assets are still seen as the main source of concern. However, amongst the asset managers we surveyed, concerns have receded with only around half still mentioning CRE. At the same time, their concerns around public sector assets are growing slowly. Across all of our responses, public sector assets are not yet a concern, though.

Third country covered bond equivalence

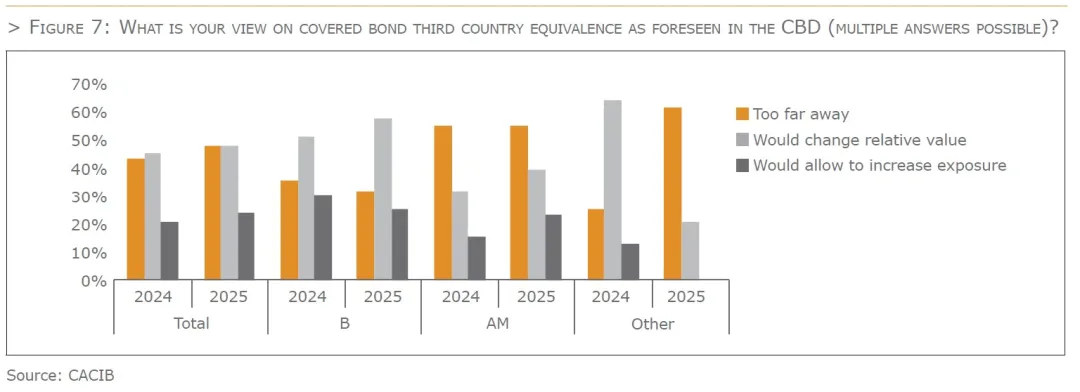

With the Covered Bond Directive (CBD) implementation a few years behind us, the focus on the regulatory side has clearly been on third country covered bond equivalence, not only since the shock announcements and then pausing of proposed rules by the UK PRA. Similar to last year responses show that third country covered bonds getting better regulatory treatment would change the way investors look at relative value. If banks can work with lower risk weights or LCR haircuts, the costs of carrying a position drops and so does the required spread. Even for asset managers this is true to some extent despite them only being indirectly impacted. For around half of the respondents in our survey (up marginally from last year), third country covered bond regime is still too far away to be relevant today.

ESG

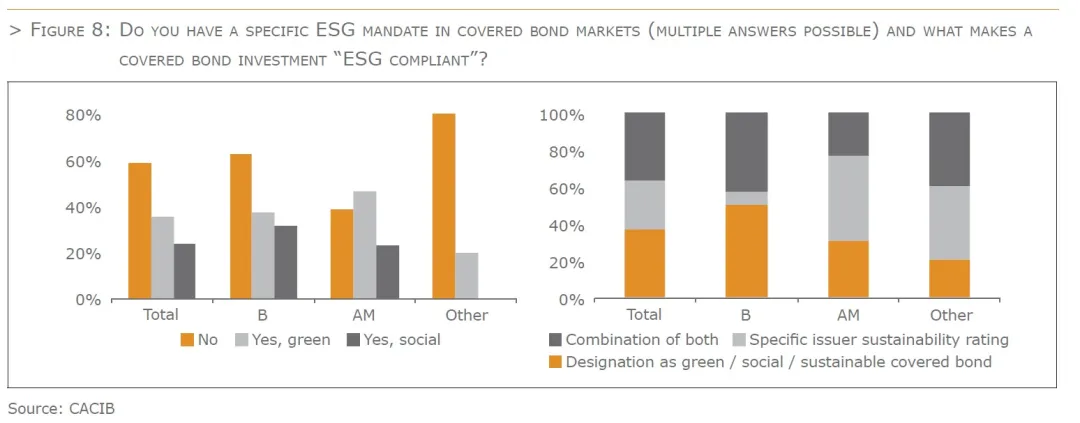

While covered bond issuance in green, social or sustainable format has been growing in recent years, it still only represents a small share in overall volumes. Often, the availability of data on the ESG credentials of balance sheet assets has been a constraining factor. With spread differentials between ESG and conventional covered bonds negligible, banks have also often chosen to use these assets for senior preferred, non-preferred or even tier 2 issuance rather than covered bonds.

The fact that we are still talking about an evolving market has led to different approaches to ESG across covered bond investors. Less than 40% of respondents state that they have a specific ESG mandate also covering covered bonds with the green angle more prominent than social, especially amongst asset managers. The diverse nature of our survey responses also continued with respect to our question what makes a covered bond investment “ESG compliant”. The designation as green / social covered bond by the issuer is good enough for just below 40% of the respondents while two third look at specific issuer sustainability ratings or a combination of both.

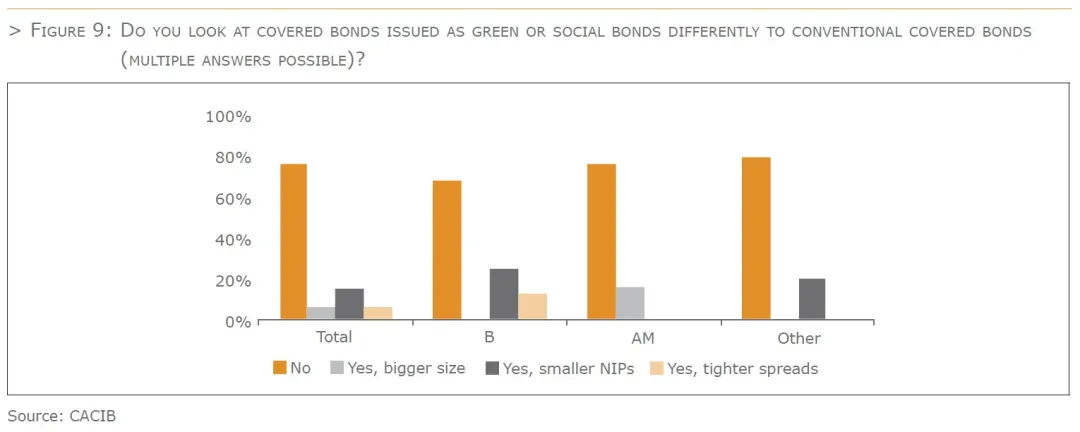

Last but not least, investors we surveyed do not make a difference between ESG and conventional covered bonds when it comes to assessing relative value. Looking at data from primary markets, ESG covered bonds have tended to have stronger order books and slightly smaller new issue premiums. However, they have often failed to trade at materially tighter spreads vs conventional ones. The survey results reflect this as well as around 75% of respondents (unchanged from last year’s survey) do not look at ESG covered bonds differently. A mere 15% accept smaller NIPs but less than 10% would buy in bigger size and / or accept tighter secondary market spreads.

1.6.1 The Attractiveness of Investments in Covered Bonds from a Bank Treasury Perspective

by Olaf Pimper, Commerzbank

Last July the European Banking Authority (EBA) has been tasked by the European Commission with, interalia, Investments in Covered Bonds have proven extremely valuable for banks in recent years, particularly concerning the fulfilment of regulatory requirements such as the Liquidity Coverage Ratio (LCR). Covered Bonds are recognized in Europe as high-quality liquid assets (HQLA). This classification makes them indispensable for banks aiming to efficiently manage their liquidity ratios, as they regularly provide higher credit spreads than other HQLA assets, especially government bonds, regions, supranationals, and agencies.

The regulatory foundations that ensure banks meet their liquidity requirements while strengthening the stability of the entire financial system are crucial. Covered Bonds are inherently low-risk, have high valuation certainty, display low volatility compared to riskier assets, and function as funding instruments even during times of severe stress. Covered Bonds successfully passed the litmus test last year when uncertainty about the US mortgage market arose again. Commercial real estate (CRE) markets were affected, and Covered Bond spreads from banks with exposure to the US CRE market initially widened massively. Unlike the early 2000s when the spread expansion practically knew no end, the confidence in Covered Bonds had grown so much that the affected banks’ Covered Bonds were bought. Additionally, the funding market functioned, enabling the return of the affected banks to the primary market in less than half a year.

A significant argument for the great trust in Covered Bonds is the transparency requirements stipulated in the European Covered Bond Directive (CBD). The requirements from Article 14 foster a high degree of market transparency. The Harmonized Transparency Template (HTT) developed by the European Covered Bond Council (ECBC) has established itself as the leading instrument to deliver CBD-required information to investors. Standardization of reports and provision of comparable information greatly facilitate the due

diligence process for investors.

Another cornerstone for bolstering trust in the asset class and easing due diligence was the introduction of the “European Covered Bond Premium.” This can be seen as a milestone in market regulation. The designation “European Covered Bond (premium)” acts as a quality seal, signalling that the Covered Bonds meet the stringent requirements of Article 129a of the Capital Requirements Regulation (CRR). The assessment is no longer the responsibility of the investor but is conducted by national regulators and published on their respective websites. This allows banks and investors to make well-informed decisions quickly, trusting in the quality of the underlying assets.

Currently, the European Banking Authority (EBA) is tasked by the European Commission to review the CBD. I believe that this directive can rightly be considered a European success model. Various countries outside the EU and Europe use dual recourse techniques, including dedicated legislation, cover pool administrators, transparency requirements, liquidity buffers, and many other safety mechanisms, to enable their banks to access affordable funding. Banks, in turn, can pass on these cost savings to their customers, allowing them to fulfil the dream of owning a home.

For Covered Bond investors, this provides additional diversification options, which are crucial during economic uncertainty or central bank-driven quantitative easing (QE). QE has led to a “crowding-out” in many European HQLA markets, where banks increasingly struggled to find profitable, high-quality liquid assets at the time.

Apart from reviewing the CBD, the EBA has been tasked with creating proposals for a third-country equivalence regime for Covered Bonds. Due to the current absence of such a regime, some investors exhibit uncertainty regarding the treatment of Covered Bonds from third countries. It would be beneficial to create regulatory frameworks that facilitate investments in international Covered Bonds, further enhancing portfolio diversification and stability.

Another innovative aspect that increases interest in Covered Bonds is the possibility of developing European Structured Notes (ESNs) based on the proven techniques of Covered Bonds. The “dual recourse” approach could be combined with different underlying assets, providing additional risk diversification and increasing the flexibility of banks in asset allocation.

In summary, Covered Bonds represent a highly attractive investment form a bank treasury perspective. They offer not only a sensible option to meet regulatory requirements but also a combination of yield, security, and transparency. By promoting diversification and creating a stable investment environment, Covered Bonds are well-positioned as a key instrument in banks’ investment strategies.

The bottom line

After a slow start to the year, covered bond supply has picked up and we’re looking at a net positive pace for the fourth year running. While 2025 has not seen a similar surge in the number of new investors as 2024, demand has continued to be strong for the asset class. After real money accounts stepped up their pace in 2024, it has rather been central banks / official institutions out to 5Y and insurance / pension buyers at the long end to pick up the pace with banks focussing more on SSA sectors for much of 2025.

Looking at the results of our investor survey, more than half of our respondents plan to still build up exposure in the asset class further with spreads vs swaps and SSAs the main angle to assess relative value. Concerns have shifted from covered bond specific ones towards external factors such as tighter Bund-ASW spreads and increased public sector supply possibly crowding out covered bonds. Issuer or collateral quality are not a major concern at this point and even CRE assets are seen as less problematic than in 2024.

Turning to regulation, a third country equivalence regime for covered bonds would be welcomed by investors. It would lead to a reassessment of relative value and to some extent larger holdings above all amongst bank treasuries who would cherish the opportunity for further diversification of their holdings. However, it would also (albeit to a lesser extent) impact asset managers’ behaviour.

Last but not least, ESG covered bond issuance has been growing but it has still played a relatively small role in terms of volumes as issuers often chose to use eligible assets for issuance further down the capital structure. For the investors in our survey, approaches to ESG in covered bond markets also differ. Less than 40% have a specific mandate for ESG covered bonds and while some are happy to work with the issuer designations of a bond being green or social, others take a more holistic view and score the issuers with their own internal assessments rather than look at the bond in question. What most have in common, though, is that similar to last year’s survey, they do not materially differ between conventional and ESG covered bonds when it comes to spread valuations. Smaller new issue premiums are accepted by some but only few are happy to buy ESG covered bonds inside conventional ones.