A Global Perspective for the Covered Bond Industry

GLOBAL ISSUANCE REMAINS STRONG DESPITE GEOPOLITICAL TENSIONS

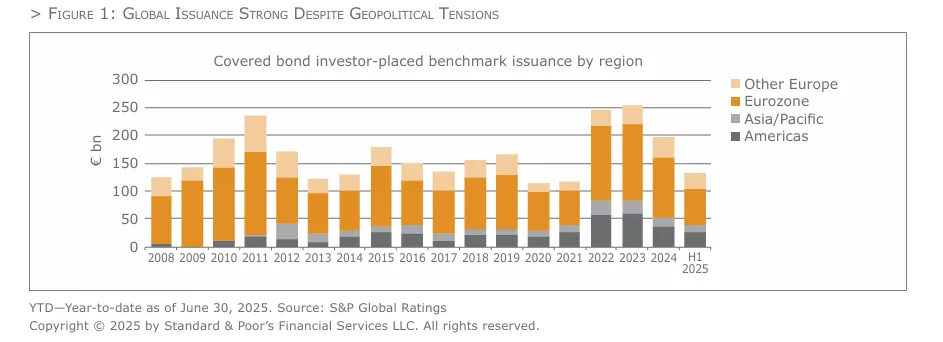

Global investor-placed benchmark covered bond issuance reached almost EUR 138 billion in the first half of 2025, slightly up from EUR 135 billion in the equivalent period in 2024. Despite a slowdown in April 2025 due to market volatility sparked by U.S. announcements on trade tariffs, covered bond issuance has since bounced back strongly, supported by slower growth in banks’ deposit funding and faster growth in their loan books. Benchmark issuance by non-European banks has also increased towards the elevated levels of 2022 and 2023, helped by the raising scheduled redemption in Australia and Canada. We expect global issuance to remain robust in the rest of 2025, reaching similar levels to those in 2024.

BANK LIQUIDITY CONSTRAINS BENCHMARK CEE ISSUANCE

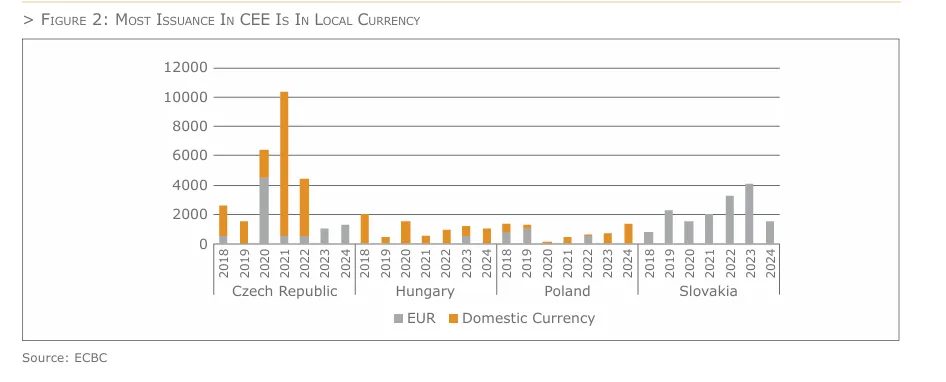

In the first half of 2025, euro-denominated benchmark covered bond issuance in Central and Eastern Europe (CEE) already exceeded the entire 2024 amount, but overall volumes remain fairly limited compared with other regions. We expect that euro-denominated issuance will remain subdued, due to ample bank liquidity and, in some instances, vibrant local-currency markets. Domestic issuance, predominant in countries such as the Czech Republic, Hungary and Poland, is partially replacing international issuance, while euro-denominated issuance is robust in countries that have already joined the euro, such as Slovakia and Estonia. Slovakian banks continued to be the most active in the euro denominated benchmark sector. In June, a Hungarian and a Polish bank issued investor-placed international covered bonds after years of absence from this segment of the market, but domestic currency issuance remains predominant in many CEE countries which have not joined the euro. The EU’s harmonization directive – which introduced a common definition of covered bonds across Europe – has not yet led to issuance in EU countries that previously lacked dedicated legislation, such as Croatia and Bulgaria. Bulgaria will join the euro in 2026, potentially facilitating issuance. But when Croatia joined the euro in 2023 local banks did not set up covered bond programs. Here, as in many CEE countries, ample liquidity is disincentivizing the issuance of covered bonds. Several countries are negotiating their accession to the European Union. As part of the accession process, they need to reform their national laws to align with EU rules, regulations and standard. The introduction of local covered bond legislation could be part of these reforms, but we don’t expect international issuance anytime soon, due to the length and uncertainties of the accession process and the size of the local banking systems.

LEGISLATIVE DEVELOPMENTS WILL DRIVE GROWTH OUTSIDE EUROPE

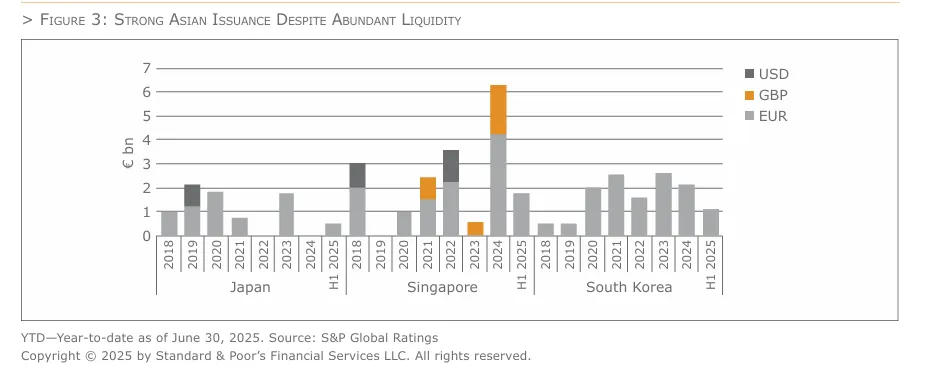

Korea and Singapore pioneered covered bond issuance in developed Asia. As local banks’ primary funding source is customer deposits, their main motivation in establishing covered bond programs was to manage asset-liability mismatch risk and diversify their funding sources. In 2018, the first covered bond program was set up in Japan. Because there is no dedicated local covered bond legislation, the program was based on a contractual structure. Despite abundant liquidity, Asian banks remained active in the covered bond market. This is testament to the strategic importance that covered bonds play in their funding strategies. We expect that the availability of customer deposits and limited loan book growth will continue to constrain issuance in developed Asia. In developed markets growth will probably come from new issuers entering exist ing markets, as well as legislative and regulatory initiatives. For example, in Japan, dedicated regulation or legislation could incentivize new banks to set up programs. But we see greater growth potential in developing countries, in Asian and beyond, where we expect housing finance needs to grow substantially, but legislative developments will be essential. In 2022, almost a decade after the introduction of the draft law, Morocco approved the first dedicated covered bond framework in Africa. While covered bonds can play a significant role in supporting housing finance in the continent, the experience in Morocco shows that the legislative process can take longer than expected. Georgia also approved dedicated covered bond legislation in 2022. We understand that covered bonds will initially be used as collateral under existing funding operations with the central bank and only at a later stage will they be distributed to private investors, probably initially domestic ones. This points to the challenges that traditional covered bonds may experience as they expand outside Europe. Covered bonds – an overwhelmingly European phenomenon for most of their 250-year history – have recently proved very popular in new markets such as Australia, Canada, Korea and Singapore. These developed econo mies aligned their models to European best-practice: local banks typically issue ‘AAA’-rated covered bonds, backed by prime residential mortgage loans, and under an established legal framework. But the greatest growth potential is probably in emerging markets, where the middle-class will expand the most in the coming decades.

Countries such as China, India, Mexico, and Indonesia could greatly benefit from a dual recourse instrument helping them mobilize private capital toward financing their growing economies. But as dual recourse financ ing expands in these markets, we can expect to see new issuers, assets, structures, and ultimately investors, challenging the established definition of what constitutes a covered bond. While covered bonds in new markets have so far primarily targeted the traditional European investor base, Brazilian covered bonds have initially attracted domestic investors. And we have seen how Georgian banks will initially use covered bonds as collateral under the local central bank’s liquidity facility, rather than placing them with international investors. More generally, we can expect that a larger share of covered bonds issued outside Europe will target domestic investors, at least initially. While covered bonds are typically issued by banks, we anticipate an increasing interest from non-bank financial institutions, such as housing finance companies in India, or even non-financial entities. And some of these new issuers will consider covered bonds backed by non-traditional assets, such as the recent examples of Indian covered bonds secured by gold loans or vehicle loans, or Turkish covered bonds backed by unsecured loans to small and mid-sized enterprises (SMEs). Turkish banks have issued SME covered bonds since unsecured SME loans are eligible collateral under the local legal framework. Banks elsewhere may consider issuing SME covered bonds even if SME loans are not eligible col lateral under the local framework, or even in the absence of a local framework. This is because in certain legal contexts covered bonds can be issued without a dedicated legal framework. Issuers can establish programs that replicate the main features of legislation-enabled covered bonds by means of contractual arrangements (so called structured covered bond programs). For example, the first two Japanese programs have been established based on a contractual structure, due to the lack of a dedicated legislation. Such contractual arrangements grant greater flexibility outside of an established legal framework, for example in terms of eligible collateral. The global success of covered bonds will lead more issuers to use the covered bond label for their dual-recourse issuance. This will create benefits but also risks. New issuers and investors will benefit the entire covered bond market – by increasing its depth and systemic importance –, the development of local capital markets – by improving liquidity and broadening the investor basis –, and society at large – by funding the growth of hous ing markets and economies. But new issuers, assets, and structures may also introduce risks to an asset class characterized by an unblemished credit history. In Europe, the harmonization directive mitigates this threat, by introducing a common definition aligned with regional best practices. Outside Europe, market participants and regulators may be tempted to align their frameworks to the definitions of the Directive, especially if Europpean regulatory authorities decide to grant equivalent treatment to covered bonds issued by credit institutions outside the European Economic Area.

THIRD COUNTRY EQUIVALENCE

Since July 2022, the regulatory treatment of covered bonds within the European Union (EU) is based on a harmonization framework which consists of a directive, that introduces a common definition of covered bonds, and a regulation, that amends the EU’s Capital Requirements Regulation. The directive also defines the pathway to achieve third country equivalence, the alignment of the regulatory treatment of covered bonds issued by credit institutions inside and outside the European Economic Area (EEA). Article 31 of the directive stipulates that the European Commission (EC) will submit a report on third country equivalence to the European Parliament and Council, which may be accompanied by a legislative proposal on whether or how an equivalence regime should be introduced. The EC’s assessments of equivalence are usually based on technical advice from European Supervisory Authorities, such as the European Banking Authority (EBA). In July 2023 the EC issued a call for advice (CfA) to the EBA on the performance and review of the EU Covered Bond Directive, including third country equivalence. The EC requested a response from the EBA before the end of June 2025. However, at the end of July no proposal has yet been published. Based on information available, it is likely the EBA will recommend a principles-based approach for third coun try equivalence, which would give third country legislators and their markets the necessary flexibility to adapt the rules to national specifics. Most likely, the EBA’s proposal on third country equivalence will cover the following areas: 1) issuance by a credit institution; 2) existence of a legal framework; 3) dual recourse; 4) asset segregation (bankruptcy remoteness); 5) eligible cover pool assets (quality requirements for asset types, derivatives, loan-to-value (LTV) ratios, and valuation); 6) coverage requirements; 7) special public supervision; 8) liquidity rules; and 9) transparency (reporting and disclosures). In essence, the EBA will propose that the third-country covered bond law would have to address the requirements of the Covered Bond Directive, while the requirements of Art. 129 CRR could be part of issuers’ programmes. Striking the right balance between the safety features of product components and the necessary flexibility for third countries and their market traditions will be challenging. A principles-based proposal certainly offers the opportunity to master this fine balancing act. It would therefore be desirable for the EU Commission to follow this proposal and transpose it into European law accordingly. Considering that a potential legislative proposal must be adopted through an ordinary legislative procedure at a European level, the overall schedule might be stretched to 2026 or even beyond. Notably, any final decision on third country equivalence will be made by the EU-Commission on a case-by-case basis. The Commission has discretionary leeway, whereby reciprocity, i.e. the treatment of covered bonds from the EU in the third country, is likely to play a role, as are political considerations. European covered bonds receive preferential regulatory treatment that extends beyond risk weightings to include:

> Favorable treatment under the liquidity coverage ratio and the net stable funding ratio standards;

> The definition of exposure and investment limits;

> The eligibility rules as collateral in central bank liquidity schemes;

and > The exemption from bail-in.

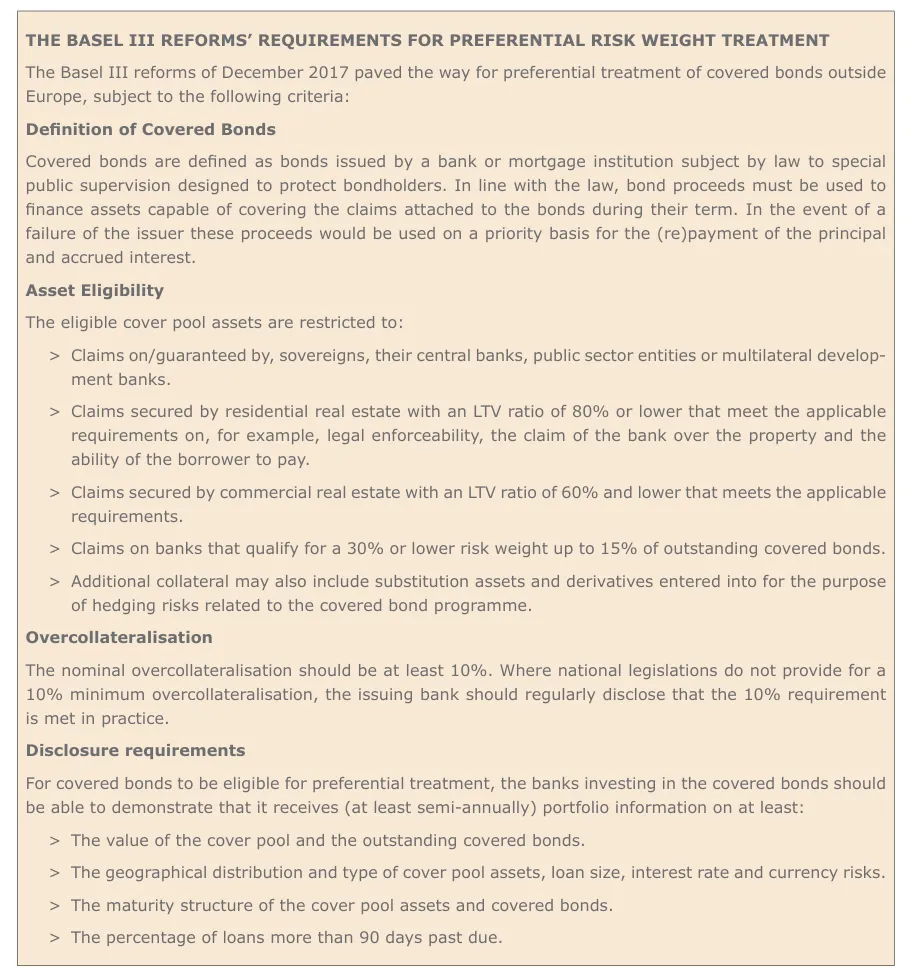

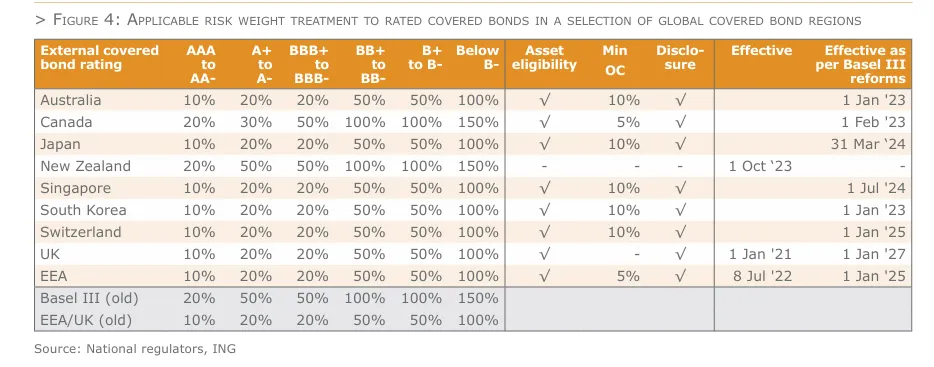

While the Basel III reforms implementation has enabled preferential risk weights for covered bonds purchased by banks outside Europe, not all countries that have already implemented the Basel III reforms have decided to provide such favorable treatment.

Importantly, covered bonds issued by credit institutions outside the EEA and purchased by European investors still receive less favorable regulatory treatment than covered bonds issued by EEA-based credit institutions.

CURRENT ALIGNMENT WITH THE DIRECTIVE

Established in 2015, the European Covered Bond Council’s Global Issues Working Group (GIWG) aims to promote a better global understanding of covered bonds and foster convergence between countries towards similar market solutions, infrastructure, and regulatory treatment. Over the past few years, the GIWG has analyzed the alignment of global covered bond regimes with the cov ered bond harmonization directive. In February 2024 the GIWG published a Concept Note on third country equivalence, the result of a consultation with market participants such financial analysts, issuers’ representa tives and investment bankers, and local authorities. The analysis revealed full alignment with the dual-recourse requirements and an almost full alignment with the bankruptcy remoteness and asset segregation requirements. On the other hand, virtually none of the global regimes provide for intragroup or joint funding options. However, the lack of alignment with these requirements is not particularly relevant because, for example, the intragroup covered bond funding is only an option for national legislators. Hence there is no obligation to implement it globally. The directive already allows for non-EU assets to be included in cover pools if they meet the directive’s eligibility criteria, and their realization is similarly legally enforceable to EU assets. Most global covered bond regimes have established asset eligibility criteria that already partially meet the directive’s requirements. Asset coverage may require further clarification. This is because non-EEA regimes provide for nominal cover age but are not always as detailed as the directive about the type of cover pool assets that should contribute to the coverage requirement. The minimum required nominal overcollateralization level of 5% as specified in the amended Article 129 of the CRR is only included in one single third country legal framework. But issuers often meet this requirement on a contractual level, and if voluntary overcollateralization is consid ered too, all jurisdictions would meet this requirement. Most global covered bond jurisdictions do not explicitly provide for a 180-day liquidity rule, but their frameworks often include other types of liquidity provisioning. While commonly allowed, the use of extendable maturity structures is also not necessarily enshrined in law. And while non-EEA frameworks lack objective extension trig gers, maturity extension triggers are, where applicable, mostly detailed in the contractual terms and conditions. Global covered bond regimes are subject to covered bond public supervision, but the law does not explicitly require competent authorities to have the expertise, resources, operational capacity, powers, and independ ence necessary to conduct public covered bond supervision. Global covered bond regimes require permission from the relevant authority to issue covered bonds, but some countries lack detailed requirements for permission. Supervision provisions in insolvency or resolution regimes are also often not as detailed as stipulated in the directive, while the global frameworks differ significantly in their reporting requirements to the authorities.

GLOBAL DEVELOPMENTS AND THIRD COUNTRY EQUIVALENCE

Country differences in risk weight treatment of covered bonds remain Considering the potential importance of reciprocity, it is important to be aware that, even with the implementa tion of the Basel III reforms, not all non-EEA jurisdictions introduced a favourable risk weighting for covered bonds. Countries that do, mostly adopted one-on-one the criteria for such preferential risk weight treatment along the lines of the Basel-III reforms. The majority of these third country regions do not discriminate between the risk weight treatment of home country and third country covered bonds. The EEA and UK are the only ones that, currently, do.

IMPLEMENTATION DIFFERS BY COUNTRY

Singapore, South Korea and Japan fully implemented the BCBS requirements for the preferential risk weight treatment of covered bonds. Australia also introduced a favourable risk weight treatment, but only for rated covered bonds. Switzerland made a distinction between Swiss legislative covered bonds and foreign covered bonds. While all covered bonds issued in accordance with the Swiss covered bond law (Pfandbriefgesetz) will benefit from a 10% risk weight under the standardised approach, foreign covered bonds will benefit from a favourable risk weight treatment along the lines of the BCBS criteria. In Canada, the Office of the Superintendent of Financial Institutions (OSFI) adopted the asset eligibility and disclosure requirements for covered bonds of the Basel reforms, but with a minimum overcollateralisation requirement of 5%. Credit quality step (CQS) 1 rated covered bonds meeting these requirements still only benefit from a 20% risk weight. If the requirements are not met, the covered bonds are risk weighted based on the external credit rating of the issuing bank. New Zealand does not have separate risk weights for covered bonds. Claims on a bank are risk weighted according to their rating grade. For rated exposures with an origi nal maturity of more than three months these risk weights are comparable to the old Basel III requirements. Since 1 January 2021, the UK defines “CRR covered bonds” referred to in Article 129 of the CRR as bonds issued by UK credit institutions and subject to special supervision. The UK has initially been insistent, that from 1 January 2027 onwards with the implementation of the Basel reforms, it would continue to apply a pref erential risk weight treatment to only UK covered bonds. Non-UK covered bonds would then, by default, also face a four times’ higher 45% LGD compared to “CRR covered bonds” (11.25% LGD) under internal models. However, in a policy update from July 2025, HM Treasury proposed the introduction of an Overseas Prudential Requirements Regime (OPRR) to identify overseas covered bond jurisdictions that could in the future receive equivalent prudential treatment.

Equivalence and the LCR treatment of third country covered bonds in the EU

Third country covered bonds are already eligible as level 2a high quality liquid assets under the EU LCR del egated regulation if they meet the applicable requirements. An EU third country equivalence decision will make little difference in that regard, unless the EU would decide to link LCR level 1 eligibility to the third country equivalence recognition for risk weight purposes. Even without such an outcome, a positive equivalence ruling could, for LCR level 2a considerations, still serve as a welcome confirmation that the supervisory and regula tory arrangements of third countries are similar to those applied in the EU.

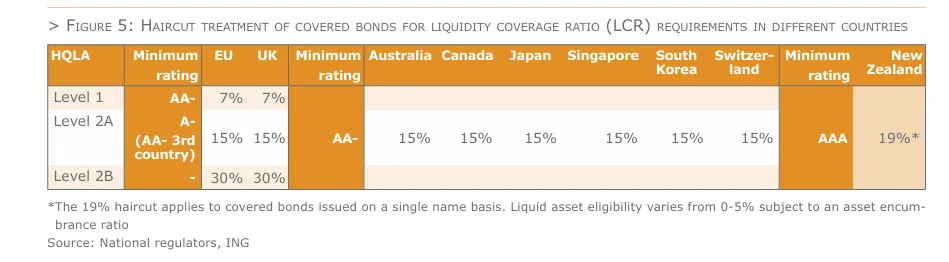

The LCR treatment of covered bonds outside the EU

Most major covered bond jurisdictions outside Europe recognize covered bonds as level 2a qualifying liquid assets (subject to a 15% haircut). The criteria for the LCR eligibility of covered bonds are typically more lenient than in the EU and mostly based upon the basic Basel Committee stipulations. Accordingly, in Australia PSA 210 facilitates the use of covered bonds as LCR level 2a eligible assets. However, APRA momentarily does not recognize any level 2 assets as qualifying for HQLA purposes. This may change in the future, if APRA decides to include covered bonds in its definition of HQLA following the July 2025 review of the Council of Financial Regulators’ (CFR) into small and medium-sized banks. Only the UK LCR eligibility criteria are comparable with the EU. The UK Prudential Regulation Authority (PRA) accepts eligible UK covered bonds as level 1 assets that can benefit from a 7% haircut, and eligible non-UK covered bonds as level 2a assets subject to a 15% haircut if they meet the applicable requirements. In April 2025, the UK PRA announced the phasing out of the LCR eligibility of non-UK covered bonds over time, while stalling this decision days after pending its further clarification. Against the backdrop of the intended estab lishment of an equivalence regime for non-UK covered bonds, the PRA decided in July 2025 to not re-launch its phasing out plans.

New Zealand never adopted the Basel liquidity metrics (LCR and net stable funding ratio) but uses its own liquidity measurements, such as the one week and one month mismatch ratio and the one-year core funding ratio. ‘AAA’ rated residential mortgage-backed securities, including covered bonds, currently qualify as primary liquid assets (PLA) in New Zealand. However, the Reserve Bank of New Zealand (RBNZ) is reviewing its liquidity policy and plans to tighten the eligibility criteria for qualifying liquid assets (PSLA/HQLA) to those that do not solely derive their liquidity from central bank collateral eligibility. Covered bonds will lose their eligibility as liquid assets on these grounds but will qualify for a new Committed Liquidity Facility (CLF) that may be established.