Assess and Classify Exposure to Physical Climate Risks - a Case for an EU-Wide Framework?

- INTRODUCTION

The European property market faces increasing threats from climate change and extreme weather events. Such events will directly affect communities and their individuals, their economies and the value of their properties. In addition, there are secondary effects to be expected on the financial services industry as well as on the broader society. It would therefore be beneficial to all stakeholders to have better transparency and higher awareness of potential impacts from physical climate risks today and in future leading to building standards with increased levels of climate change resilience. To achieve such a goal, an EU-wide framework with standardised and comparable data to assess and classify the vulnerability of buildings from acute and chronic physical climate risks in a systematic manner would certainly be useful. Such a framework could cre ate transparency and facilitate the efficient use of resources, facilitating the process of making the European property stock more resilient. Additionally, it could support the financial stability of European covered bond markets and provide investors with standardized and comparable data.

However, an assessment of each individual building in the EU with its property-specific characteristics and their available mitigants like insurances or structural elements, would be a huge undertaking and might not be feasible soon. This article provides insights to solutions available in the market as of today on portfolio and single asset level using climate prediction models applied to specific geo-locations and their buildings. There will also be an insight into an initiative having made first experiences with the development on a climate resilience certificate.

- DEFINING THE CHALLENGES

Climate Change

Climate change refers to the long-term change in the Earth’s climate in terms of changes in average tempera tures, precipitation patterns and the frequency of extreme weather events over a period of at least 30 years or more. Since 1970, the climate has warmed faster and more strongly than ever before. In its publications, the IPCC has shown that the current climate change is mainly man-made and that the rise in temperature cannot be explained without considering human action.

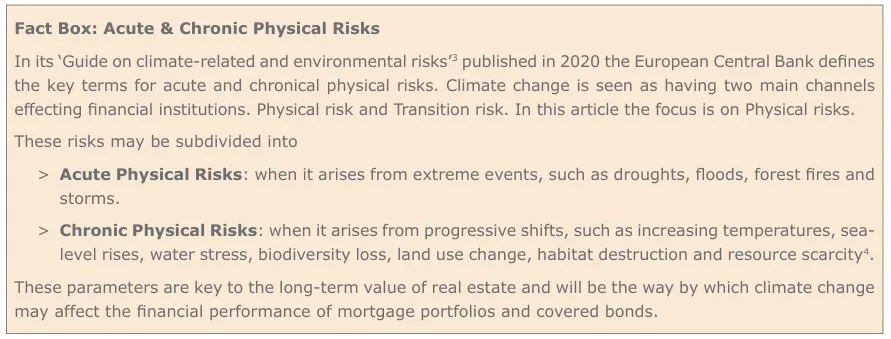

The consequences are diverse and closely linked: glaciers are melting, resulting in rising sea levels, an increase in extreme weather events, destruction of ecosystems and loss of biodiversity. Moreover, extreme weather also affects social stability, health risks, and is a cause for famine. These extreme weather events have in EU-law been classified in two categories: acute and chronic physical risks (see fact box).

Costs to Stakeholders

Climate change directly affects individuals and as these events become more frequent the effects will increase in magnitude. Effects can be direct, for example, repair costs following a flood or other natural events. They may also be indirect, rising insurance premia, higher financing costs or a reduced ability to obtain insurance and financing if risks become too high. It is also possible that the value of properties, e.g. in flood-prone areas, may fall.

Society is also experiencing the effects from climate change, both practically and financially. For example, the recent flooding of Valencia in 2024 triggered costs of more than EUR 10 bn in damages or the 2021 flooding in the Ahr-Valley in Germany resulted in costs exceeding EUR 40 bn. Germany provided EUR 30 bn aid and insurance companies paid EUR 8.5 bn in claims.

Adaptations to climate change is therefore needed. Heat protection, flood protection and adapting the sewage system are common examples. Municipalities are facing significant investment requirements. State funding programs will be required. However, resources are limited, and they must be put to the most efficient use. The non-life insurance industry faces a major challenge – financially and strategically. When extreme weather phenomena become more frequent this will increase premia and potentially make properties uninsurable if the frequency of events become too high.

Physical climate risks also affect banking. Firstly, because extreme weather conditions may result in damage that reduces collateral value and secondly because the insurance cover is only in place for the next twelve months, while mortgage loans can have maturities of up to 50 years. After an insurance claim the insurance provider might not be willing to renew the cover. This could trigger a significant mismatch with far-reaching consequences for the banking sector.

Regulation and Data

Both banks and insurances are asked by their regulators to measure and quantify the effects of climate change on their financial risks. These analyses require detailed data that still is hard to come by and proxies and estimates are often the only possible option.

Standardised property-level information is essential for effective risk management. First, it enables accurate assessment of potential consequences for the institution. Second, it supports customer relationship management. Third, it allows institutions to clearly communicate risk levels to counterparties and investors. These considerations highlight the importance of data availability and standardisation.

Although property-level data remains incomplete, standardised methods for assessing exposure to physical climate risk have been developed – primarily by the reinsurance industry, rating agencies, and various start-ups.

Benefits of Standardisation

Financial markets rely on standardisation, transparency, and predictability. In the context of climate risk, analytical tools for risk assessment are increasingly converging toward standardised methodologies, although discrepancies in classification and quantification persist. Harmonising climate-related risk metrics would enhance the comparability of key risk indicators across institutions.

Moreover, detailed property-level information is essential not only for fostering transparency but also for man aging complexity. Introducing a climate resilience certificate or rating system for properties could support the analysis of complex sets of factors in a uniform way.

Crucially, the technical specifications of buildings vary significantly, and these differences play a critical role in determining a structure’s resilience relative to others. Evidence suggests that such characteristics can influence the outcome of stress events. Therefore, systematically capturing and integrating real estate attributes would contribute to more accurate and reliable property valuations.

- ASSESSING VULNERABILITY OF BUILDINGS TO PHYSICAL CLIMATE RISKS

The analysis of physical climate risks requires the integration of property-specific data with geographical, geological, and meteorological information. Building characteristics help determine the potential consequences of extreme weather events, while geographical and geological data inform both the likelihood and severity of such events. Meteorological information primarily contributes to assessing the probability of extreme weather occurrences.

This analysis can be conducted at varying levels of precision. While proxies and modelled data may suffice for aggregate-level assessments, the impact of climate risks can differ significantly between individual properties. Consequently, property owners have a vested interest in ensuring that their assets are accurately evaluated.

In the interim, financial institutions and investors have several approaches available for assessing both acute and chronic physical climate risks. These frameworks differ primarily in the climate models employed, the granularity of geolocation data, and the extent to which they account for existing mitigation measures. The following sections present two widely used methodologies from the reinsurance industry, which are particularly popular among banks in the European Union. These examples demonstrate how climate risk can be assessed at both the portfolio and individual property levels. Additionally, a growing number of providers offer physical climate risk assessment tools. For instance, rating agencies have begun incorporating physical climate risk modules into their ESG-Scorings. Moreover, some climate risk data is publicly available at no extra cost.

Methods to Quantify Physical Climate Risk

The reinsurance industry was among the first to develop physical climate risk models aimed at quantifying risk in absolute and relative terms over short-, medium-, and long-term horizons. To estimate the potential financial impact of physical climate risks, these models typically multiply the expected intensity of a hazard by asset vulnerability curves. These curves represent the estimated damage to buildings across different regions, accounting for variations in building types, construction materials, and local building codes.

In simplified terms, multiplying this risk indicator by the cost of rebuilding a property yields the expected monetary loss – expressed in euros – due to physical climate risk, whether at the portfolio or individual asset level. For instance, this type of indicator can serve as a standardised metric for quantifying the financial cost of climate change. Munich Re refers to this metric as the “Climate Expected Loss.”

Another way to get around this issue was developed by the German natural hazard assessment tools K.A.R.L.® and VIDA. K.A.R.L.® combines the natural hazard and location analysis with an object analysis to identify the quantified or qualified risk. Therefore, K.A.R.L. looks at various building types that differ according to the type of use and the number of floors. Types of use are, for example, single/two-family houses (with or without cel lar), multi-family houses and office buildings, hospitality, flat-roofed halls and shopping centers. The number of floors provides further information about the potential impact of a natural hazard on the property. For each building cluster, a specific construction type is assumed that corresponds to the German building standard.

This framework assigns buildings to specific vulnerability clusters, even if the type of construction or the building material might differ. Nevertheless, it offers the possibility of obtaining a risk classification from the analysis that is close to the actual vulnerability of the property.

Furthermore, the clustering facilitates the analysis. The building clusters can also be determined in a very short time without the need for an on-site inspection or review of documentation. This makes the system economical to use.

In cases of very important buildings, it might be necessary and useful to carry out an individual classification to obtain an accurate assessment. However, such building surveys are costly and take time.

Acute physical risks, such as floods, storms and hailstorms, can be quantified by K.A.R.L.. The severity is set at different intensities (100-year event, 200-year event, etc.) and shows what a specific event would cost, referring to the restoration costs of the object. Considering the 1-year event up to the 10,000-year event, it is also possible to calculate an average damage per year. If this average annual loss is 1% per annum, it means that statistically the building would be a total loss after 100 years, which is classified as a high risk. To provision for such a damage frequency, 1% of the value needs to be provisioned every year.

On the other hand, it is not easy to calculate financial damage for chronic physical risks. To assess the cost of a 1°C increase in global average temperature it is necessary to work with a broader risk classification based on a traffic light system: no risk, low risk, medium risk, or high risk. This recommendation was suggested by the German Federal Environment Agency in 2022. This classification makes it possible to estimate the extent of possible damage without detailed inputs. A low risk means that although damage is possible, it is expected to be minor and therefore more or less negligible. A high risk, on the other hand, means that you should urgently consider possible adaptation measures because there is a high risk of damage occurring.

The process described here is not carried out in the same way by all providers in the market. Each provider of natural hazard and climate risk analyses has developed their own individual calculation methods to identify, describe or quantify the risk.

It is also important to note that such models typically do not incorporate the specific characteristics of indi vidual properties or account for bespoke risk mitigation measures, as would be evaluated through an individual building survey.

Impact on Property Valuations

There have been many studies showing a positive impact on valuations resulting from improved building energy efficiency through renovation. At the same time, it is increasingly recognised that climate-related and environmental risks have the potential to affect collateral values negatively and should therefore be carefully understood and managed.

Indeed, in Expectation 8 of its Guide on Climate-related & Environmental Risks, the ECB, for example, requires financial institutions “… to consider climate-related and environmental risks in their collateral valuations” and “give particular consideration to the physical locations and the energy efficiency of … real estate”. Therefore, there is an urgent need to accelerate the development of a market where energy efficiency and climate related risks are firmly embedded and reflected in valuations.

Building on the foundation of the 2017 Energy Efficient Mortgage Initiative (EEMI) Valuation Checklist & Guidance, and in close consultation with valuers from the European Mortgage Federation’s (EMF) Valuation Committee, the Royal Institution of Chartered Surveyors (RICS), and the International Valuation Standards Council (IVSC), the EMF-ECBC and its expert partners are advancing their efforts under a new EU-funded project within the EEMI framework.

As part of this initiative, the consortium is undertaking a comprehensive review, update, and expansion of the EEMI Valuation Checklist & Guidance. The objective is to ensure that the tool fully captures all ESG-related risk drivers that influence property value, thereby equipping valuers with the necessary resources to integrate relevant building characteristics and climate- and environment-related risk considerations into their assessments.

In parallel, the project is developing a complementary sustainability assessment aligned with the evolving EU regulatory and supervisory landscape. This includes a particular focus on the EU Taxonomy, the revised Capital Requirements Regulation (CRR), and the recast Energy Performance of Buildings Directive (EPBD), ensuring consistency with key legislative and policy frameworks.

To support implementation and capacity building, the initiative also includes the creation of targeted education and training materials for both valuers and financial institutions. These resources will be delivered through webinars and workshops, aimed at upskilling professionals and fostering a deeper understanding of sustaina bility-related valuation practices across the financial and real estate sectors.

Climate Resilience Certificates (CRC)

In 2021, Gävle a town 250 km north of Stockholm experienced a cloudburst resulting in 161mm of rain in 12 hours, 101mm of which fell within two hours the night between August 17 and 18. The results were severe floodings and massive destruction of property and infrastructure. This disaster triggered a research project focusing on the variation of damages and the reasons for why some properties were severely damaged while adjacent buildings were relatively unharmed.

The resulting project managed by RISE, a government research consultancy, gathered a broad representation from the real estate industry, construction, banking and insurance. The resulting report proposed a Climate Resilience Certificate system, described in the Swedish Research Institute RISE report by Thidevall et al., designed to provide a standardized assessment of property resilience against physical climate risks.

The system proposes an A-G classification, like energy performance certificates, to rate properties based on their resilience to climate-related acute and chronic physical climate risks. This classification can help property owners, banks, insurance companies and other stakeholders better understand the degree of resilience of a particular property against the effects from climate change and better prepare against the risks they might face with increasing volatile climate.

Access to comprehensive data is a requirement for the effective implementation of Climate Resilience Certificates. Therefore, the continued work by RISE, the DaSaKlim-project, focuses possible data gathering structures and necessary support, including roles and responsibilities for public and private stakeholders in Sweden.

Ultimately, the results of the Climate Resilience Certificates could unlock its full potential if they were used as real input parameter for the vulnerability curves to calculate the expected loss caused by climate hazards, just like real EPCs are used to assess the transition risks derived from the degree of CO2 Emission. In an integrated European market where property finance and insurance activities are cross border activities it is key to achieve comparability and transparency to efficiently allocate scares financial resources.

- CONCLUSION

There is a growing interest in the analysis and quantification of acute and chronic physical climate risk. The reinsurance industry pioneered the development of assessment tools to qualify and quantify physical climate risk using their experience in modelling climate impacts enriched with their comprehensive data. Their tools provide today climate risk analysis capabilities for individual properties or for large real estate portfolios. The analysis can be done as of today or with the use of various scenarios projected into the future until the end of the century in various time buckets.

In their calculations the degree of vulnerability of individual properties is based on approximations. This is where the climate resilience certificate comes into play. By establishing an EU-wide framework to assess properties for their resilience against potential climate hazards and classify the degree of their resilience, European proper ties are better prepared for climate change. This would also support financial stability and provide investors with standardized and comparable data. Ultimately this may contribute to maximize the long-term value of the European property stock to the benefit of citizens and societies alike.

Key preconditions for effective climate risk management include comparability, enhanced market transparency, robust price discovery mechanisms, stress testing, and accurate property valuations. Given the integrated nature of financial markets within the European Union, standardisation efforts should be further developed with an EU-wide framework in mind.

As this article has outlined, several climate risk management solutions are already available, albeit often relying on approximations. The introduction of a climate resilience certificate could significantly enhance the availability of granular, bottom-up data on the condition and risk profile of individual properties.

Such a certificate would not only reflect a shared recognition of the importance of climate resilience but could also serve as a catalyst for broader standardisation efforts. While implementing such an initiative across the EU would require substantial effort, it holds the potential to drive meaningful progress toward a more transparent and resilient property market.