11 October 2022

The current geopolitical context, the resulting energy crisis and climate change are making it increasingly necessary to radically rethink the regulatory framework and market best practices of the European housing finance sector. The need for a real step-up in pace in the coordination of national and European policies opens new scenarios that perhaps have never been seen before.

This turning point is already having a profound influence on current political and legislative debates on crucial market dossiers such as the EU Taxonomy, the Energy Performance of Buildings Directive, the implementation of the final Basel III reforms and, more generally, all issues related to digitalisation and sustainability.

The key to interpreting these new dynamics must be found in the political perimeter outlined by the NextGenerationEU package, which is intended to lay the foundations for a common European home and provide the keys to a future full of opportunities for upcoming generations.

The housing sector is key to the development of a clear market roadmap that will enable the European Union to achieve its goal of reducing greenhouse gas emissions. Indeed, housing is a strategic sector not only because homes are the main place where people spend their lives and, increasingly, work, but also because they account for 40% of CO2 emissions in continental Europe.

The scale of the investment needed to improve the energy performance of more than 220 million homes to meet the EU’s energy saving targets is immense and cannot be achieved by the public sector alone. The private financial sector in the EU has a central role to play in the transition to a more sustainable economy, reducing energy poverty for households, especially those that struggle to meet the transition challenges, safeguarding consumers’ wealth in terms of disposable income and asset value, and supporting economic growth and job creation. In this context, it is of strategic importance to align the interests of lenders, investors, SMEs, utilities and, above all, consumers in multi-service platforms at European level. If we are to reach our 2030 targets, almost 500,000 homes in Europe must be upgraded every week.

The real breakthrough of a net-zero Europe will come through the large-scale use of green mortgages. Today, the mortgage market is equivalent to around 46% of the EU’s GDP. Facilitating the transition to green mortgages is crucial to achieving a climate neutral economy, as highlighted by the Energy Efficient Mortgages Initiative , which seeks to introduce a greener, sustainability-focused system for purchasing, renovating and living in homes. There is therefore a need for in-depth energy renovations.

In this respect, it is important to ask how much it costs each owner, whether individuals or families, to make the necessary jump in energy class: the answer is an investment of at least €25,000-30,000. There are not many who can afford such sums without systemic help or stimulus. The problem is that if the necessary “green” improvements are not made, there will inevitably be a net and tangible loss in energy consumption.

Member States cannot fully assume this huge burden via public debt, which would mean shifting the cost to future generations, so we have to build a mechanism which brings together public and private stakeholders, working in coordination and leveraging each other’s contributions and actions. The contribution of financial markets, if combined with public intervention and structured in the right way, can give life and impetus to a genuine green renaissance, capable of giving an economic boost not only to the mortgage, construction, and real estate industries, but to the entire economy.

The positive repercussions would be felt not only from an environmental point of view, but also in terms of employment, research and development, certification and the professional skills involved in this work.

At the heart of the Energy Efficient Mortgages Initiative (EEMI) are efforts to boost and support consumer demand for buildings’ energy renovation by way of an energy efficient mortgage ‘ecosystem’. Bringing together a wide range of relevant market players, including lenders, investors, SMEs and utilities, the EEMI is aligning strategies and actions through a new, innovative market mechanism focused on a green “fulcrum” of products, services and data, delivered by way of a “one stop shop”.

With the overall objectives of optimising the end-to-end customer journey and experience, deploying market interventions and partnerships that support delivery, and therefore maximising benefits for consumers, the EEMI is concretely building an open source platform at the centre of the “ecosystem”, which will:

The EEMI is building a constellation of national platforms focussed on local characteristics and implementation needs but with a European footprint. The EEMI governance structure, combining the European-level EEM Label and Advisory Council with the EEMI national hubs, will provide the European coordination of national actions, including institutional interventions, which will support timely and cost optimised coordination between and amongst the public and private market sectors. The Energy Efficient Mortgages Initiative brings together all market stakeholders and provides them with the opportunity to share innovative solutions through its “green platform”, which promotes the idea of the EU’s New European Bauhaus. Since November 2020, the Initiative has organised 13 successful EEMI Bauhaus events with the twofold aim of building a community and stimulating market development towards the green transition. There is also another key aspect to this new green ecosystem narrative. The home is a very special place, a social driver for economic growth and cultural integration where our lives are built and our future is dreamt. On average, people spend between one third to more than half of their lives in their homes. This makes it an ideal focal point for financial education for citizens as consumers by embedding a new culture with greener microeconomic decisions in support of a transition economy.

Such an exercise should not be seen as “just” a philanthropic decision taken by already environmentally conscious people who also tend to be more affluent. It will be a win-win solution, especially for those families for whom it is more difficult to make ends meet and who are more likely to live in less energy-efficient homes and for whom running and living costs represent a larger share of their budget.

In this time of unprecedented crisis, we must turn challenges into opportunities, looking the next generation in the eyes. Our homes, the place where we raise our children, are at the heart of our lives and interests: exactly like the word “Home”, οἴκος (oikos) at the heart of the ancient Greek word “oikonomia”.

A sustainable economy must be built around the concept of “home”, the cornerstone of citizens’ interest, centred on an ESG “ecosystem” that promotes green values and raises environmental awareness.

The first building block of this new ecosystem lies in the Energy Efficient Mortgage Label (EEML) launched in 2021, which is a quality toolbox for consumers, lenders and investors, aimed at identifying energy efficient mortgages in lending institutions’ portfolios. Under the Label, banks commit to develop specific mortgage products to finance energy efficient homes or home energy renovation.

The EEM Label was created to deliver a quality market benchmark supporting recognition of and confidence in energy efficient mortgages. This was intended to be achieved by ensuring access to relevant, quality, and transparent information for potential borrowers, regulators, and other market participants. In addition, the Label aims to facilitate a process of standardisation to secure and enhance overall regulatory recognition of the asset class.

Before the official launch of the Label, the Energy Efficient Mortgages Initiative (EEMI) designed its core elements, including the IT platform and legal texts. The Label is built around the EEM Label Convention and a process of self-certification, both of which are overseen by the label governance structure consisting of: the Label Committee, the Label Secretariat and the Label Advisory Council.

The EEM Label has been developed using the Covered Bond Label as a blue-print, which is managed by the EMF-ECBC and can look back on a 10-year success story, a period during which it has established itself as the global reference point and data collection benchmark for the nearly EUR 3 tn. outstanding covered bond asset class. It is the intention that the EEM Label emulates this goal in the field of Energy Efficient Mortgages and in the wider field of financing of energy efficient renovation, scaling-up volumes and best practices on both retail activities and funding policies in the ESG sector.

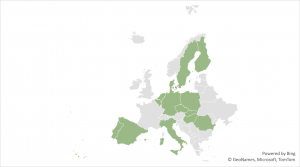

The initiative comes at a pivotal point in time, where efforts are underway at EU level to redesign the regulatory and monetary policy framework to address climate change and transition risks. As of August 2022, 38 pioneering lending institutions from 14 countries have adopted the Energy Efficient Mortgage (EEM) Label, covering the four corners of the Old Continent, large and small lending institutions, traditional banks and FinTech platforms.

Figure 1. Geographical breakdown of EEM Label lending institutions

Source: EEM Label Data

The EEML provides information on the portfolios of energy efficient loans as assets to be included in green covered bonds, allows for enhanced evaluation and tracking of their financial performance relative to alternatives and provides greater transparency regarding climate risks and resilience.

The EEM Label is granted either to a specific product offered by a lending institution or to the entirety of mortgages which are aligned with the EEM Label Convention. At the time of writing there are 53 labelled products registered. Considering the heterogeneity of alternative available loans to support the energy efficient improvement of dwellings, on the EEM Label website there is also a section for “complementary products” where financial institutions can upload general information on other products, such as personal loans, green accounts, renovation loans and loans to acquire energy savings solutions.

To be part of the EEM Label interested parties need to self-certify that they are a lending institution with products aligned with the EEM Label Convention, for which they need to disclose at least on a quarterly basis relevant information using the Harmonised Disclosure Template.

The EEM definition was launched in December 2018 and consists of high-level, principles-based guidelines for the technical assessment and valuation of eligible properties. The definition provides clear eligibility criteria for assets and projects that can be financed by energy efficient loans and for the tagging of existing assets in banks’ portfolios. The EEM definition provides the protocols to ensure appropriate lending secured against properties that are likely to have both lower credit risk and support climate change mitigation and adaptation.

Importantly, the EEM Label Committee is working on the revision of the Definition/Convention to ensure alignment, as appropriate, with the EU Taxonomy.

Finally, it is worth noting here that in recognition of the availability of different types of energy efficient/green financing products, the EEM Label website also provides the possibility to label unsecured consumer loans for energy efficient renovation purposes.

With a growing focus on sustainable finance – from regulators, market participants and investors alike – transparency and disclosure are becoming crucial drivers in harmonising best practices and in mitigating the “green-washing” risk in the capital markets arena, securing investors’ confidence and financial stability in the ESG space. Considering this, the Harmonised Disclosure Template (HDT) allows for improved comparability of energy efficiency mortgages. The key is to establish centralised and up-to-date qualitative and quantitative information, which will be available for investors, regulators and other market participants.

The objective is to stimulate the creation of a positive incentive sequence across the mortgage value chain for more consistent and standardised data collection and management, as well as for better linking loan information, property and energy efficiency characteristics in a single common template. Standardisation will facilitate investors’ due diligence, facilitate regulatory reporting requirements in this area and enhance overall transparency in the EEM and (covered) bond markets. To strike the balance between the standardised structure valid for all labelled EEM products and the national peculiarities in reporting specific data points such as the breakdown of loan size, the HDT provides for the introduction of nation-specific breakdowns managed by national coordinators.

The HDT is based on the Master Template delivered under the Energy efficient Data Protocol & Portal (EeDaPP) Project, which organises EEM “input” data and is also inspired by the successful Harmonised Transparency Template (HTT) of the Covered Bond Label. Indeed, efforts have also been undertaken to align the HTT and the HDT as much as possible to facilitate completion and due diligence by banks which have both an EEM Label and the Covered Bond Label. The HDT is furthermore fully compliant with existing regulatory and market disclosure requirements.

The HDT must be completed for each labelled EEM product at least every quarter and has the following structure:

In order to be aligned with market best practices and with regulatory requirements, the HDT undergoes an annual revision process which culminates with the approval of the updated HDT in September/October. This effort is supported by both the lending institution community and by the Disclosure Working Group comprising national coordinators, EEM Label Committee members and interested representatives of the lending institutions to support the Secretariat in gathering potential amendments to the HDT based on suggestions related to overarching and national-specific reporting and disclosure issues.

Currently, 12 lending institutions have disclosed HDTs on 17 products that are available on the EEM Label website. As with the Covered Bond Label, for the EEM Label the HDTs are exclusively publicly available via the lending institutions’ own websites whereas on the EEM Label website a reporting tool using direct links to the HDTs creates a graphical representation of the data contained therein as shown in Figure 2.

Figure 2. HDT data presentation on the EEML website

Source: EEM Label website: https://www.energy-efficient-mortgage-label.org/products

For the time being, complementary products are not required to present an HDT, but the Label Committee is already planning to develop adapted HDTs and/or extra tabs in the existing HDT to accommodate new and diversified data requirements.

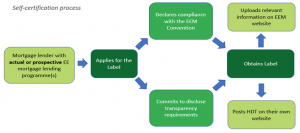

Again, drawing on the experience of the Covered Bond Label, the EEM Label is based on a process of self-certification, according to which lending institutions signal their compliance with the Convention. The process of self-certification is detailed in Figure 3.

The self-certification process highlights and testifies a real ESG engagement and strategy for labelled lenders. This process of self-certification pioneered by the Covered Bond Label has proven to work very efficiently as a result of subsequent scrutiny by other market participants, including investors and rating agencies, of the publicly disclosed HTT, representing a form of “third-party verification”. This has given rise to a market-led mechanism which effectively polices itself with the result that the cost of not accurately disclosing data or falsely declaring compliance with the Convention is high in terms of reputation and potential impact on the underlying product or ratings. This will help to mitigate any risk of “green-washing”.

Figure 3. EEM Label Self–Certification Process

Source: Energy Efficient Mortgage Label

The EEML is intended to scale-up private market support for the NextGenerationEU vision, the EU Renovation Wave Strategy and the EU Green Deal, by acting as a catalyst for consumer demand and a driver of the qualitative upgrade of the energy profile of lending institutions’ portfolios and of enhanced asset quality. Following on from the ECBC’s Covered Bond Label, the EEML will allow for identification, exchange and implementation of market and legislative best practices at European and international levels, particularly in light of the adoption of the EU Taxonomy.

Against this background a specific Taxonomy Task Force has been established which produced a first report in spring 2022 making the following recommendations to the Label Committee:

These discussion points have triggered a reflection in the Label Committee, which is discussing whether to include in the revised HDT a separate Taxonomy Tab in order to provide the possibility to lending institutions to report, where available, initial quantitative evidence that the labelled mortgages are EU Taxonomy compliant.

After a year of operation of the EEM Label, the EMF-ECBC surveyed both lending institutions and non-lenders through two surveys focusing on the appropriateness of its governance, scope, core elements and communication activities. The surveys aimed to provide insights into the user experience and expectations, which can guide improvements of the Label’s functioning and support in the further development of standards for quality and transparency in relation to energy efficient mortgages.

From the responses received to the surveys, it is apparent that the majority of actors are very satisfied with the EEM Label’s functioning and performance to date, whether this be in relation to the impacts of the EEM Label from the retail, funding and macroprudential perspectives, where multiple benefits are highlighted, or in relation to the governance structure, the HDT or strategic alignment and communication activities, for example.

Significantly, the responses also provide important indications in terms of room for further improvement in light of new and ongoing challenges. These indications pertain to access to and availability of comprehensive energy efficiency data to facilitate completion of the HDT, the extension of the HDT to include the request to expand the scope beyond mortgage products to cover personal/consumer loans, and the potential for the EEM Label to provide strategic guidance to the market with regard to the EU policy landscape.

This feedback is extremely relevant and will help steer future discussions of the EEM Label Committee with a view to addressing the points raised. Positively, the infrastructure is already in place to manage these issues, for example, by way of the EEM Label Taxonomy Task Force and the EEM Label Disclosure Working Group, which are seeking, respectively, to ensure alignment of the EEM Label with EU regulations and the EU Taxonomy in particular, and to ensure a timely revision of the HDT. Regarding access to and availability of Energy Performance Certificates (EPCs), the feedback received reconfirms the mandate given to the EEM Label Secretariat to seek policy changes at EU level which secure access of credit institutions to EPC data and registers. These efforts are ongoing and, in light of the feedback received, will continue, particularly in the context of the recast of the Energy Performance of Buildings Directive (EPBD).

The EEM Initiative and the EEM Label were designed to raise consumer awareness and appetite for buildings’ energy efficiency, which represents a core element of the market transition. Against this background, the EEMI identified the main drivers of consumer demand with a focus on the appeal, relevance and understandability of EEMs across European markets. This latest consumer research has generated key insights with regards to EEM market developments. These findings further support the need for a standardised approach in terms of information exchange between the different actors that constitute the EEM ecosystem, namely lending institutions, small and medium enterprises active in the refurbishment of the building stock, and providing energy efficient solutions for mortgage holders.

In this context, the EEM Label has undertaken several actions to introduce a product feature grid that succinctly collects the key features of the labelled products in order to provide a clear overview of the various products of the EEM Label. The grid was created to reinforce the value of the EEM Label for consumers by providing easy access to all labelled products and guiding them towards the most efficient and cost-effective financial products. All these efforts seek to scale-up the EEMI’s work, demonstrating the end-to-end customer journey and the EEM life-cycle.

Figure 4. EEM Label Product Feature Grid

Source: EEM Label website

The Energy Efficient Mortgages Initiative is leading the market towards a real cultural change in the housing sector by proposing coordinated and integrated solutions at global level for retail, funding, marketing and risk analysis strategy in the banking sector. This will accompany lenders in building common best practices and deliver new green products and solutions for consumers. This pivotal change will not only support the appetite for ESG assets in capital markets but, more importantly, help mitigate green washing, thereby facilitating investors’ due diligence and reinforcing the overall financial stability perspective in the ESG space.

The Initiative aims at scaling-up volumes, solutions, and opportunities for the entire value chain with the end goal of bringing into the hands of consumers a real and affordable microeconomic advantage when renovating their homes.

Against this backdrop, we must remember that the real decision-makers in the housing transition economy are the owners of properties who need to be encouraged to make informed decisions for the future benefit of their children, looking at the world from a new perspective. This revolutionary behaviour should be supported by the appropriate toolbox of incentives, regulation and subsidies. The banking sector is ready to provide the magnifying glasses helping them to look for a new path in their consumer journey by supplying new green products and renovation opportunities.

With the EEM Ecosystem, the mortgage and covered bond industries are laying the foundations for a win-win market paradigm that secures both economic growth and financial stability. This, it is hoped, will give rise to a Green Renaissance rooted in a new perspective of sustainability, digitalisation and social inclusion, to fund the hope for a better, greener future.

By the EMF-ECBC Secretariat

The European Covered Bond Council (ECBC) is the platform that brings together covered bond market participants including covered bond issuers, analysts, investment bankers, rating agencies and a wide range of interested stakeholders.