26 November 2020

The journey towards harmonisation of European Union (EU) covered bond frameworks reached a milestone

in November 2019 when the EU Parliament approved the text of the new Directive and Regulation. On 18

December, the text was published in the Official Journal of the European Union, implying that the Directive

entered into force on 8 January 2020. This completed a process that had started in 2014.

The next phase is to incorporate the new Directive into national covered bond laws, for which countries have

18 months. Given that the Directive is of high-level and principle-based, there is a risk that national regulators

interpret the Directive in different ways. Therefore, the ECBC has established an Implementation Task Force

to monitor the legislative implementation process. This Task Force has identified three key areas that needed

a more detailed analysis, with the conditions attached to covered bonds with extendable maturities being high

on the agenda. In this article, we discuss the main details of the new legislative package, while we also have

a detailed look at covered bonds with extendable maturities.

The legislative package includes a new Directive (i.e. rewrite of Article 52(4) of Directive 2009/65/EC) and a new Regulation (i.e. amendment of Article 129 of the CRR). The Directive will become the new single reference point for regulation related to covered bonds. It provides a common definition of covered bonds, while defining all core features of covered bonds, as well as defining the tasks and responsibilities of supervisors. Overall, it regulates the covered bond product with a focus on protecting investors. Still, the Directive has remained high-level and principle based. On the one hand, it strengthens the definition of covered bonds, while on the other hand, it prevents any harm to existing well-functioning markets.

Furthermore, member states can take into account country-specific features when implementing the Directive in national covered bond frameworks. The latter reflects that for instance, mortgage laws, insolvency laws, and bankruptcy laws are still different in many countries. The new Directive consist of the following chapters (or titles):

The articles of the Directive start off by defining the dual recourse principle and bankruptcy remoteness of covered bonds, also noting that covered bonds can only be issued by EU credit institutions. Below we touch upon the most eye-catching features of the new Directive.

Cover assets

Article 6 deals with the type of assets allowed in cover pools. It notes that only high-quality assets can be used as collateral for covered bonds, referring to points (a) to (g) of CRR Article 129 (1). This includes the ‘traditional’ cover pool assets, such as residential mortgages, commercial mortgages, public sector loans, and ship loans. Currently, 89% of covered bonds are backed by mortgages.

However, the Directive leaves room to include other high-quality assets as long as their market value can be derived, while being enforceable in one way or the other. Furthermore, there needs to be a kind of registration in the case of physical assets. In addition, assets in the form of loans to, or guaranteed by, public undertakings are allowed as cover assets under certain conditions (e.g. a minimum level of overcollateralisation of 10%). As a result, we might see the creation of cover pools with non-traditional cover assets. Moreover, the outbreak of the Covid-19 pandemic, and the focus on banks to keep lending to the real economy, could open the debate to how covered bonds could be used to help the recovery (i.e. supporting the use of covered bonds backed by non-traditional collateral assets). The covered bond industry likes to stress that it does not prefer a watering down of the quality of collateral allowed in cover pools in order to safeguard the high quality of the covered bond product. In fact, it judges the introduction of European Secured Notes (Fact Book 2019, 1.11) as a good dual-recourse alternative for non-traditional collateral assets.

The articles following Article 6 describe that issuers might include cover assets from outside the EU in cover pools as long as they meet the criteria set out in Article 6, while the level of protection should be similar to assets from the EU. Another condition related to the cover assets is that member states should ensure that there is sufficient homogeneity of the cover assets regarding, for instance, their lifetime and risk profile. Finally, the Directive includes articles regarding the cover assets that address intra-group structures, joint funding, the use of derivative contracts, segregation of assets, and the cover pool monitor.

Joint Funding

Interesting to highlight is Article 11 about joint funding, which allows the pooling of cover assets by several credit institutions. Joint funding should reduce the costs of setting up covered bond programmes for smaller credit institutions, while it should allow them to issue covered bonds in reasonable size, which improves their liquidity. As such, joint funding should support smaller credit institutions to join forces, paving their way to the covered bond market. The aim is also to create covered bond markets in countries where there is currently no well-developed market. The Baltic region is a good example, as Estonia, Latvia, and Lithuania are in the process of setting up a pan-Baltic covered bond framework, which would allow credit institutions from these countries to issue covered bonds with underlying assets from across these countries.

Reporting, OC requirements and liquidity risk

The Directive continues with proposals about the information that covered bond issuers need to provide in order to allow investors to carry out their due diligence properly. The Directive requires that issuers provide information on a quarterly basis related to the value of the cover pool and the outstanding covered bonds, a geographical split as well as type of cover assets, their market risks (including interest rate and currency risk), liquidity risks, maturity structures, and coverage.

Meanwhile, there are also important new requirements for overcollateralisation (OC) and liquidity. Indeed, the introduction of a minimum level of OC is one of the highlights of the legislative package in our view. Article 15 states that the ‘aggregate principal amount of all cover assets is equal to or exceeds the aggregate principal amount of outstanding covered bonds’. This is the so-called ‘nominal principle’. However, the Regulation also stipulates that a 5% minimum level of OC is required, based on a nominal calculation. National authorities are allowed to reduce this level to a minimum of 2% under certain conditions (i.e. the calculation of OC is either based on a model which takes into account the assigned risk weights of the assets or a model where the valuation of the assets is subject to mortgage lending value). This seems to align the new legislation with common practice in Germany and Austria.

Furthermore, Article 16 strengthens investor protection for liquidity risk, as it requires for issuers to keep liquid assets to cover the net liquidity outflow for 180 calendar days. However, the liquidity buffer has some overlap with other EU legislation, in particular with the LCR. To reduce regulatory costs, national authorities will be able to align the different forms of EU legislation, to avoid that the same outflows will be covered with different liquid assets for the same period. A rewrite of the LCR seems the best solution to tackle this issue.

What is more, liquidity risk can also be addressed by the possibility to extend the maturity date of the covered bonds in case of liquidity shortage. The Directive allows national legislators to stipulate that issuers of covered bonds with extendable maturity structures can use the extended maturity date rather than the scheduled maturity of principal payments when calculating the liquidity buffer. However, some national legislators might not allow to base the liquidity buffer on the extended maturity date. In that case, issuers of soft bullets/conditional pass-through covered bonds will be forced to calculate the liquidity buffer without taking the extension into account.

Treatment of covered bonds with extendable maturities

The Directive then pays special attention to covered bonds with extendable maturities. It stresses the need to harmonise extendable maturity structures across the EU by setting specific conditions for these, while avoiding them to become too complex and expose investors to higher risks. The main focus is on the triggers that allow for the maturity extension. These should be objective and well-defined, while the maturity extension should be outside the discretion of the issuer. We discuss all details and issues related to extendable maturities extensively later in this chapter.

Public supervision

The new Directive continues with many pages about the public supervision of covered bonds. This contrasts heavily with the current legal framework, which does not define the nature, content and authorities that should be responsible for supervision. It is therefore essential to further harmonise public supervision of covered bonds, making clear the tasks and responsibilities of national supervisors for covered bonds. Furthermore, it should be ensured that supervisors have all the capabilities and means to carry out their role in a proper way. Indeed, the articles on public supervision address issues such as reporting requirements to authorities, the powers that supervisors have in case of non-compliance of issuers, and the role of the supervisor when an issuer is insolvent or in resolution. In the end, strengthened supervision will improve investor protection.

Labelling

The Directive introduces two new labels to the covered bond universe, albeit their use is facultative. Issuers can use the ‘European Covered Bond’ label for covered bonds that only comply with the Directive, while they can use the ‘European Covered Bond (Premium)’ label when the covered bonds also comply with the CRR. This should make it easier for investors to assess the quality of the covered bonds, which should increase their attractiveness inside and outside the EU, according to the Directive. Although it could help to identify the quality of different covered bonds, the Directive allows for the labels to be used in combination with national labels as well as that of the already existing Covered Bond Label. As a result, the new labels could create confusion rather than clarity.

Worth mentioning in this respect is the Covered Bond Label that the European Mortgage Federation and European Covered Bond Council already introduced in 2012. This label established a clear perimeter for the asset class and has resulted in the introduction of the Harmonised Transparency Template (HTT), which has improved transparency and reporting standards. As such, we expect that the labelling in the Directive will be absorbed by the existing Covered Bond Label which is already providing most of the reporting requirements and is actively preparing for the necessary steps to be taken.

Transition measures

The aim is to get a smooth transition towards the new Directive, which should prevent any unintended market distortions. Therefore, the Directive includes generous grandfathering provisions. Actually, all existing covered bonds that have been issued before 8 July 2022 and which comply with the UCITS Directive and the CRR will be grandfathered, keeping all existing regulatory benefits. As such, current outstanding covered bonds will not be treated differently, which should indeed allow for a smooth transition. Furthermore, it will be possible to tap already outstanding covered bonds under certain conditions (e.g. maximum of 5y remaining maturity, total issue size of taps less than twice the outstanding amount, while the total size at maturity does not exceed EUR 6bn) to 24 months after the Directive becomes effective.

Timeline

The new Directive will be fully effective 30 months after the Directive enters into force. Firstly, there will be a 18 month transposition period, after which issuers will get 12 months to comply with the new legislation. Therefore, the new legislative package will be fully effective on 8 July 2022.

Third country covered bonds and extendable maturities assessment

The Directive also includes calls for reviews and reports after the Directive has become effective. The regulatory treatment of covered bonds issued by credit institutions from third countries is one worth mentioning. The EC shall, in close cooperation with the EBA, publish a report, including legislative proposals, about whether and how an equivalent regime could be introduced for third-country credit institutions issuing covered bonds. However, this will take time, as the deadline has been set at 8 July 2024. Still, the prospect of third country covered bonds receiving a similar regulatory treatment could support the further development of covered bonds outside the EU.

Also by 8 July 2024, the EC should submit a report, and if appropriate a legislative proposal as well, about the risks and benefits of covered bonds with extendable maturity structures. This study should also be conducted in close cooperation with the EBA. Finally, by 8 July 2025, a report should be submitted about the implementation of the Directive and the developments of the covered bond market more generally. That report should also include recommendations for further action.

Finally, there is the request to the EC to adopt a report on the possibility of introducing the earlier mentioned dual-recourse instrument called European Secured Notes.

Amending Article 129 of the CRR

Amendments to Article 129 of the CRR are also part of the legislative package. These changes will be two-fold. On the one hand, some parts of the CRR Article 129 will be deleted. This is for instance true for the reporting requirements, which will be shifted towards the Directive. Furthermore, it will no longer be allowed to use as cover assets RMBS/CMBS or senior units issued by French Fonds Communs de Titrisation securitising residential or commercial property exposures.

Regarding the inclusion of substitution assets in the cover pool, it will be allowed to use substitution assets qualifying as credit quality step 2 for a maximum of 10% of outstanding covered bonds and also short-term deposits and derivative exposures qualifying as credit quality step 3 for a maximum of 8% of outstanding covered bonds. Before, only assets with credit quality step 1 were allowed (up to 15%), while now the substitution assets with credit quality step 1,2 and 3 together cannot exceed 15%. This amendment was due to the increased difficulty to comply with the former stricter rule.

Meanwhile, the minimum required level of OC has also been specified in the CRR (see above). Furthermore, the amendments address the issue of LTV limits. Overall, the authorities stick to the 80% LTV limit for residential mortgages, 60% for commercial mortgages (with possibility to rise to 70%), and 60% for ship loans. However, the CRR is more explicit in saying that these are soft limits, implying that a loan in the pool can only act as collateral within the LTV limits without the need for the loans that exceed the required limits to be removed from the cover pool.

Alignment with proposals

All EU Member States need to adjust their covered bond frameworks to fully align them with the new Directive and Regulation. Overall, we do not expect major issues regarding the implementation of the new Directive in different countries, although some countries (e.g. Spain) have probably more issues updating their covered bond law.

Response of the sector and rating agencies

The covered bond community gave the new legislative package a warm welcome, saying it was extremely pleased with the outcome. The ECBC noted that ‘The Package provides a basis for enhanced harmonisation of the European covered bond market, in line with the objectives of the CMU, reinforcing a European common qualitative benchmark for international investors and respecting well-functioning traditional markets. It moreover paves the way for the smooth introduction of this asset class in newer and emerging covered bond markets in the Union, such as those in the Baltic regions, Poland, Slovakia and Romania, and will also serve as an important legislative benchmark on a global level for countries such as Australia, Brazil, Canada, Japan and Singapore’. The rating agencies also welcomed the new package, also stressing that it will further strengthen the quality of covered bonds, which is credit positive.

Extendable maturities: the new standard

We now turn to the discussion related to covered bonds with extendable maturities being the new standard. The most fundamental idea of covered bonds is safeguarding a steady flow of payments to investors following an issuer event of default. Once the issuer ceases to exist, the cash-flow stemming from a separate portfolio of assets is used to cover all claims due to bondholders. The two most significant sources of risk threatening the ability to satisfy the claims are (i) credit default risk, which potentially leads to an over-indebted cover pool and (ii) market risk – first and foremost in the form of liquidity risk – which potentially leads to a sufficiently large cover pool, which, however, is no longer able to satisfy claims due to illiquidity.

In the past, following an issuer default, the cover pool administrator could easily monetise the assets in the cover pool either by disposing parts of the cover assets or in an indirect way, i.e. by bundling them into an asset-backed security (ABS) or – if applicable – by using the refinance register. In particular against the backdrop of uncertainty regarding the functionality and the efficiency of these tools, it is particularly important that the cover pool administrator is equipped with a broad set of instruments so he is free to pick the most efficient one.

In cases involving hard bullet structures, issuers try to enhance the effectiveness of the tools by regularly calculating pre-maturity tests or by maintaining a certain amount of liquid assets in the cover pool – a costly exercise for issuers since liquid assets usually come with a negative carry. By extending the maturity, the liquidity and refinancing risk can be reduced. This can be achieved by either using soft bullet structures or pass-through structures. Soft bullet structures have a limited extension period of usually one year. However, since the soft bullet timeframe might still turn out to be insufficiently long, pass-through structures were introduced with the aim to completely eliminate any refinancing risk by eliminating pressure to sell assets at the expense of a maximum timeframe for the payment deferral.

Below, the definition of hard, soft and conditional pass-through covered bonds provided by the ECBC1:

> “Hard bullet covered bonds: are repaid on the scheduled maturity date. Neither the documentation nor the legal framework contain provisions for a maturity extension. Failure to repay the final redemption amount of a hard bullet covered bond on the scheduled maturity date could trigger the default of the relevant covered bonds and, possibly, the liquidation of the cover pool depending on the respective national insolvency rules.

> Soft bullet covered bonds: Soft bullet covered bonds have a scheduled maturity date and an extended maturity date. If objective, predefined and transparent criteria have been met, the maturity of a soft bullet covered bond can, and in some cases, will automatically, be prolonged up to the extended maturity date. During the extension period, the covered bond may be redeemed using cover pool proceeds. Failure to repay a covered bond on the extended maturity date triggers the default of the relevant extended covered bonds (unless multiple extensions are allowed).

> Conditional pass-through covered bonds (CPTCB): Conditional pass-through covered bonds have a scheduled maturity date and an extension mechanism. By itself, the failure to repay the CPTCB on the scheduled maturity date does not lead to an acceleration of the covered bond but to an extension of the maturity date of this and potentially other relevant covered bonds. The extension requires that objective, predefined and transparent criteria are met. In such circumstances the maturity of a CPTCB can be prolonged to the extended maturity date, which is typically linked to the maximum legal maturity of the underlying assets. During the extension period, cash-flows received or generated from the cover assets will be distributed to the covered bonds investors. Regular attempts are in general made to sell the cover pool assets to redeem the covered bonds. Such sales are subject to predefined criteria intended to protect the interests of all investors under the same programme. In certain jurisdictions and programmes, CPTCB may feature an initial soft bullet extension.”

Soft Bullet remains the prevailing extension format

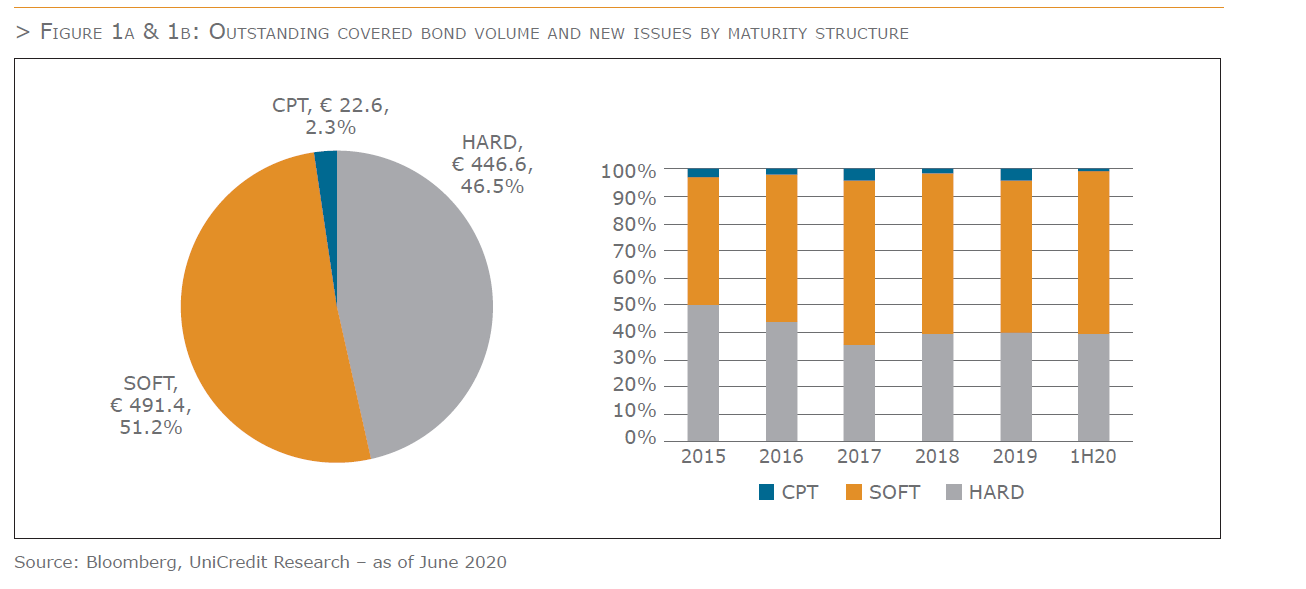

Soft bullet covered bonds remained the prevailing benchmark issuance format in 2019 and the first half of 2020. As a result, these structures continue to dominate euro-denominated benchmark covered bonds. Measured against an outstanding total volume of EUR 960 bn (as of end-June 2020), the share of soft bullet covered bonds is 51% or EUR 491 bn. Conditional pass-through covered bonds now account for 2% or EUR 23 bn. By contrast, the share of hard bullet covered bonds continued to decline at 47% or EUR 447 bn. Covered bonds with extendable maturity structures have thus dominated the outstanding volume of benchmark covered bonds since 2017 and it can be assumed that this will also be the case in the future.

The share of new benchmark issues with extendable maturity structures (soft bullet or CPTCB) was 60% in 2019 (basically unchanged versus the previous year) and also in the first half of 2020. The proportion of bonds with extendable maturities versus hard bullet covered bonds depends to a certain extent also on the countries of origin as some jurisdictions have a dominant maturity structure, for example, hard bullet structures in Germany, France or Spain. With a share of 4% in 2019, conditional pass-through covered bonds also gained ground, thus defying the ECB’s decision of 13 December 2018 that no conditional pass-through covered bonds will be purchased under CBPP3 any longer. Beside Polish, Greek and Italian issuers, in particular Dutch institutions were able to successfully place their conditional pass-through covered bonds with investors.

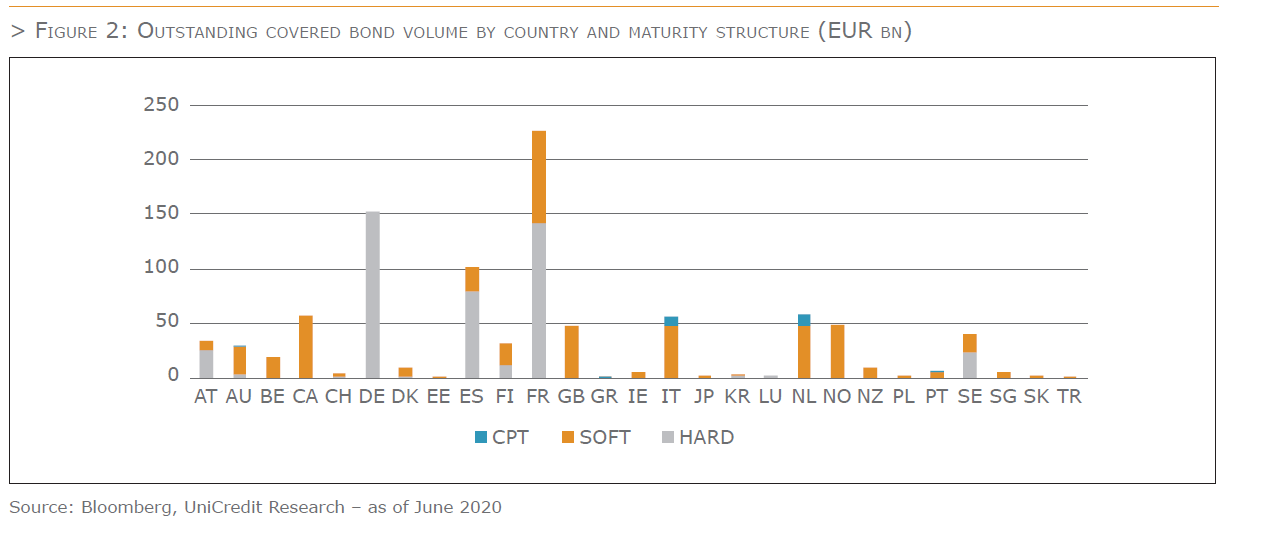

Pure hard bullet jurisdictions are becoming a rarity. The only remaining countries in the benchmark universe

are Germany (EUR 153 bn), the Spanish single Cédulas (EUR 80 bn) and Luxembourg (EUR 2 bn). Plans to

introduce a maturity extension into the German Pfandbrief Act have been the subject of discussion for a number of years and remain in place. In case that new provisions on maturity extensions in Germany would also apply to already outstanding Pfandbriefe, the proportion of outstanding hard bullet covered bonds would see another substantial decline to just 30% of benchmark covered bonds based on current figures.

Most covered bonds with an extendable maturity structure are currently issued on the basis of contractual regulations. So far, statutory requirements exist only in Poland and Denmark. With the revision of the Slovak covered bond legislation, legal regulations for extendable maturity structures in Slovakia have also entered into force at the beginning of 2018. In an insolvency, the general insolvency administrator is also responsible for the covered bond creditors. He first has to consider whether a regular continuation of the covered bond programme would lead to a reduced satisfaction of the claims of covered bond investors. If this is the case, he may transfer the covered bond programme to another Slovakian bank after prior approval from the Slovakian National Bank. The programme must be transferred within one year. Covered bonds that mature during that transfer period are automatically extended by 12 months. If the programme is not transferred in the above mentioned period, the national bank may decide to extend the period for a further 12 months.

Extendable maturity structures in the focus of EU harmonisation

As a result of the growing use of extendable maturity structures, regulators have increasingly turned their attention to them. As described earlier, the new Directive pays indeed special attention to them. The main questions raised were to what extent extendable maturity structures influence the dual recourse principle of covered bonds and the conditions of triggering an extension. For example, if the maturity extension were invoked too early, recourse to the issuer could be cut off too quickly, even though the issuer is still solvent. Moreover, if extension periods are too long, recourse to the issuer’s insolvency estate is considerably delayed. We examine extendable maturity structures in light of 1. the new Directive and Regulation and 2. the EBA’s Report on Covered Bonds, as the EBA will eventually publish a report on them as well.

1) The new Directive

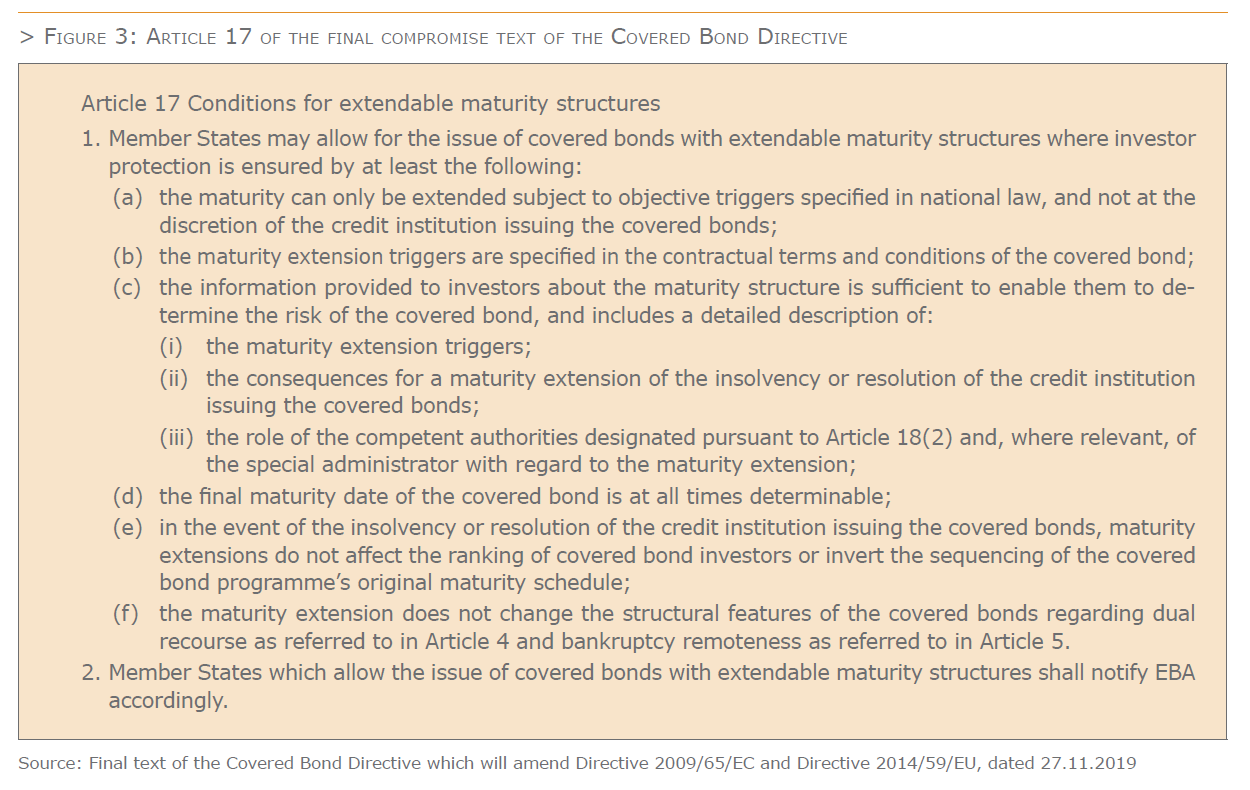

The final text of the Directive defines extendable maturity structures as “a mechanism which provides for the possibility to extend the scheduled maturity of covered bonds for a pre-determined period of time and in the event that a specific trigger occurs”. Article 17 of the final text of the Directive lays down the conditions for extendable maturity structures (see Figure 3 below).

Compared to the EBA report discussed below, the final text of the Directive has left to each national regulator to define in their respective covered bond frameworks what the maturity extension triggers should be. To avoid the risk of creating discrepancies amongst extendable maturity covered bonds across Europe, the ECBC Implementation Task Force has been set-up to identify, amongst other things, what could constitute objective triggers. The Task Force has identified two triggers, namely non-payment of principal at the final maturity date and/or the possibility for the cover pool administrator to decide to extend the maturity date of the covered bonds. Due to the various covered bond structures used in Europe, the Task Force has decided not to recommend what the consequences of an extension should be. Worth mentioning is that in the case of structures which use an SPV guarantor, the consequences of a maturity extension are clearly included in the base prospectuses of the programmes.

2) The EBA Report on Covered Bonds

In response to the addressed topics, the EBA’s report entitled “Recommendations on Harmonisation of Covered Bond Frameworks in the EU” dated 20 December 2016 put forward a wide range of requirements for soft bullet and conditional pass-through covered bonds. The recommendations aim to ensure, first, that such bonds meet the covered bond definition (step 1) and, second, that they are eligible for preferential risk treatment under the CRR (step 2). Specifically, the conditions are as follows:

In most cases, the conditions for a maturity extension are set out in the base prospectus and related final terms. So far, statutory requirements exist only in Poland, Denmark and Slovakia. In general, a distinction can be made between two types of structure:

1) Issuer and cover pool constitute legally independent entities

These are normally SPV/guarantor structures. Several requirements have to be met before the maturity can be extended. First of all, non-payment of the covered bonds by the issuer on the final maturity date will automatically trigger an issuer event of default. The payment obligation then passes to the guarantor in connection with a notice to pay/guarantee enforcement notice. If the guarantor does not have sufficient liquidity to repay the covered bonds on the original date (final maturity date), payment is deferred to the extended maturity date.

This specific approach should comply with the EBA rules. On the one hand, the decision to extend the maturity is not made at the sole discretion of the issuer alone, but ultimately depends on the guarantor’s ability to pay. The issuer not meeting its obligation to pay the covered bond on the final maturity date will trigger an issuer event of default. Accordingly, the maturity extension does not focus on the issuer’s ability to survive, but on securing the largest possible repayment for investors.

2) Issuer and cover pool constitute the same legal entity

These are generally on-balance-sheet structures. In addition to universal bank structures, specialist credit institutions and French SFHs and SCFs are included in this group.

Unlike in the jurisdictions under group 1, the conditions for a maturity extension for these structures are much more general. For example, the only requirement for an extension is that the issuer is unable to pay on maturity. The biggest difference, however, concerns the issuer event of default. In most cases, the documentation notes that a maturity extension does not lead to a default of the issuer. Conversely, this would mean that the maturity can be extended to avert or postpone an issuer default. Accordingly, an issuer event of default would not occur until non-payment of the due amount on the extended maturity date or non-payment of interest. This would contradict the EBA’s maturity extension proposals.

In the case of Polish covered bonds, a bankruptcy event of the Mortgage Bank triggers a maturity extension. However, it remains unclear if this would be in line with the EBA report which states that for specialist banks the sponsoring institution must have defaulted, and not the issuer itself.

The plans for a shift in the maturity date in Germany should also comply with the conditions drawn up by the EBA. In the event that insolvency proceedings are opened in respect of the Pfandbriefbank, each cover pool is separated as a legally independent entity with its own banking license (Pfandbriefbank with limited business activity). The management of these Pfandbrief banks with limited business activity is the responsibility of the cover pool administrator appointed in accordance with §31 PfandBG. As a result, the extension falls outside the issuer’s scope of influence.

At present, 24 countries have covered bonds with extendable maturity structures outstanding in the iBoxx € Covered Index. Twelve jurisdictions have structures that should comply with the EBA conditions. The total amount of soft bullet and conditional pass-through covered bonds outstanding in those countries is EUR 277 bn as of June 2020. In the last 12 months some Austrian issuers have adapted their base prospectuses. According to the new wording, the covered bonds will be extended automatically to the extended maturity date if resolution measures are imposed on the issuer or for example in the event of insolvency. These structures should also comply with the EBA conditions.

Conditional pass-through structures have solid footprint

In 2013, conditional pass-through structures were introduced in the covered bond benchmark universe. NIBC was the pioneer issuing a EUR 500 mn 5Y benchmark covered bond in October 2013, followed by further benchmark issues on a yearly basis. While for the first two years, conditional pass-through structures were widely discussed but remained a niche product, it was in 2015 that this redemption format started to gain momentum. At the time of writing, there are conditional pass-through covered bonds issued out of the Netherlands, Italy, Portugal, Austria, Australia, and Greece. Poland is so far, the only country, which implemented a conditional pass-through extension into its covered bonds legal framework.

Since the first CPTCB issuance back in 2013 there are today circa 20 covered bond programmes, across jurisdictions, structured in conditional pass-through format.

In CPTCB programmes in general, following an issuer event of default, any repayments, including early repayments and excess spread, remain with the cover pool until a covered bond series reaches its scheduled maturity date (SMD). Following an issuer default, a particular covered bond will only become pass-through once a covered bond reaches its SMD and the available cash is insufficient to fully redeem the bond. Other outstanding covered bonds will not turn into pass-through covered bonds as long as they are paid as scheduled. It goes without saying, that the switch to pass-through on the SMD does not prevent the cover pool administrator from trying to sell assets in order to improve the liquidity of the cover pool and, in doing so, making the switch to pass-through less likely.

The maturity extension and switch to pass-through aims to reduce refinancing risk, i.e. the risk of fire-sales. In order to generate sufficient cash flows to repay the covered bonds due, the cover pool administrator is empowered to sell a randomly selected part of the asset portfolio as long as the conditions of the amortisation test are met.

Following issuer default, the amortisation test has to be passed. The amortisation test is designed to ensure that cover assets are sufficient to repay the outstanding covered bonds. Key aspects in that respect are the level of overcollateralisation in the programme as well as provisions to address transactions risks like servicing. If the test is failed, the commonly used structure is that all covered bonds becoming pass-through. In this case, it will be required to use all funds available to redeem all covered bonds on a pro rata basis, while interest continues to accrue on the unpaid part of the covered bonds.

An important feature in the CPTCB is the minimum overcollateralisation (OC), which is needed to allow for the programme to switch to pass-through. Shortage of collateral, which could arise from paying administrative costs as well as covering potential credit losses, would otherwise instantly trigger a failure of the amortisation test and an acceleration of payments to bondholders. This reflects the fact that cover pool credit risk is the key remaining source of loss in the cover pool asset-liability-management. In order to eliminate market risk completely, the legal final maturity is extended to beyond the maximum maturity date of the cover pool assets. The extension period usually ranges from 31 years to 38 years, depending on the respective programme documentation.

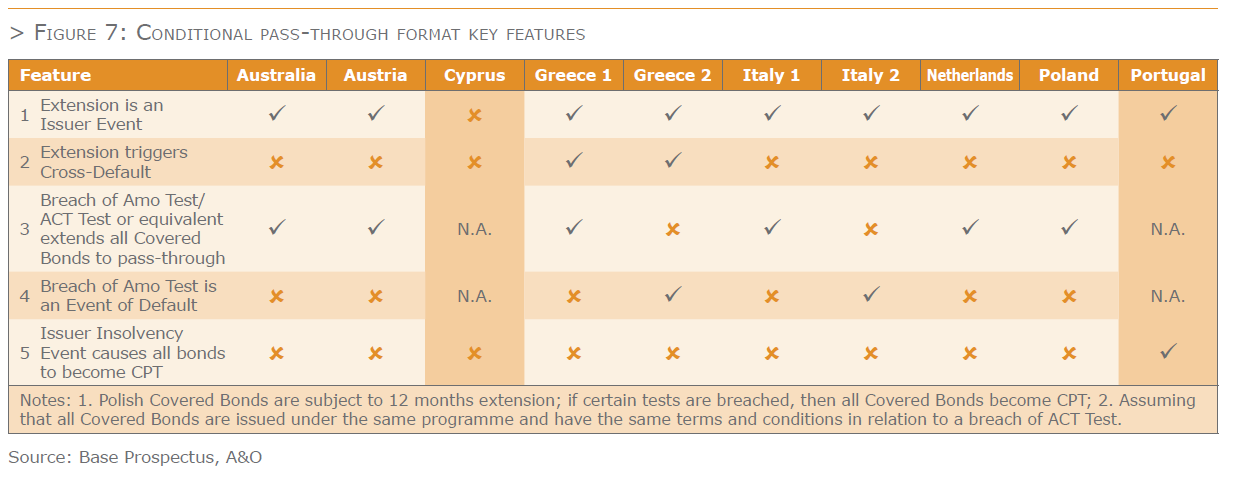

The increased number of CPT programmes in the past few years has led to a relatively broad diversity of structures (Figure 7), for example showing different extension triggers and procedures following the failure of the amortisation test. While within countries like the Netherlands, CPT structures are relatively homogenous, they are less homogenous in Italy, Greece and Portugal and differ quite substantially between countries. It will be interesting to see if the transposition of the new Directive will reduce some of the differences we have seen across the numerous CPT structures currently in the market.

The decisive difference between soft bullet redemption formats and (conditional) pass-through formats raises the question of the length of the deferral term. The longer the deferral period of the soft bullet payment regime, the closer the two redemption formats become. The remaining differences are not essential and could be replicated: the (implicit) SARA clause (Selected Asset Required Amount) is also frequently found in soft bullet structures. Thus, during the deferral period, the scope of actions taken by each cover pool administrator is quite similar: both will not hold on to an unnecessary amount of liquidity but will instead use it to redeem the deferred principal amount. Furthermore, both will try and find opportunities to liquidate assets (in line with the SARA clause) in order to allow redemption to occur as quickly as possible.

However, the one-year deferral period of most soft bullet covered bonds provides the cover pool administrator with a relatively limited timeframe in which the required amount of cover pool assets can be liquidated. In contrast, the opportunities in a (conditional) pass-through case are technically unlimited. Hence, market risk is mitigated with soft bullets covered bonds and eliminated with CPTCBs.

The harmonisation of covered bond frameworks via the national implementation of the new covered bond Directive should result in a less fragmented market in which investors will be even better protected, while the high quality of the covered bond product is safeguarded. By doing so, there will likely also be more clarity and transparency about covered bonds with extendable maturity triggers, also further strengthening the covered bond product.

The European Covered Bond Council (ECBC) is the platform that brings together covered bond market participants including covered bond issuers, analysts, investment bankers, rating agencies and a wide range of interested stakeholders.