ECB POLICY MEASURES AND COVERED BONDS: A MOVING FINISH LINE

By Matthias Melms, NordLB, Franz Rudolf, UniCredit and Maureen Schuller, ING Bank

EXECUTIVE SUMMARY

The European Central Bank (ECB) perhaps has had the most prominent influence on the covered bond market throughout the past decade. Be it as a buyer of covered bonds, by granting banks access to central bank funding at favourable conditions, or by setting standards for collateral eligibility, the ECB has, for many years, defined the key performance and supply parameters for the covered bond market and continues to do so. The covered bond purchase programme is probably the non-standard monetary policy measure most discussed.Initiated in September 2014 by the ECB and later embedded in a broader asset purchase program, net purchases of the covered bond purchase programme (CBPP) ended in December 2018, with the reinvestment phase ongoing since January 2019. The programme has been a major driver for the covered bond market since its implementation. This article addresses the criteria and mechanism of the purchase programme, but also discusses the ECB’s targeted longer-term refinancing operations (TLTROs). The article concludes with the use of covered bonds as collateral for ECB refinancing operations.

COVERED BOND PURCHASE PROGRAMME 3

The reinvestment phase

On 13 December 2018, the Governing Council of the European Central Bank (ECB) decided to end the net purchases under the APP in December 2018 and announced that it “intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation”.

Following the announced end of net purchases under the CBPP3, since January 2019, the reinvestment phase of the CBPP3 as part of the APP has started. The Eurosystem aims to maintain the size of cumulative net purchases under each constituent programme of the APP, e.g. the CBPP3, at the level attained at the end of December 2018. The holdings of the CBPP3 as of year-end 2018 were EUR 262.2 bn. During the reinvestment phase, the Eurosystem continues to adhere to the principle of market neutrality via smooth and flexible implementation and as a result limited temporary deviations from this level may occur. Market capitalisation continues to be the guiding principle for reinvestment purchases of covered bonds. Purchases of securities in primary markets continue to be permitted as necessary.

Since January 2019, the Eurosystem no longer conducts net purchases, but continues to reinvest the principal payments from maturing securities held in the CBPP3 portfolio. The amount of holdings as of end-June 2019 was EUR 261.3 bn. The holdings are calculated incorporating monthly net reinvestments as well as quarter-end amortisation adjustments. Data on the amount of CBPP3 holdings are published ex post on a weekly basis.

{kind=link}

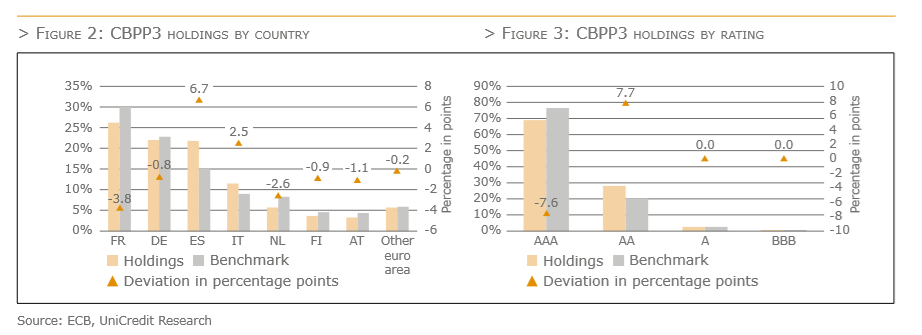

In March 2019, the ECB has released for the first time a description of the distribution of its CBPP3 holdings by country and rating. It shows a deviation between actual holdings and the market capitalization of specific countries.

The ECB stated that CBPP3 purchases were broadly oriented towards a market-capitalisation-based benchmark of eligible securities, with due consideration being given to market liquidity conditions. The ECB published information on actual holdings compared to a benchmark. The benchmark is constructed using the universe of eligible securities pertaining at the end of 2018. The weighting assigned to certain covered bond classes was adjusted lower to reflect bonds’ lack of availability and illiquidity, and only bonds with an asset rating were included in the data used to construct the credit-rating distribution. The ratings are first-best-asset ratings, and the distributions are arranged by nominal value. According to the ECB, the market-capitalisation approach evolved over time, with the benchmark weighting attached to certain securities decreasing as some covered bond categories were found to be increasingly hard to purchase. For example, the launch of TLTRO-II increased the attractiveness of retaining covered bonds as collateral rather than placing them in the market. To account for this, the relative weighting assigned to retained covered bonds was reduced in the CBPP3-eligible benchmark by the ECB.

The disclosure of holdings by country and rating showed that, as of the end of 2018, France, Germany, the Netherlands, Finland and Austria were underrepresented in comparison to their market capitalisation, while holdings in Spanish and Italian covered bonds exceeded the benchmark. The same picture is reflected with respect to ratings. While covered bonds with a triple-A rating were underrepresented by 3.8 percentage points, the rating category double-A was 7.7bp above the benchmark.

{kind=link}

Background and facts

On 4 September 2014, the European Central Bank (ECB) announced its plan to buy covered bonds. This CBPP came as a surprise to markets at that time and was the third covered bond purchase programme besides the CBPP1 (from July 2009 to June 2010) and the CBPP2 (from November 2011 to October 2012). Purchases of the CBPP3 started at the end of October 2014. The CBPP3 programme was originally scheduled until October 2016. In January 2015, however, it was embedded in a broader Asset Purchase Programme (APP), including sovereign debt, international and supranational institutions and agencies as well as asset-backed securities with a monthly target volume of EUR 60 bn. In December 2015, the ECB asset purchase programme was extended to March 2017 and the monthly volume was increased to EUR 80 bn in March 2016, including also corporate bonds from June 2016 onwards. After two years in operation, the ECB announced in December 2016, that from April 2017 onwards, monthly purchases under the APP are reduced to EUR 60 bn from previously EUR 80 bn, while at the same time extending the term of the programme until year-end 2017. In October 2017, the ECB announced to extend the programme until September 2018 with monthly purchases lowered to EUR 30 bn from EUR 60 bn previously. Finally, in June 2018, the ECB decided to extend the programme by another three months and to reduce monthly purchases further to EUR 15 bn. Purchases ended at the end of December 2018 and the re-investment phase started.

{kind=link}

The ECB’s rational is that alongside the public sector programme (PSPP), the asset-backed securities purchase programme (ABSPP), the corporate sector purchase programme (CSPP) and the targeted longer-term refinancing operations (TLTROs), the CBPP3 will further enhance the transmission of monetary policy, facilitate credit provision to the euro area economy, generate positive spill-overs to other markets and, as a result, ease the ECB’s monetary policy stance, and contribute to a return of inflation rates to levels closer to 2%. The purchases are conducted in both primary and secondary markets in a uniform and decentralised manner, meaning that the Eurosystem central banks purchase eligible covered bonds from eligible counterparties.

In order to qualify for purchase under the programme, covered bonds must fulfil the following eligibility criteria:

Be eligible for monetary policy operations in line with section 6.2.1 of Annex I to Guideline ECB/2011/14 (eligibility criteria for marketable assets) and, in addition, fulfil the conditions for their acceptance as own-used collateral as laid out in section 6.2.3.2. (fifth paragraph) of Annex I to Guideline ECB/2011/14.

> Be issued by euro area credit institutions; or, in the case of multi-cédulas, by special purpose vehicles incorporated in the euro area.

> Be denominated in euro and held and settled in the euro area.

> Have underlying assets that include exposure to private and/or public entities.

> Have a minimum first-best credit assessment of credit quality step 3 (CQS3; BBB- or equivalent) by at least one rating agency.

> For covered bond programmes which currently do not achieve the CQS3 rating in Cyprus and Greece, a minimum asset rating at the level of the maximum achievable covered bond rating defined for the jurisdiction will be required for as long as the Eurosystem’s minimum credit quality threshold is not applied in the collateral eligibility requirements for marketable debt instruments issued or guaranteed by the Greek or Cypriot governments, with the following additional risk mitigants: (i) monthly reporting of the pool and asset characteristics; (ii) minimum committed overcollateralisation of 25%; (iii) currency hedges with at least BBB- rated counterparties for non-euro-denominated claims included in the cover pool of the programme or, alternatively, that at least 95% of the assets are denominated in euro; and (iv) claims must be against debtors domiciled in the euro area.

> Covered bonds issued by entities suspended from Eurosystem credit operations are excluded for the duration of the suspension.

> Counterparties eligible to participate in CBPP3 are those counterparties that are eligible for the Eurosystem’s monetary policy operations, together with any of the counterparties that are used by the Eurosystem for the investment of its euro-denominated portfolios.

> The Eurosystem will apply an issue share limit of 70% per ISIN (joint holdings under CBPP1, CBPP2 and CBPP3), except in the case of covered bonds issued by issuers in Greece and Cyprus and not fulfilling the CQS3 rating requirement; for such covered bonds, an issue share limit of 30% per ISIN will be applied.

> Covered bonds retained by their issuer shall be eligible for purchases under the CBPP3, provided that they fulfil the eligibility criteria as specified.

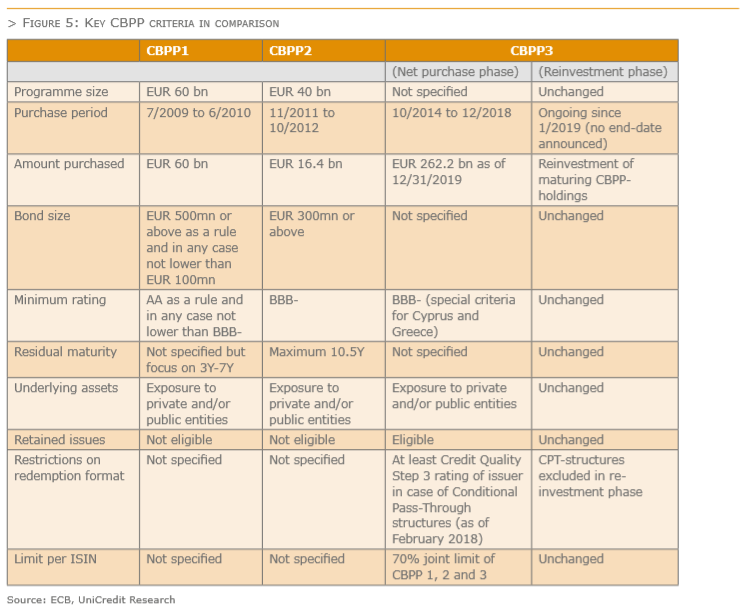

>Since February 2018: In case of conditional pass-through covered bonds, the issuing entity must have a first-best issuer rating of at least credit quality step 3. During the reinvestment phase, CPT covered bonds are no longer eligible.Furthermore, the Governing Council has decided to make its CBPP3 portfolio available for lending. Lending will be voluntary and conducted through security lending facilities offered by central securities depositories, or via matched repo transactions with the same set of eligible counter parties as for CBPP3 purchases. Compared to the CBPP1 and CBPP2, the current purchase programme (CBPP3) did not apply any minimum size or any specific maturity of the covered bonds purchased.

Previous covered bond purchase programmes

In June 2009, the ECB had announced its first covered bond Purchase programme (CBPP1) with a volume of EUR 60 bn – with purchases between July 2009 and June 2010. The programme was fully used with a nominal value of EUR 60 bn, and, in total, 422 different bonds were purchased, 27% in the primary market and 73% in the secondary market. The Eurosystem mainly purchased covered bonds with maturities of three to seven years, which resulted in an average modified duration of 4.12 for the portfolio as of June 2010. In November 2011, the ECB launched its second covered bond purchase programme (CBPP2) with a programme size of EUR 40 bn and eligible covered bonds to be purchased up until October 2012. However, cumulative purchases reached only a volume of EUR 16.4 bn, of which 36.7% related to the primary market and 63.3% to secondary markets.

{kind=link}

A key difference during the reinvestment phase since January 2019 compared to the net-purchase phase of the CBPP3 (from October 2014 to December 2018) is the eligibility of conditional pass-through (CPT) covered bonds. In December 2018, the Governing Council decided to exclude conditional pass-through covered bonds from purchases under the CBPP3, as of the end of the net purchase phase. The decision reflects their somewhat more complex structure, whereby some pre-defined events may lead to an extension of a bond’s maturity and to a switch in the payment structure, according to the ECB.

As of 28 June 2019, the ECB reported covered bond holdings of EUR 261.29 bn under the CBPP3 at amortised cost, deriving from primary market (37.8%) and secondary market sources (62.2%). In addition, the remaining holdings from terminated covered bond purchase programmes were reported as EUR 2.95 bn under the CBPP1 and EUR 3.43 bn under the CBPP2.

THE (T)LTROS: ANOTHER IMPORTANT DRIVER TO COVERED BONDS

The ECB’s major policy announcements of the past five years:1) 5 June 2014 – The ECB cuts the deposit rate to negative territory at -0.1%, while at the same time announcing the TLTRO-I operations and indicating to intensify the preparatory work related to theout right purchases of asset backed securities.2) 4 September 2014 – The ECB announced intentions to start buying covered bonds under the CBPP33) 22 January 2015 – The ECB announced that it would expand the asset purchase programme to include government bonds and SSAs. The total programme size was calibrated at EUR 60 bn.4) 10 March 2016 – The announcement to expand the asset purchase programme to include corporate bonds, a new round of TLTROs, the lowering of the deposit rate to -0.4% and an increase in the sizeof the programme from EUR 60 bn to EUR 80 bn.5) 8 December 2016 – The ECB announced intentions to extend the term of the programme until the end of 2017 (from March 2017), while reducing the size of the programme to EUR 60 bn as of April 2017, and to allow purchases to be made at a rate below the -0.4% deposit rate.6) 26 October 2017 – The ECB confirmed to lower its monthly asset purchases from EUR 60 bn to EUR30 bn as of January 2018, but at the same time extended the duration of the net asset purchases by nine months until the end of September 2018.7) 26 July 2018 – The ECB resets its monthly asset purchases from EUR 30 bn to EUR 15 bn as of September2018 until the end of December 20188) 13 December 2018 – The ECB confirms to end its net monthly asset purchases after December 2018,with intentions to continue reinvesting in full redemptions for an extended period of time past thedate when the ECB starts raising its key interest rates.9) 7 March 2019 – The ECB announces a new series of quarterly TLTROs, starting September 2019 and ending in March 2021. The forward guidance on (stable) rates was changed to at least through the end of 2019 from at least through the summer of 2019.

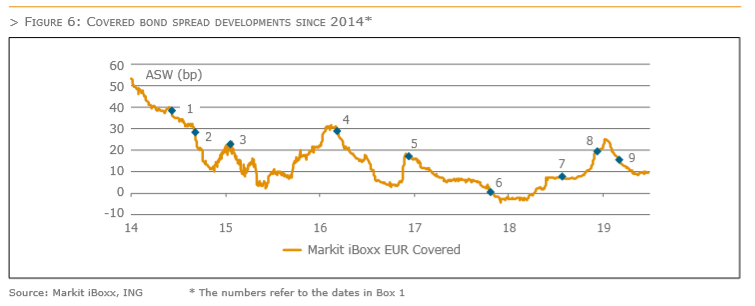

On 7 March 2019, the ECB announced to start a new series of TLTROs (TLTRO-III). At the same time, the central bank indicated to leave rates on hold at least through to the end of 2019. The “stable rates” forward guidance was changed again in June 2019 to the first half of 2020. The announcements in March did not come as a surprise to financial markets. Less than one month after ending its net APP purchases the ECB first indicated that the economic data were weaker than anticipated, thwarting the 2018 spread widening in covered bonds (see figure 6).

{kind=link}

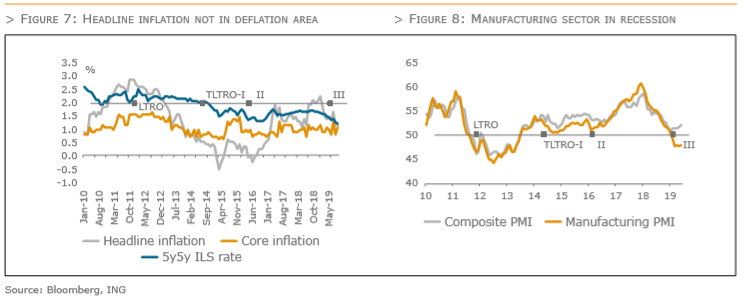

The timing of the TLTRO-III announcements in March 2019 looked more preemptive compared to the previous two TLTRO statements. Headline inflation was not yet near the low levels seen at the time of announcement of the TLTRO-I and II. However, inflation expectations, as measured by the 5y5y ILS rate, were at almost unprecedented low levels. At the same time the purchasing managers’ index for the Eurozone manufacturing sector was about to crossover the 50 mark indicating negative growth. Both measures signalled that headline inflation could move further away from the lower than but close to 2% inflation target, delaying a further scaling back of the non-standard monetary policy measures.

{kind=link}

The details

The purpose of the new round of TLTROs remains unchanged. By offering banks longer term funding at attractive conditions, the ECB aims to preserve favourable bank lending conditions and enhance the transmission of monetary policy. The ECB will conduct the new series of quarterly TLTROs (TLTRO-III) from September 2019 through to March 2021, each with a shorter maturity of two years compared to the four year maturity of the TLTRO-II tranches. Banks are entitled to borrow 30% of their stock of eligible loans at 28 February 2019, reduced for TLTRO-II amounts still outstanding. Maximum 10% of the eligible loan amount can be borrowed under each of the seven new operations. Drawings under the TLTRO-III cannot be repaid on a voluntary basis before maturity, reflecting the shorter 2yr term of the TLTRO-III operations. The previous two TLTRO operations did allow for early repayments after two years and up to final maturity date of the tranches.

The rate on the TLTRO-III tranches will be indexed to the rate on the main refinancing operations. Banks can borrow at 10bp above the average MRO rate (0% at the end of June 2019) over the life of each operation. When banks exceed their lending benchmark between the end of March 2019 and end of March 2021, an interest rate as low as the average deposit facility rate (-0.4% on 30 June 2019) plus 10bp may apply. The interest rate will be communicated in September 2021. The reference to the average MRO rate makes the TLTRO-III conditions adjustable to ECB rate changes. This differs from the TLTRO-II where the rate was fixed at the MRO rate at the time of the allotment.

Banks will only benefit from the maximum rate of reduction if they exceed their benchmark stock of eligible loans by 2.5% at 31 March 2021. Below this target the decrease in the interest rate will be linearly dependent upon the percentage by which the benchmark stock of eligible loans is in fact exceeded. The benchmark lending is set at 0 for banks with positive net lending in the 12-months to 31 March 2019. For banks with negative net lending in this 12-month period, the benchmark net lending is equal to the eligible net lending in that period. At the time of writing the technical details on the eligible lending had yet to be announced. If similar to the

TLTRO-I and II, eligible loans would include loans to non-financial corporations and households excluding loans for house purchases.

The prospects for TLTRO-III borrowing

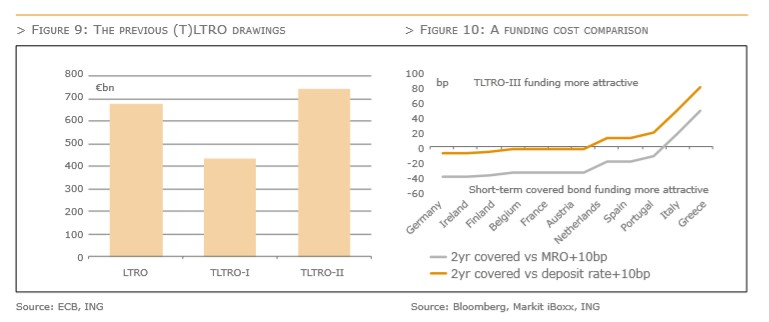

Drawings under the ECB’s longer term refinancing operations have thus far been highest under the TLTRO-II (figure 9). This has two reasons: a) the terms of the TLTRO-II in comparison to the TLTRO-I were less restrictive, while b) the economic considerations of borrowing via the ECB became far more important to banks than the alleged stigma of holding sizeable amounts of (T)LTRO debt.

The conditions for the TLTRO-III will remain favourable for banks to attract funding under the central bank’s longer-term refinancing operations. Nonetheless, drawings may not easily reach a similar EUR 740 bn level as for the TLTRO-II. For instance, for some banks the funding cost advantages over covered bonds are less than at the time of the TLTRO-II drawings (the weighted average interest rate applied was -0.365% for these drawings).

The TLTRO-III interest rate will be 10bp higher than for the TLTRO-II tranches if the ECB keeps rates unchanged. Only if the ECB decides to cut the deposit rate by 10bp or more, the conditions may match or become more favourable than for the TLTRO-II. The negative 2yr swap rate levels at the end of June 2019 together with aggregate covered bond spreads of 0bp to 5bp for core Eurozone markets, suggest that short-term funding via covered bonds, for instance, could for some banks be more interesting than TLTRO-III funding, unless the deposit rate were to be cut by 10bp or more. Having said that, we don’t consider covered bonds to be the most logical short-term funding alternative for TLTRO debt, as we will discuss later in this article.

{kind=link}

Having said that, of the original EUR 740 bn drawings, banks still have a substantial EUR 689 bn in TLTRO-II debt left outstanding to either repay or replace with TLTRO-III debt. Even on 26 June 2019 Eurozone banks repaid only EUR 26 bn in TLTRO-II debt, despite the fact that the first tranche lost 50% of its net stable funding recognition that month. This suggests that banks are willing to hold on to cheap TLTRO-II funding for as long as they can and, in any event, for the short (50% NSFR) overlap period in anticipation of the first opportunity to rollover TLTRO-II debt into the TLTRO-III as of September 2019.

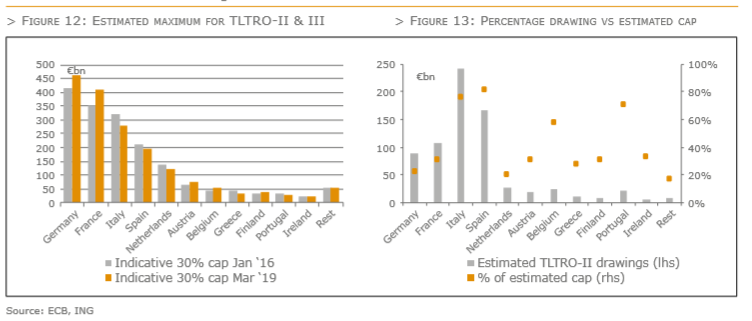

Similar to the last round of TLTROs, banks can borrow up to 30% of the eligible loans. Figure 12 gives an indication of the caps of TLTRO-III drawings versus TLTRO-II with reference to ECB country statistics on a) loans to non-financial corporations and b) loans to households in the form of consumer credit and other loans (i.e. excluding loans to households for house purchases). This analysis assumes that the definition for “eligible loans” remains similar to the previous TLTROs.

Figure 13 plots the percentages of drawings per country under the TLTRO-II versus the estimated maximum. A roughly similar percentage of drawings versus the estimated 30% TLTRO-III drawing potential (adjusted for TLTRO-II debt left outstanding) could see the EUR 690 bn in TLTRO-II debt left outstanding on 30 June 2019 be fully rolled over in TLTRO-III debt. This would likely somewhat overestimate the ultimate rollover amount. Namely, Southern European banking sectors that attracted most TLTRO-II funding now have lower loan balances and refinancing needs and at the same time do strive to attract funding allowing them to meet their MREL requirements. Furthermore, to core Eurozone banks, which are also still in the process of meeting their MREL requirements, the funding cost advantages of TLTRO-III drawings may look less appealing compared to 2016 and 2017 when they participated in the TLTRO-II. This may hold in particular for banks that question their abilities to show sufficient lending growth in the event of slower economic growth.

{kind=link}

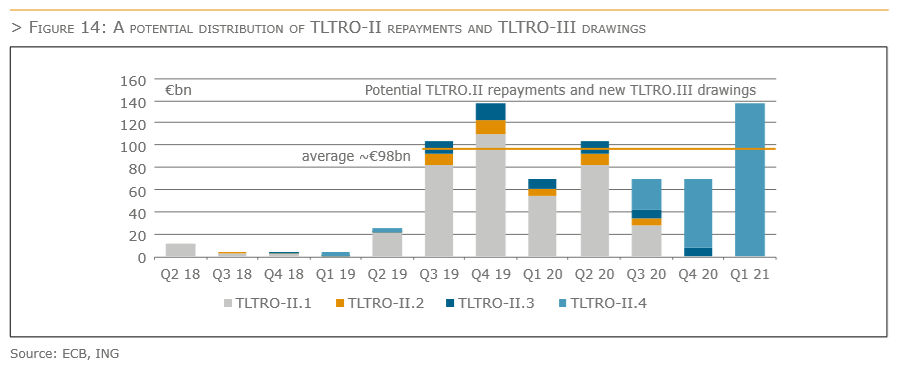

The seven opportunities to borrow under the TLTRO-III, starting September this year, exactly match the seven repayment options left for outstanding TLTRO-II debt. Banks will make their rolling decision against the backdrop of different considerations: a) the (partial) loss of net stable funding recognition of the existing TLTRO tranches, where deemed relevant, b) the shorter 2yr term of the new TLTRO-III tranches with no voluntary repayment options before maturity, c) the, at current rates, 10bp less favourable funding rate of the TLTRO-III, d) the fact that the reference MRO under the TLTRO-III will be adjusted with ECB rate changes and e) a maximum 10% of the eligible loan amount can be borrowed under each of the seven new operations. These may spread the TLTRO-III borrowings more evenly across the tranches than under the TLTRO-II. Namely, after replacing their TLTRO-I debt by TLTRO-II debt at the first opportunity, banks primarily sourced funding from the TLTRO-II’s final tranche to optimise the length of use of the facility.

Any rate cut by the ECB will make the decision to rollover TLTRO-II into TLTRO-III debt at the first opportunity at least rate neutral subject to the condition that banks show sufficient lending growth. NSFR considerations may prompt banks to rollover more at year end 2019 when the net stable funding credit for the first tranche drops to zero. There are no voluntary repayment options for the TLTRO-III. Hence, banks will try to avoid repayment spikes by spreading their TLTRO-III drawings. At the same time banks would benefit longest from the TLTRO-III if they borrow more at the last opportunity in March 2021. Figure 14 gives an indicative profile for TLTRO-II repayments and their potential replacement with new

TLTRO-III drawings after considering all these dynamics.

{kind=link}

The impact on covered bond supply

Albeit not discussed in greater detail here, covered bond supply has historically been impacted more than senior unsecured supply by the ECB’s longer-term refinancing operations. However, different dynamics may be at play this time around.

First of all, the opportunity to rollover TLTRO-II into TLTRO-III drawings should be more or less bank supply neutral versus current conditions. Even banks that did borrow up to their 30% cap during the previous rounds of TLTRO-II and have seen their loan balances, and as such the benchmark reference, decline, may not have to resort to other sources of funding. After all, the lower eligible loan balances should mostly be cancelled out by a lower refinancing need if they are a reflection of balance sheet declines. Furthermore, the 2yr maturity of TLTRO-III tranches is shorter, while the rate on TLTRO-III borrowings is adjustable to changes in the MRO or deposit rate. If any, this may impact preferred senior unsecured supply more that covered bond supply. Particularly the floating rate preferred senior issuance tends to focus on the 2-3yr area and therefore has the strongest overlap with the characteristics of the TLTRO-III.

Covered bonds will remain the funding instrument of choice for longer term funding. In the end, longer maturity covered bonds still make the most optimal funding match with the longer duration assets securing the bonds. The deeply negative rates at the front end of the curve also remains an incentive for banks to issue in maturity buckets where yield levels (and preferably asset swap spread levels) are positive. Covered bonds are proportionally less expensive for issuers than other bank bond instruments in the long end.

The housing market lending growth in core Eurozone jurisdictions is also likely to keep covered bond supply at decent levels. This will partly neutralise any dampening supply implications of the TLTRO-III.

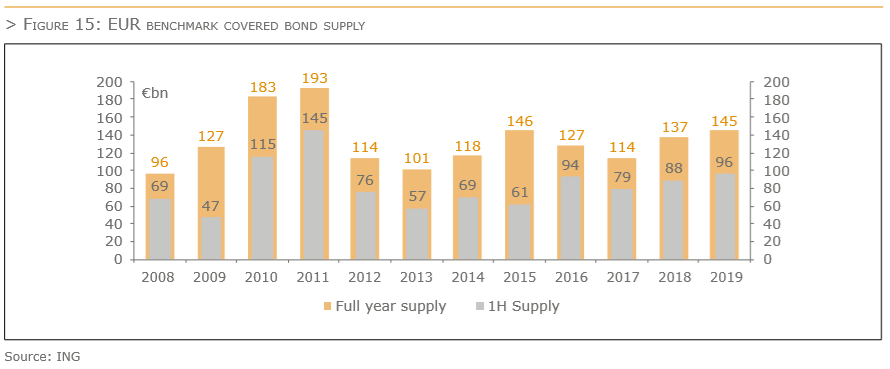

Thus far the ECB’s announcement of a new round of TLTROs has indeed had limited implications for the pace of covered bond supply. In the first half of this year, EUR benchmark covered bond supply ran slightly ahead of last year. Similar issuance as in the second half of last year, could see covered bond supply touch EUR 145 bn in 2019. This would confirm a steady annual growth in EUR covered bond supply since 2017, the year that banks enthusiastically seized their final opportunity to attract funding under the TLTRO-II.

{kind=link}

COVERED BONDS AS COLLATERAL IN REPO TRANSACTIONS WITH THE ECB

Covered bonds are often regarded as eligible by central banks

For credit institutions, the provision of collateral is a highly important criterion in the course of borrowing from central banks. In this context, central banks – such as the ECB – also attach great importance to covered bonds as marketable financial securities. Covered bonds, for example, are defined as eligible assets in the ECB collateral framework and can be deposited as collateral with the ECB when the relevant criteria are met. Furthermore, the eligibility of covered bonds as collateral for central banks is a necessary condition for many investors, which has to be met in their allocation process. In this context, it should also be noted that covered bonds are a global product by now. This has been made evident not least in the ECBC’s annual statistics, which at the end of 2017 indicated a distribution of the outstanding covered bond volume (EUR 2,460 bn) across a total of 29 jurisdictions. This globalization of the product can also be seen from the perspective of covered bond investors.

Transparency plays an important role: both for market participants and for central banks

In addition, the ECB specifies transparency requirements tailored specifically for the purpose of the collateral class of covered bonds. If, for example, the external rating agencies fail to comply with the prevailing obligations to provide information on covered bond ratings in the context of the ECB collateral framework, there is a risk of a step up of the collateral discounts in the form of haircuts. However, the ECB, on the other hand, also ensures a certain degree of transparency by providing information on securities recognised as collateral a) in the form of lists on an ISIN basis or b) by allowing individual queries at the securities level in order to provide financial market participants with information on securities that are currently suitable as collateral for central bank transactions. In this context, it should be noted that the lists of eligible assets published by the ECB are not equivalent to the securities actually deposited as collateral (collateral used). In addition, the central banks generally require a registration or application before securities can be regarded as eligible assets or used as collateral. Even though newly issued bonds are often registered with the central bank concerned by one of the mandated credit institutions, especially in the case of publicly placed covered bonds, this is by no means an automatic process. Nevertheless, the central banks’ data compilations allow trend statements to be made on the significance of covered bonds in the respective collateral frameworks of the monetary policy institutions examined. Irrespective of this, almost every central bank reserves the right to admit or reject securities as collateral or – in some cases – makes haircut adjustments at its own discretion and – in part – also independently of the criteria listed below.

Euro area – European central bank

Covered bonds have a high priority in the collateral framework of the European Central Bank and the system of European central banks, which is due not least to the comparatively low credit risk of covered bonds. Overall, the requirements with regard to assets suitable for ECB collateral management are documented extensively and in detail and are basically laid down in Guideline (EU) 2015/510, which has been amended by various other guidelines in recent years. The essential requirements can also be found in the Eligibility Criteria for Marketable Assets or the General Framework, which are supplemented or overruled by the ECB’s so-called Temporary Frameworks.

ECB criteria allow for a wide range of international covered bonds

The ECB’s criteria for marketable assets allow for a broad range of covered bonds as collateral. In principle, central bank eligibility applies to euro-denominated investment grade covered bonds from the European Economic Area (EEA). On the basis of the ECB’s temporary guidelines, this sp