30 November 2021

by Luca Bertalot, EMF-ECBC Secretary General and EEMI Coordinator

The latest Report of the United Nations Intergovernmental Panel on Climate Change, published in August 2021, is simply and shockingly a wakeup call to the world. The Report reiterates that the clock is ticking ever louder and that we are about to reach the point of no return with regards to mitigating the human activity-related causes of climate change.

Since the Paris Agreement of 2015, which set out a global framework to avoid dangerous climate change by limiting global warming to well below 2°C and pursuing efforts to limit it to 1.5°C, it has been argued that it will take time for societies to adapt and put in place the mechanisms needed to achieve these objectives. We are now almost six years further down the road, edging ever closer towards the cliff edge, and this argument is beginning to lose credibility. As the IPCC makes clear, there is no longer scope for further hesitation and postponement of the decisions that must be taken.

Every stakeholder in our societies and our economies, whether as a private consumer and citizen, or as a representative of an organisation or business must act now to put in place the tools to reach the Paris Agreement’s goals. There is ever-strengthening consensus that whatever the forecasted financial costs of taking the actions required now are, the costs – financial and societal – of further delay far outweigh these.

As the voice of the mortgage credit and covered bond industries, we are acutely aware that the prospects for future generations are in our hands today and that we have a moral obligation to play our part in limiting climate change.

The EMF-ECBC seeks to be part of the solution here and, together with our Energy Efficient Mortgages Initiative (EEMI), from the onset of the pandemic activated the mortgage industry’s best resources to monitor, analyse and guard against potentially negative impacts on mortgage, housing and funding markets in Europe.

Over recent years, the EMF-ECBC has sought to channel the industry’s reflections on sustainability to national, European, and global authorities, including its concerns regarding the potential impact of sustainability related issues, such as the taxonomy, and made concrete proposals regarding possible ways forward. As a community, we are committed to providing economic impetus towards a transition economy, encouraging countries to move from a pandemic mind-set towards a more sustainable capital markets infrastructure, and supporting consumers and borrowers in turning the current challenges into opportunities. The spaces we occupy need to be able to adapt to different social uses, to new functions over time, without the need to constantly destroy and then rebuild them.

We need to use our imagination, to develop visions and ideas of what the European private and public space should look like. This is clearly an opportunity to change not only finance and banking, but urban planning, construction, manufacturing – in short, to change the way we live. But this needs to be a comprehensive cultural project. This is a unique opportunity to bring attention and momentum to the European Green Deal.

During the COVID-19 pandemic, we have come to accept that remote working really is both possible and effective in many sectors. As a consequence, many people are now looking at ways to leave cities to find a greener, more open and more socially distanced space to live and work in. This does not mean that we will completely abandon cities – not everyone will or can leave, but things will change. More importantly, this tells us that people are thinking more profoundly about what it really means to have a good place to live, what are the attributes of a home that really matter to them. Healthy homes, healthy cities, greener spaces where trees absorb CO2, the way in which we build, the materials we use and how we maintain our buildings – these are increasingly the factors that count.

We are entering a new age of banking, of constructing and operating buildings where digitalisation is changing everything. We talk about and start to see autonomous cars. What about autonomous houses with sophisticated sensors that can adapt to ambient temperature, humidity, to the presence of people, adapting spaces and minimising energy consumption? What about intelligent neighbourhoods or villages where communities share energy or other resources? This is an age where we need to combine high tech and no tech, artificial intelligence and nature.

We believe that a green market ecosystem, with ESG covered bonds, Energy Efficient Mortgages, green European Secured Notes (ESNs), is paving the way for a green Industry roadmap.

If Europe and the world really want to achieve net zero emissions, we need to reduce buildings’ emissions, transform the way we inhabit our homes and our cities, and rethink mega infrastructures, energy infrastructures and mobility infrastructures. The way we finance these activities can influence this shift.

Whilst we could close our eyes and wait for the world to go back to its pre-pandemic norms, in reality we cannot ignore the strength of the winds of change blowing through our lives, our societies and our economies. We have all witnessed radical shifts in our daily life and business activities, some have been negative and others positive, and there is now a broad acceptance that we are in the midst of a generational turning-point. Indeed, we all know that more changes must come as the full impacts and consequences of the pandemic continue to reverberate.

We believe that changing residential energy demands can play a key role in transitioning to a greener and more sustainable economy. Environmental psychology suggests that behavioural changes regarding energy use are affected by knowledge, awareness, motivation and social learning. Data on various behavioural drivers of change can explain energy use at the individual level.

Consequently, an environmental, social and governance (ESG) revolution in the financial sector can help to stimulate a green mentality in consumers and stakeholders. In the same way, the building of a new ecosystem of energy efficient financial tools can have significant implications for macro-energy demands at a regional and national level.

There are a number of actions households can pursue individually which impact their energy footprint. We categorise these into three main types of energy-related behavioural changes:

1) investments;

2) energy conservation; and

3) switching suppliers.

A household could make an investment: either large, such as the installation of solar panels and/or insulation etc., or small, such as buying more energy efficient electrical appliances. The latest research indicates that today, on average, the level of investment required in order to make an improvement of two notches in a house’s energy rating is in the range of €20,000-€30,000. This would be expected to result in an energy bill saving of somewhere in the range of 50%-70%. Alternatively, households may seek to reduce their energy consumption by changing their daily routines and habits: by adjusting their heating thermostats downwards or by systematically completely switching off unused electrical appliances.

Finally, households could change to an energy supplier that provides independently certified green electricity. We believe that a new housing market ecosystem featuring a collaborative effort from multi-sectoral suppliers, utilities and banks, could provide all of these solutions to consumers.

Indeed, the nexus between our private interests and civil society is our home. The Ancient Greek word “oikos” (home) is at the heart of the word “oikonomia” (economy). Drawing inspiration from this, we believe that a sustainable economy has to be built around the concept of the home and centred on an ecosystem that promotes green values and raises environmental, social and governance awareness.

At this unprecedented time, civil society is called to action to design and shape a better future for the next generations. Climate change indiscriminately affects every region of the planet and therefore calls for a global and comprehensive approach, one that the EU can help to lead. Despite the challenge represented by the COVID-19 pandemic and the resulting economic crisis, which has required gigantic efforts of both national and European policymakers over the last two years, the European Institutions have set highly ambitious targets to fight climate change, seeking to turn the Old Continent into the first carbon-neutral economic area by 2050.

In this context, the EU is committed to reduce its own primary energy consumption by 32% by 2030, as witnessed with the adoption of the Green Deal in 2019, further complemented in October 2020 with the Renovation Wave Strategy and in April 2021 with the EU Taxonomy. Both the latter provisions encompass the building sector, globally identified as one of the main producers of CO2 emissions. Nevertheless, these legally enshrined efforts need to be supported by adequate funding schemes, as the scale of investment required to meet the energy savings targets alone is estimated to be in excess of €200 billion per year, three-quarters of which is accounted for by energy efficiency in buildings.

Moreover, within this framework, the financial services sector covers a non-secondary position considering that the achievement of the sustainability of the industry must play a crucial role in the transition to a climate-neutral economy. In particular, the mortgage credit and covered bond sectors have the potential to play a transformative role in relation to the attainment of the 2050 emissions targets for both the building and financial sectors.

This is precisely what the EU-funded Energy Efficient Mortgages Initiative (EEMI), launched five years ago, has been doing, by establishing a comprehensive ecosystem around Energy Efficient Mortgages through a pan-European market-led initiative, bringing together lending institutions, investors, utilities, and public authorities. The Initiative covers the whole scope of action in the energy efficiency improvement process, for the benefit of citizens, enterprises, and broader society.

Indeed, since 2016, the EEMI, which comprises of three inter-linked EU-funded Horizon 2020 Projects (see below) and is coordinated by the European Mortgage Federation-European Covered Bond Council (EMF-ECBC), has been leading market efforts together with a consortium of expert partners. With the EU’s households and businesses at its heart, the Initiative delivers the capabilities to support the financing of the renovation of the EU’s building stock, 35% of which is over 50 years old and almost 75% of which is energy inefficient.

More specifically, the EEMI is divided into three projects, comprehensively matching the European Commission’s own framework for climate and energy policies. The Initiative began with the Energy efficient Mortgages Action Plan (EeMAP), was followed by the Energy efficient Data Protocol and Portal (EeDaPP) and continues today with the Energy efficient Mortgage Market Implementation Plan (EeMMIP). Together, these projects represent the kingpins of EMF-ECBC’s mission: to finance the greening of the aging European building stock. This goal will be reached by providing, respectively:

Alongside the EEMI, the Energy Efficient Mortgage (EEM) Label is a new quality instrument allowing transparent identification of energy efficient mortgages for market stakeholders. The Label was launched in February 2021, with the support of the European Commission, and denotes a further effort that the EMF-ECBC is making towards the sustainable finance and real estate/building sectors, in compliance with the EU legal framework. Indeed, the Label allows easier access to energy efficiency financing, green bond markets, better tracking of EEM performance, provides greater transparency in relation to climate risks and portfolio resilience, and fights greenwashing.

The Label enables lending institutions that are committed to continuous progress and improvement initiatives to disclose energy efficiency related data through the Label’s Harmonised Disclosure Template (HDT) at least every quarter, and thereby jumpstart the investment and mortgage market for energy efficiency finance.

Amongst other relevant datapoints necessary to assess the credit quality of a mortgage issued by a financial institution to improve or to acquire residential or commercial real estate, the HDT also seeks to collect data which will allow assessment of the loan’s ESG quality. For the time being, data requirements on EPC, age structure of the relevant real estate, energy demand data, type of dwellings and the amount of new or existing real estate the portfolio covers are collected. Several of these datapoints have only just started to be collected by the financial institutions themselves and often there is little temporal depth available. Thanks to the EEMI, through the EEM Label, for the first time a transnational effort to produce comparable data via a harmonised template exists.

Currently this covers 30 financial institutions from 13 different jurisdictions, providing 37 labelled Energy Efficient Mortgage Products.

Amongst these, at the time of writing some institutions are already publishing initial ESG data and more are expected to do so shortly, with the bulk being expected to have some form of data disclosure available by the end of the year.

Ultimately, drawing on the extensive experience of the Covered Bond Label, the EEM Label is proposed as a market intervention to support recognition of and confidence in energy efficient mortgages and facilitate access to relevant, quality, and transparent information for market participants. The Label relies on the EeDaPP data protocol to develop a harmonised transparency template for the disclosure of mortgage products compliant with the Label criteria. The effort in creating a standardisation would, in due course, facilitate a revolution in investors’ ESG due diligence and enhance overall transparency in the EEM and bond markets.

What does an ESG revolution imply for the financial sector?

Well, we know that we can play a fundamental role in changing market best practices and in providing the real-life answer to this question. The answer could be simply that the banking sector is pivotal to helping fund the renovation wave through a systemic ESG approach, providing the cathartic boost for properties and the basics for accessing capital markets via green covered bonds and securitisations. We could say that every renovated home will pollute less, be less risky as an investment/asset, increase the disposable income of borrowers, enhancing the quality of our lives. All of this is feasible provided that we take the opportunity before us to build an ecosystem capable of delivering on citizens’ expectations. In parallel, we must develop a more efficient capital market infrastructure optimising the use of private capital and investments, thereby allowing public resources to be focused on those other social needs where only the State can act.

With a holistic approach looking at the entire value chain from the asset-side (the green property and loan) through to liabilities (the green covered bonds or securitisations), we can build a green catalysing mechanism on the balance sheets of banks and in investors’ portfolios. Potentially, every mortgage and loan can contain a seed that will germinate into part of the green recovery, motivating and helping consumers to improve the energy performance of their homes. This will trigger a cascade effect throughout the entire value chain, giving rise to a new, green ecosystem.

We have long witnessed steadily growing attention being paid by our members to the issuance of ESG and green bonds, which are becoming an increasingly important feature of the European financial landscape.

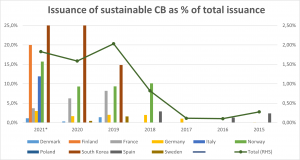

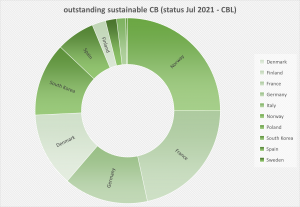

This is evidenced by the Covered Bond Label website, which now provides detailed transparency on green liabilities and cover assets. What started in 2017 as a simple self-certification[1] operation by labelled covered bond issuers to highlight (shown by a green leaf on the Covered Bond Label website) those of their bonds which are considered sustainable has now reached significant proportions: around 50 outstanding bonds in 10 jurisdictions[2] coming from 23 banks account for over EUR 30bn. of issuance.

This volume equates to roughly 1% of the total number of covered bonds outstanding at the end of 2020, and to 1.5% in terms of new issuances during the same period. For 2021, the figures available on the Covered Bond Label website suggest that around 1.8% of new issuances are sustainable covered bonds. In particular it is interesting to see that the Nordics, together with South Korea, are especially keen on this type of product. This being said, a number of other core covered bond countries as well as newer players, like Poland, have now also started to issue sustainable covered bonds as can be seen in the graph below.

Source: Covered Bond Label, Fact Book

Note: 2021 data are referring to year-to-month July 2021

Source: Covered Bond Label

Together with the Covered Bond Label, the EEM Label will not only facilitate compliance with the EU Taxonomy but, in the light of the EEMI’s demonstrated negative correlation between energy performance and credit risk, will help to reinforce financial stability and secure quality and transparency for market stakeholders in the gathering, processing and disclosure of EEM and ESG data. This will be key to further stimulating both EEM and ESG market developments and demonstrating the efforts that our sector is making to play its part in the fight to limit climate change.

Join us and help to build an energy efficient housing finance ecosystem suitable for future generations. To find out more about the role that housing finance can play in this transition, watch the video

[1] Through said self-certification the issuer declares that the bonds presenting a green leaf on the covered bond label website is “…a covered bond that is fully compliant with the Covered Bond Label Convention, and also includes a formal commitment by the issuer to use an amount equivalent to the proceeds of that same covered bond to (re)finance loans in clearly defined environmental (green), social or a combination of environmental and social (sustainable) criteria. Covered Bond Labelled sustainable covered bond programs are based on their issuer’s sustainable bond framework which has been verified by an independent external assessment. The issuer strives, on a best-efforts basis, to replace eligible assets that have matured or are redeemed before the maturity of the bond by other eligible assets.

[Against this background, please note that the EMF-ECBC is currently working on market initiatives which will ultimately define European criteria for energy efficiency covered bonds and sustainability standards]”

[2] Denmark, Finland, France, Germany, Italy, Norway, Poland, South Korea, Spain and Sweden

The European Covered Bond Council (ECBC) is the platform that brings together covered bond market participants including covered bond issuers, analysts, investment bankers, rating agencies and a wide range of interested stakeholders.