30 January 2024

Market overview:

A green covered bond is a bond where the proceeds (or an equivalent amount) are used to (re)finance in part or in full eligible green projects which meet specific green standards. The most popular format is a structure wherein mortgage loans to residential and/or commercial properties are (re)financed that meet certain sustainable criteria. However, we currently observe four exceptions in the market. Two issuers (re)finance green public sector loan assets, one issuer has (re)financed renewable energy loans in sub-benchmark size green format out of a Luxembourgish programme and one Swedish issuer refinances sustainable forestry.

ICMA’s Green Bond Principles:

In the absence of regulation, the green covered bond market adopted, in line with other debt capital market instruments, the principles and standards as set by ICMA in their Green Bond Principles (GBP). The GBP are voluntary guidelines and are intended for broad use by the market.

The latest version of the GBP was published on 10 June 2021. Appendix 1 of the GBP was updated in June 2022 to make a distinction between “Standard Green Use of Proceeds Bonds” (unsecured debt obligation) and “Secured Green Bonds” and to provide further guidance on green covered bonds.

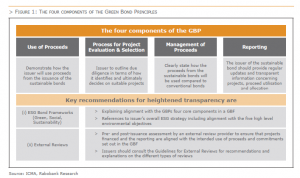

The GBP provide issuers guidance on the key components involved when issuing a green bond. Simultaneously, the GBP support investors by promoting the availability of information necessary to evaluate the environmental impact of their green bond investments. Furthermore, they assist underwriting banks by offering steps that help to preserve the market’s integrity. The GBP put emphasis on transparency and integrity of the information that is disclosed and reported by issuers through four core components and two key recommendations. The four core components for alignment with the GBP are:

(i) Use of Proceeds;

(ii) Process for Project Evaluation & Selection;

(iii) Management of Proceeds; and

(iv) Reporting

Additionally, ICMA promotes two recommendations for increased transparency. First of all, issuers should explain the alignment of their green bond with the abovementioned four core criteria in a Green Bond Framework (GBF). In doing so, issuers are encouraged to also incorporate any relevant information on their overall ESG strategy, including alignment with the five high-level environmental objectives.

Secondly, issuers are recommended to seek external review to confirm the alignment with the GBP’s four core components

See below figure 1 for a detailed overview of these components and the recommendations.

When analysing the largest and most active green covered bond programmes in the market, we observe that they all (i) claim compliance with the GBP, (ii) have a GBF in place (either on a covered bond programme level or on issuer level) and (iii) that they use external verification:

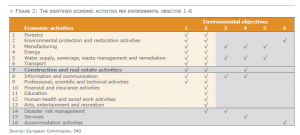

The GBP recognize five high level environmental objectives, to which a green bond can contribute:

Based on these five areas, the principles make reference to numerous possible project directions, without limiting them. With regard to the green covered bond universe, we currently observe the following categories:

Furthermore, ICMA has published a reference framework that helps parties to translate investment targets of to the so-called UN Sustainable Development Goals (SDGs). Market analysis shows that the following categories are the most popular among green covered bond issuers:

Most green mortgage covered bond issuers focus primarily on the goals of ‘Affordable and Clean Energy’ (SDG 7), ‘Sustainable Cities and Communities’ (SDG 11) and ‘Climate Action’ (SDG 13). Whereas green public sector covered bond issuers also include categories such as ‘Clean Water and Sanitation’ (SDG 6). ‘Affordable and Clean Energy’ (SDG 7), ‘Industry, Innovation and Infrastructure’ (SDG 9) and ‘Responsible Consumption and Production’ (SDG 12), in their use of proceeds.

Currently, almost all green covered bonds in the market are GBP based. It is important to note that the GBP are largely build on recommendations. When it comes to the eligibility criteria to define ‘green projects’, the GBP address these on a high-level basis. In doing so the definitions of green projects and ‘green’ may vary between issuers, jurisdictions, and sectors. This limits the comparability between GBP based green bonds to some extent. These shortcomings are covered under the EU Green Bond Standard (EU GBS). Whereas the GBP make only recommendations on the alignment of the proceeds with environmental goals, the EU GBS require clear alignment of the use of proceeds with eligible projects as defined under the EU Taxonomy.

The EU taxonomy regulation in a nutshell

The EU taxonomy regulation came into force in July 2020. It provides a unified classification system for sustainable activities and is an important pillar within the EU sustainable finance framework.

At this point, the EU taxonomy identifies six environmental objectives. An economic activity is considered environmentally sustainable and thus EU taxonomy aligned if it:

The climate delegated act of June 2021 sets the TSC for the climate mitigation and climate adaptation objectives (1-2) and the conditions for avoiding significant harm to the other objectives (including 3-6). These criteria became applicable per 1 January 2022. The European Commission approved the environmental delegated act for the remaining four environmental objectives in June 2023 (to become applicable per 1 January 2024).

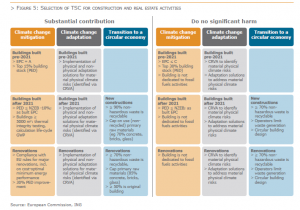

Building loans contributing substantially to climate change mitigation

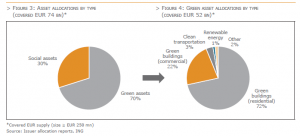

Due to the dominance of mortgage assets in cover pools, the TSC for construction and real estate activities are the most relevant for green covered bonds. Figure 5 confirms that of all the EUR sustainable covered bond green asset allocations, 95% finance energy-efficient building loans.

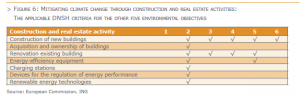

The climate delegated act divides the construction and real estate activities in seven sub-categories. Two of them are low-carbon activities that themselves contribute substantially to one of the taxonomy’s environmental objectives. These are generally most important for the selection of green real estate assets:

One is a transitional activity:

The remaining four activities are all enabling activities. These include the installation, maintenance and repair of:

Figure 5 summarises the TSC for the climate change mitigation, climate change adaptation, and transition to a circular economy objectives. The overview only shows a subset of the criteria for SC and DNSH, solely for the aforementioned low carbon and transitional construction and real estate activities.

To contribute to the climate change mitigation objective, buildings built as of 2021 should have a primary energy demand that is 10% lower than a countries threshold for ‘nearly zero-energy buildings’ applicable for new buildings in the EU per 2021. Buildings built before 31 December 2020 should have an energy performance certificate (EPC) class A. These buildings are also taxonomy compliant if they belong to the top 15% most energy efficient buildings of the regional and national building stock built before 2021.

The 15% best in class criterion for buildings built before 2021 is currently most crucial for the ability of banks to issue green covered bonds that (re)finance taxonomy aligned mortgage loans. After all, the largest share of the building stock is built before 2021. Within this segment the portion of properties labelled with an A class EPC is typically small in most jurisdictions. Besides, these labels often lack comparability between countries. The comparability issue may improve with the planned revisions to the Energy Performance and Buildings Directive (EPBD) as discussed later in this article.

Meeting the TSC for SC is not the only challenge issuers face when ensuring taxonomy alignment. Even if an economic activity contributes substantially to the climate change mitigation objective, it still must avoid doing significant harm to all other environmental objectives. The generic criteria for DNSH to the climate change adaptation objective are crucial, as they apply to all construction and real estate activities. They require a climate risk and vulnerability assessment (CRVA) to identify physical climate risks such as floods, and an adaptation solutions plan to reduce these risks if material.

The importance of taxonomy compliance for green covered bonds

Banks have good reasons to strive for the best possible taxonomy alignment of their green assets. These stretch well beyond the purpose of green bond issuance. The taxonomy regulation is an important pillar to the voluntary EU GBS agreed upon in February 2023, which requires full taxonomy alignment of the use of proceeds.

However, it also forms an integral part of EU regulation promoting sustainable reporting, via the sustainable finance disclosure regulation (SFDR) and the corporate sustainability reporting directive (CSRD). The latter directive becomes applicable in 2024 and replaces the non-financial reporting directive (NFRD) These disclosure regulations have the consequential side-effect that companies (including banks) face increased investor scrutiny on the sustainability of their activities, among others from investors that must show to what extent their investments consider sustainability aspects. The taxonomy compliance of the assets financed via green (covered) bonds is just the tip of the iceberg.

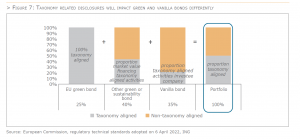

For taxonomy disclosure purposes, the SFDR, NFRD (CSRD) and EU GBS will work as communicating vessels. This is illustrated by an indicative investment portfolio comprised of bonds in figure 7 based on the regulatory technical standards on disclosures under the SFDR. These apply since 1 January 2023 to financial market participants such as insurance companies, pension funds, and investment firms.

The key performance indicator measuring the taxonomy compliance of financial products, is calculated as the ratio of the market value of investments in environmentally sustainable (i.e. taxonomy aligned) activities versus the market value of all investments. Environmentally sustainable investments can (among others) include the following:

For banks, this proportion comes down to the share of environmentally sustainable economic activities as disclosed under the NFRD (CSRD) (i.e., “green asset ratio”).

This illustrates that the taxonomy-related disclosure requirements may impact all bonds, whether marketed with a sustainable use of proceeds or not. The taxonomy compliance of vanilla bonds will also be considered via the issuer’s overall portion of environmentally sustainable activities. Hence, for issuers reporting a stronger taxonomy alignment under the NFRD (CSRD) could translate into more attractive pricing for their vanilla bonds.

The intentions of the ECB to introduce climate change related disclosure requirements for collateral, could strengthen this effect. As of 2026 the ECB will solely accept marketable assets and credit claims from companies and debtors that comply with the CSRD. In light thereof, the ECB and the ESAs also support better and harmonised disclosures of climate related data for assets that do not fall under the CSRD, such as covered bonds and asset-backed securities (see Chapter 1.6).

The European green bond standard

Meanwhile, investors will likely favour those instruments that meet all the criteria of the EU GBS, as these bonds count as 100% taxonomy aligned. Green covered bonds that comply with the EU GBS should therefore allocate the bond proceeds to (new and/or existing) loans (i.e. financial assets) that finance environmentally sustainable economic activities (i.e. taxonomy aligned). These loans do not have to be part of the cover pool.

The proceeds of the financial assets financed through a European green bond should be allocated to fixed assets (eg construction or acquisition of buildings), capital expenditures (eg the installation of renewable energy technologies), or operating expenditures (eg building renovation measures). The loans can also finance other financial assets if there are not more than three subsequent financial assets in a row. The loans financed by green (covered) bond proceeds should in any event not be created later than five years after the issuance of the European green bond.

Issuers may also allocate the proceeds from a portfolio of outstanding European green bonds to a portfolio of taxonomy-aligned assets (portfolio approach). In that case they must prove that the total value of the green assets exceeds the total value of the outstanding green covered bonds. Most banks with green covered bonds outstanding apply a portfolio approach at this stage, but there are also banks that allocate their green bond proceeds to a dedicated loan portfolio.

The European green bond regulation provides some flexibility regarding the full taxonomy alignment requirement. Namely, issuers are allowed to allocate up to 15% of the bond proceeds to economic activities that comply with the EU taxonomy apart from the TSC (flexibility pocket). These include economic activities for which the TSC have not entered into force at the time of issuance. This doesn’t change the fact that issuers still must prove that the activities contribute substantially to at least one of the environmental objectives, DNSH to the other objectives and comply with the MS.

Moreover, capital and operating expenditures funded through a European green bond do not have to be fully taxonomy aligned yet upon issuance if there is a CapEx plan in place. This plan specifies the deadline when the expenditures should be taxonomy-aligned before the bond matures.

European green bond proceeds must always be allocated in full before the bond matures. If the TSC and DNSH provisions are amended ahead of maturity, issuers must ensure that unallocated proceeds and proceeds covered by a CapEx plan, are allocated conform the new criteria within seven years. If the proceeds are allocated via a portfolio approach, the green assets should be aligned with any of the TSC applicable during the seven years prior to the publication of the allocation report. As such, assets not meeting the amended TSC can remain part of the green portfolio for seven years at most.

The EU GBS also subjects issuers of European green bonds to stricter transparency requirements. The required (pre-issuance) green bond factsheet and (post-issuance) allocation and impact reports, will only provide information on the level of the green asset portfolio. For covered bonds there are no information provisions on the taxonomy alignment at the level of the cover pool. However, the climate change disclosure improvements deliberated by the ECB and ESAs for securitisations could also become relevant to covered bonds. The EU GBS already sets specific disclosure and exclusion requirements for EU GBS securitisation notes. These include information on the taxonomy eligibility and alignment, and compliance with the DNSH criteria of the underlying assets.

The EU GBS may become the preferred reference for investors to show the taxonomy alignment of their green bonds. Especially as investors may not always have resources to perform a taxonomy compliance assessment for every green bond. Against this backdrop, industry initiatives, such as the EMF-ECBC’s Energy Efficient Mortgages Initiative (EEMI) and the VDP’s minimum standards for Green Pfandbriefe, will remain an important support to both issuers and investors in their green bond structuring and investment processes.

EPBD revisions will enhance the energy efficiency of buildings

When it comes to the future evolution of the environmental metrics of covered bond collateral pools, it is also important to bear in mind that the EPBD is aiming for a zero-emission building stock by 2050. The measures included in the legislative proposal 2021 are considered pro portionate and build on the existing design of the original 2002 Directive and the 2010 and 2018 revisions. As indicated in the Climate Action Plan, the EPBD is the key legislative instrument to deliver on the 2030 and 2050 decarbonization objectives. It follows up on key components of the three focus areas of the Renovation Wave Strategy, including the intention to propose mandatory minimum energy performance standards, following an impact assessment looking at their scope, timeline, phasing in and accompanying support policies.

In the EU, heating, cooling and domestic hot water account for 80% of the energy that households consume. In order to make Europe more resilient there is a need for energy efficiency renovation for buildings and making them less dependent on fossil fuels. Energy efficient buildings are key for reducing the energy consumption, bringing down emissions and reducing energy bills since buildings account for 40% of energy consumed and 36% of energy-related direct and indirect greenhouse gas emissions.

The EPBD trilogues have begun and will continue after the summer, so expected outcomes are very far from certain when writing this. At this point there is only the knowledge of the following positions.

European Parliament:

Building energy performance: All new buildings should be zero-emission from 2028, while new buildings occupied, operated or owned by public authorities from 2026 (the Commission has proposed 2030 and 2027 respectively). All new buildings should be equipped with solar technologies by 2028, where technically suitable and economically feasible, while residential buildings undergoing major renovation have until 2032 to comply.

Residential buildings would have to achieve at least EPC E by 2030, and D by 2033. Non-residential and public buildings would have to achieve the same classes by 2027 and 2030 respectively (Commission has proposed F and E). All measures needed to achieve these targets would be established by each member state in national renovation plans. To take into account EU countries’ diverse building stocks, G should correspond to the 15% worst-performing buildings in the national stock.

MEPs also want to allow member states to adjust the new targets in a limited share of buildings covered by the requirements depending on the economic and technical feasibility of the renovations and the availability of skilled workforce.

Mortgage portfolio standards: Are defined in Art. 2(36) as mechanisms “requiring any mortgage lenders to establish a path to increase the median energy performance of the portfolio of buildings covered by their mortgages towards 2030 and 2050”. Art. 15 requires the European Commission to adopt a delegated act “to ensure that mortgage portfolio standards effectively encourage financial institutions to increase volumes provided for renovations, to prescribe supportive measures for financial institutions and necessary safeguards against potential counter-productive lending behaviors”.

Access to data: Article 19(2) foresees “easy and free of charge access to the full energy performance certificate for financial institutions as regards the buildings exposure to residential or commercial property which have been assigned to their non-trading book”.

Energy Performance Certificates: MEPs propose that EPCs “shall include a dedicated section on financing, listing available financing options and grouping indicators most relevant to financial institutions, mortgage providers, national promotional banks and other relevant institutions providing access to funding”.

Council:

Remains very close to the original EC proposal, but with some modifications:

Differentiation in the approaches between non-residential buildings (threshold approach) and residential buildings (trajectory approach) in Art. 9 on Minimum Energy Performance Standards;

Harmonisation of Energy Performance Classes and introduction of a new category (i.e. A0 and A+) to the EPCs in Art. 16;

The ECBC is paying close attention to the negotiations and in the spring submitted a position paper, alongside the EBF and AFME, to the co-legislators, highlighting the industry’s concerns including requirements for mortgage lenders for their portfolios, Mortgage Portfolio Standards, the template for EPCs and pay as you save scheme-requirements for lenders.

Green covered bonds as an instrument to finance green investments by the local public sector

While the (re)financing of energy efficient housing loans is the most important use of proceeds, green covered bonds are also issued to finance other environmental activities.

Local and regional governments in most European countries are, for instance, in charge of investments related to waste management, water treatment and public transportation. These investments often have important environmental benefits, in particular by reducing pollution and CO2 emissions. Together, these activities represent an important share of local and regional government investments. In 2021, European Union local and regional government investments totaled EUR 258 bn[1]. Waste water treatment represented investments by local and regional governments for a total amount above EUR 8 bn, and more than EUR 4 bn was invested by local authorities in the area of waste management. Investments by local and regional governments linked to transportation, including clean public transportation, exceeded EUR 47 bn in 2021.

Public sector covered bonds finance an important share of these investments in large parts of Europe, including France and Germany. A significant share of these loans finances investments in clean transportation, sustainable water management and waste management.

Green public sector covered bonds are a relatively new instrument. The first benchmark green public sector bond was issued in 2019, to finance green investments by local authorities in France. One problem holding back public sector covered bond issuers from issuing under green covered bonds is the difficulty of identifying green projects. Local government lenders typically finance the overall investment budget of a local authority, and do not link the loan contract to specific investment projects. In some cases, local government lenders may finance public sector entities with a clearly defined mission, for example public water boards or public transport authorities. However, in most cases local government lenders will need to adjust the lending process by setting up loan contracts linked to specific green investments, in order to refinance these assets via the issuance of green public sector covered bonds.

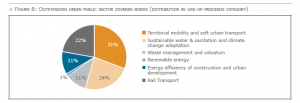

The total outstanding volume of benchmark green public sector covered currently stands at EUR 2.25 bn with two active benchmark issuers. The majority of proceeds has been used to finance investments in clean transportation:

It is worth noting that local authority investments often have both environmental and social objectives. As an example, the construction of a new school will be an investment in public education, but at the same time, it may also be considered a green project, if the construction is an energy efficient building. Another example would be the construction of a new tramway line with a focus on providing clean local public transportation, but at the same time providing important social benefits. Sustainable water management is another area, where social and environmental objectives are closely linked. Very often, it will be up to the issuer to determine whether a specific local government investment mainly aims to address social or environmental issues.

Taxonomy considerations

Many issuers will aim to align their green covered bond issuance with the applicable taxonomy regulation.

The relevant delegated act also defines the criteria for some areas of investment that may be financed by green public sector covered bonds. In particular, it defines the criteria for ‘urban and suburban transport and road passenger transport’ which is relevant for investments in tramways and subway systems, a key area of investment for local and regional governments. Investments will generally comply with the TSC of zero tailpipe emissions defined by the taxonomy. The delegated act also provides criteria for other investments in clean public transportation, for example electric busses.

Energy efficient public buildings are another area of investments refinanced via the issuance of green public sector covered bond. These are subject to the same criteria as set out for green mortgage covered bonds.

The two other key areas of investment financed via green public sector covered bonds are waste management and sustainable water management. The delegated act on sustainable activities for climate change adaptation and mitigation provides some criteria that may be applied to these activities, with a focus on CO2 emissions. However, in many cases the criteria to be set out in the future delegated act on the sustainable use and protection of water and marine resources, to the transition to a circular economy, to pollution prevention and control, or to the protection and restoration of biodiversity and ecosystems will be more relevant for these activities.

Outlook

One additional issuer has come to the market with a green public sector covered bond with a focus on financing rail infrastructure. However, the overall use of the green bond format for public sector covered bond issuance remains very limited.

One potential area of growth may be linked to the financing of export contracts with public guarantees. Export loans benefitting from Export Credit Agency guarantees are regularly financed via the issuance of public sector covered bonds. In many cases, these loans finance green investments, for example in the area of renewable energies or rail transport. To date, one framework has been set up to finance this type of loan via the issuance of green public sector covered bonds.

Green covered bond market

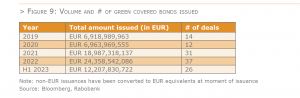

After two years of relatively stable supply, the volume of green covered bonds exploded in 2021, when over EUR 17.4 bn was printed. 2022 was an absolutely record-breaking year for green covered bonds with an equivalent amount of over EUR 24.0 bn. H1 2023 is on track with over EUR 12.2 bn already absorbed by the market, see below figure 9.

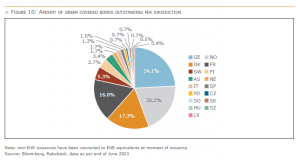

2022 saw three jurisdictional debut transactions: the first green covered bond from the Netherlands, an inaugural fully green issue from Spain and a debut deal out of Slovakia. In June 2023 an inaugural deal from the Czech Republic was added to this list. Measured as per 1H 2023 figures, we have now seen green covered bonds issued out of 17 different jurisdictions by 63 single issuers. German, Norwegian, Danish and French issuers represent the largest group with 78.4% of the current outstanding volume.

What is driving this recent acceleration of the green covered bond market? A key difference between conventional covered bonds and green covered bonds can be found in the investor audience and reception.

Primary markets perspective:

Printing a covered bond in green format involves additional costs (ie additional ESG reporting, drafting and maintaining a GBF, costs of SPO(s)). Hence one could assume that issuers are only willing to make these investments if printing a green bond compensates for these costs.

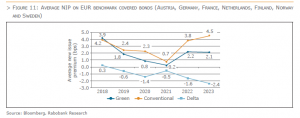

Figure 11 confirms that, since 2019, green covered bonds have benefited from a lower average new issue premium (NIP) than conventional covered bonds in the primary market. This delta increased over the years with one exception: 2021, when the delta between the two metrics decreased to 0.5bp. In 2022 the average difference in NIP increased again to 1.6bp, followed by a further increase to 2.4bp for the first five months of 2023. Based on these figures, one could conclude that the demand for green covered bonds is higher than for conventional covered bonds, resulting in lower NIPs for the first, which consequently results in a funding cost advantage.

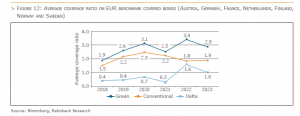

Another way of looking at this, is by focusing on the average coverage ratio. Studying this data it follows that green covered bonds have been able to accumulate larger order books than conventional covered bonds over the period 2018 to 2023 (end of May). Whereas the delta between both groups remains equal in the first two years, it further grows in 2020. After a decline of the delta in 2021, the delta grows to 1.6 in 2022. For the year to date (until end of May 2023) months in which the ECB gradually decreased its order, we see that the average coverage ratio for both types of covered bonds decreased. Nevertheless, the coverage ratio for green covered bonds only dropped from 3.4 to 2.9 times (a decrease of 14.7 %), whereas the same metric for conventional covered bonds decreased from 1.6 to 1.0 times (a decline of 37.5 %).

Based on the above two perspectives, green covered bonds outperform conventional covered bonds in terms of coverage ratio, and (most likely) as a result of that by paying a lower NIP. These benefits help to explain the popularity of green covered bonds from an issuer perspective. Printing a covered bond in green format would coincide with lower execution uncertainty than printing a conventional issuance.

Secondary Markets perspective:

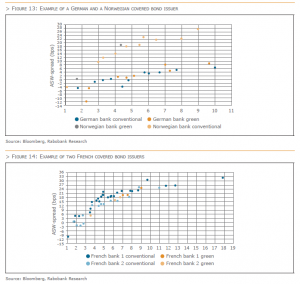

A different perspective can be generated by studying secondary market data whereby we compare outstanding bonds. In doing so, we compare the average spread levels (ASW based) on a single moment in time (i.e. 23 May 2023) for issuers that have both green covered bonds and conventional covered bonds outstanding. In order to isolate spread differentials between countries, we created three different selections: (i) a German issuer, (ii) two French issuers and (iii) one Norwegian issuer. Studying these market snapshots to see how pricing occurs in secondary markets does not offer a clear picture. Taking the most active German issuer as an example in Figure 13, we observe that on the short end of its curve, its green covered bonds are tighter than the levels for its conventional bonds. This difference, subject to tenor, seems to indicate a greenium of 2bp to 8-9 bp. Please note that on 23 May 2023 one of the outstanding green covered bonds was a relative outlier on the curve, thereby most likely inflating the greenium. When focusing on the middle part of the curve for this specific issuer, we observe no greenium, whereas on the longer end of the curve two of the green covered bonds priced wider at that moment in time. This difference can be explained however by the fact that these two bonds were printed in 2023 and required a NIP at the time of printing which has not been fully converged at the moment of recording the data. When performing a similar analysis on the curve of a Norwegian bank, which is the most active in EUR benchmark format, we see no indication of a greenium.

In figure 14, the green covered bonds from two French issuers are compared with their conventional covered bonds. In this case, we observe no greenium for French bank 2. Both its conventional and green covered bonds seem to price in the same range. However, for French bank 1 a greenium of 2-3 bp is visible in the 7 to 8 years part of the curve.

We therefore conclude that the existence of a greenium is issuer-driven and subject to issuer-specific characteristics. For those issuers that are already very active in the green covered bond space, we expect the greenium to be negligible. For those issuers with limited green covered bonds outstanding (and also country specific) we consider the greenium to range between 1-3bp. Furthermore, tenor and timing of issuance seems to play a role. Finally, this form of analysis is also subject to timing as different bonds are compared on a single moment of time. As a result, we cannot determine a market-wide greenium for green covered bonds on 23 May 2023. For some issuers, this could be explained by already tight spread levels and hence limited room for further tightening as well as reduced liquidity in the market.

Conclusion

Although the market share of green covered bonds is relatively modest compared to the overall green bond market, the direction of travel is clear. Since 2021 green covered bonds have experienced an impressive growth path. This growth is supported by political and regulatory developments in Europe, aiming at channeling investments towards environmentally sustainable assets. Currently, all green covered bonds are ICMA GBP based. However, the taxonomy regulation, and related voluntary EU GBS will form an important future reference point for investors when assessing the contribution of green covered bonds towards environmentally sustainable objectives. The execution in green covered format has tangible benefits for issuers in the form of higher coverage ratios and lower NIPs compared to conventional bonds. However, in the secondary market the existence of a greenium is to a large extent issuer specific. For those issuers that are already very active in the green covered bond space, we expect the greenium to remain more negligible than for issuers with fewer green covered bonds outstanding.

By Maureen Schuller, ING & Sjors Hoppenbrouwers, Rabobank & Ralf Berninger, CAFFIL & Sanna Eriksson, OP Mortgage Bank

The European Covered Bond Council (ECBC) is the platform that brings together covered bond market participants including covered bond issuers, analysts, investment bankers, rating agencies and a wide range of interested stakeholders.