14 November 2016

By Bernd Volk, Director, Deutsche Bank

By Bernd Volk, Director, Deutsche Bank

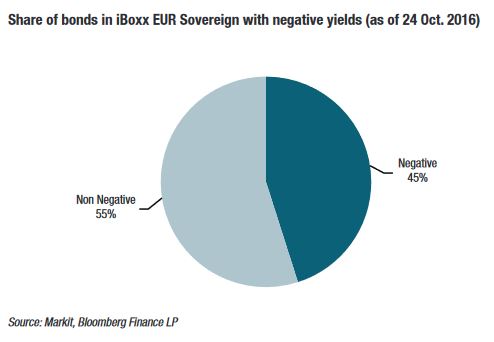

Given the current environment, fixed income assets are undoubtedly expensive. As of the 24th of October 2016, the share of negative yielding bonds in the iBoxx EUR Covered index was 74%. This compares to 45% in the case of the iBoxx EUR Sovereign index. Peripheral countries account for 23.7% in the iBoxx EUR Covered (Spain 15.5%, Italy 6.5%, Ireland 1%, Portugal 0.6%) compared to 38.6% in the iBoxx EUR Sovereign (Italy 23.9%, Spain 12.8%, Ireland 2%).

Even though a part of the difference in the share of negative yielding bonds between the iBoxx EUR Covered and the iBoxx EUR Sovereign can be explained by the country distribution (and also by differences in duration), most euro area covered bonds trade tight versus underlying sovereign bonds. Moreover, on top of historically low absolute yields, also versus swaps, covered bonds trade close to historically tight levels. However, with no covered bond investor having suffered a loss in recent history, in contrast to sovereign bonds, relative value remains an open discussion, particularly in the case of covered bond markets that are relatively small and therefore easier to exempt from losses.

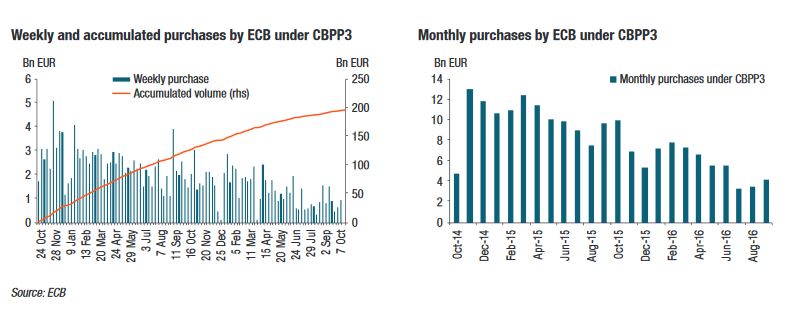

Generally, settlements under the European Central Bank’s (ECB) covered bond purchase programme (CBPP3) were significantly lower after the summer break compared to settlements before the summer break. In recent weeks, the CBPP3 purchase rate was at the lowest since the programme started. Mainly driven by low issuance of EUR benchmark covered bonds by euro area banks, average weekly purchases under CBPP3 have amounted to EUR 1bn since July compared to EUR 1.7bn in the first half of the year.

Hence, there is some kind of covered bond tapering, which might be due to lack of available bonds or due to relative value considerations by the ECB. The volume of covered bonds purchased by the ECB under CBPP3 as a percentage of volume purchased under PSPP was only 6% in September 2016, the second lowest monthly level since the start of PSPP in March 2015 (after 4.7% in July 2016), comparing to a high of 26.2% in March 2015, 24% in April 2015, and 19.4% in May 2015.

In total, the ECB held EUR 196.5bn of covered bonds under CBPP3 as of the 21st of October 2016. Together with CBPP1/2, the ECB held EUR 218bn of covered bonds. As this compares to EUR 550bn of covered bonds issued by euro area banks in the iBoxx EUR Covered, the ECB holds 40% of the thereby defined public market. However, the total volume of euro denominated covered bonds “issued” by euro area banks registered in the ECB collateral database, including retained covered bonds and private placements, amounts to EUR 1050bn. Consequently, in this respect, the ECB holdings under CBPP1-3 account for only 21%.

The ECB press conference on the 20th of October 2016 did not provide new insights regarding quantitative easing (QE) extension or tapering. Technical changes to enable the ECB to continue sourcing the significant monthly QE volume it targets could be announced at the December 2016 meeting. However, ECB Governing Council member Ewald Nowotny is quoted as saying on the 24th of October (at a speech on wider policy issues at the Vienna University of Economics & Business regarding covered bonds): “That is an individual area where we have reached limits. In the meantime, we have enough other investment options.”

The question remains if the ECB will formally end CBPP3 before the ending of ECB QE or during tapering of ECB QE. On the one hand, CBPP3 started four months’ earlier than PSPP. Moreover, the ECB may want to save itself from what happened with CBPP2, which was closed due to lack of available bonds. On the other hand, as long as ECB QE is running and the ECB does not see CPI inflation moving closer to its target level of “close but below 2%”, the ECB may want to keep its flexibility regarding asset purchases. In this respect, exiting CBPP3 earlier than ECB QE would take away a comfortable purchase channel, i.e. purchasing covered bonds in the primary market for euro benchmark covered bonds. Moreover, at the introduction of CBPP3, the ECB highlighted that the programme is “very different” to CBPP 1 and CBPP2. Hence, any comparison between CBPP3 and CBPP1/2 seems challenging.

In December 2015, the ECB announced the reinvestment of maturing bonds. Given the wording (“reinvest the principal payments on the securities purchased under the APP as they mature, for as long as necessary”), the announcement seems to refer only to CBPP3 and not to the ECB holdings under CBPP1 and CBPP2 (amounting to EUR 14.281bn and EUR 7.115bn respectively as of the 21st of October). Given that the ECB holds EUR 196.5bn of covered bonds under CBPP3 as of the 21stof October, reinvestments are likely to amount to over EUR 10bn in 2017 and over EUR 15bn from 2018 to 2022.

With only EUR 15bn of new EUR benchmark covered bonds, primary market activity regarding euro benchmark covered bonds in Q3 2016 was at the lowest Q3 level in euro area history, followed by EUR 15.2bn in Q3 2012, EUR 17.2bn in Q3 2002 and EUR 17.5bn Q3 2008.

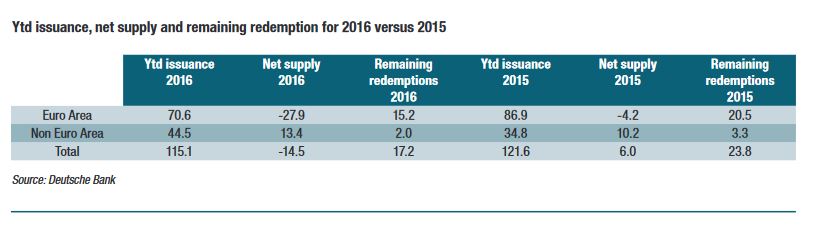

As of the 24th of October, euro benchmark covered bond issuance amounted to EUR 7.2bn compared to EUR 16.7bn in October 2015. Total year-to-date (ytd) issuance of euro benchmark covered bonds amounted to EUR 115.1bn compared to EUR 122bn in 2015 ytd. Net supply amounted to minus EUR 14.5bn ytd compared to positive net supply of EUR 6bn in 2015 ytd. Overall, the high negative net supply supported tight spreads of covered bonds.

With a share of 18%, German issuers rank highest regarding ytd issuance of euro benchmark covered bonds, followed by French issuers (17%), Canadian (11%) and Spanish issuers (9%). While non-euro area banks provided a remarkable share of 38.2%, with 61.8%, euro area banks still dominated.

Euro benchmark covered bond redemptions until year-end amount to EUR 15.3bn, with EUR 13.3bn being from euro area banks. There seems also no indication for a massive increase of supply until year-end. In 2017, euro benchmark covered bond redemptions will be by EUR 30bn lower than in 2016 (EUR 147bn), amounting to EUR 116.5bn.With EUR 26.1bn, Spanish issuers again face the highest redemptions in 2017, even though declining significantly from the EUR 38.5bn in 2016. French and German issuers follow with EUR 23.5bn and 15.4bn respectively. Overall, given the lower redemptions in 2017 and assuming primary market activity in 2017 would be similar to 2016, 2017 could become a year of positive net supply.

Besides ECB purchases under CBPP3 and new issuance volumes, also covered bond structures remain in focus. Given the increasing issuance and also numerous conversions due to consent solicitations in recent years, the share of extendible covered bonds in the iBoxx EUR Covered Index is at is at 42% already comparable to 27% in 2013.

Soft-bullet structures are already well established in the covered bond market. However, until a few years ago, public issuance of conditional pass-through (CPT) covered bonds was hardly accepted by investors. In the meantime, the issuance of CPT covered bonds has become more and more usual. Supported by the ultra-low yields and structural enhancements in prospectuses, most investors have accepted investing in CPT covered bonds. In contrast to soft-bullet covered bonds, a sale of cover pool assets during extension is an option and not an obligation in case of CPT covered bonds.

Even though some details of CPT covered bonds are similar to asset backed securities, a main strength is that CPT covered bonds can typically only be extended in case of issuer insolvency. Moreover, issuer insolvency is typically only a necessary but not a sufficient condition for pass-through (PT).

In the case of resolution of the bank issuing CPT covered bonds, the main risk seems to be that the covered bonds end up in the winding-down entity. The switch to PT can apply to one or all series of outstanding CPT covered bonds depending on

the trigger breached. CPT covered bonds typically become PT sequentially if the issuers and the cover pool fail to pay principal at the scheduled bond maturity whereas a breach of contractual tests (amortisation/asset coverage test) triggers the switch of all outstanding series. It seems noteworthy that the PT in the case of CPT covered bonds only refers to the principal but not the interest. Covered bonds continue to pay interest during extension.

With an inaugural euro benchmark covered bond out of Poland issued in October 2016, the first legal framework based CPT covered bond had a successful market appearance. In the case of Polish CPT covered bonds, non-payment of the covered bonds at scheduled maturity leads to a mandatory legal framework based on 12 months’ maturity extension. A breach of the liquidity test or the coverage balance test during extension would trigger the PT for all outstanding series.

Overall, the share of extendible covered bonds in the euro benchmark covered bond market is likely to increase further. While soft-bullet structures will continue to dominate the extendible covered bonds, also CPT covered bonds are likely to become more important.

This article was originally published in the October 2016 edition of the EMF-ECBC Market Insights & Updates newsletter. Please note that any views or opinions expressed in this article are those of the authors and not necessarily those of the EMF-ECBC. This article does not constitute investment advice.

The European Covered Bond Council (ECBC) is the platform that brings together covered bond market participants including covered bond issuers, analysts, investment bankers, rating agencies and a wide range of interested stakeholders.