24 August 2018

Harmonisation of covered bond frameworks has been topping the agenda of authorities and the covered bond community in recent years. In 2018, the journey towards harmonisation reached a new milestone with the European Commission’s (EC) final proposal for a new Covered Bond Directive as well as an update to the regulation regarding covered bonds (i.e. amending Article 129 of the CRR). In this article, we discuss the main details of the EC’s proposals. The following chapter will discuss European Secured Notes, which are likely to be created as new separate funding instrument as well.

In recent years, an increasing number of reports, and proposals, have been published on harmonising EU covered bond frameworks. It started in July 2014 when the European Banking Authority (EBA) published its view on the preferential risk weight treatment of covered bonds. The EBA concluded that the preferential risk weight treatment of covered bonds was warranted, but it also noted that more convergence was needed. This in order to increase the safety and robustness of the covered bond instrument which would enhance financial stability as well as safeguard the preferential risk weight treatment. Overall, the EBA identified various areas where convergence of legal frameworks was recommended in the medium to longer term. The key areas were:

The EC took the discussion on covered bond harmonisation to another level in 2015, when it published a consultation paper on covered bonds in the European Union (EU), which was part of the EC’s action plan to build a Capital Markets Union. In September 2016, the EC decided to request a study on the costs and benefits of introducing a legislative EU framework on covered bonds. This report ‘Covered Bonds in the European Union: Harmonisation of legal frameworks and market behaviours’ was published in May 2017. In the meantime, however, the EBA published a follow-up report in December 2016, which included its recommendations on harmonising covered bond frameworks in the EU.

In this report, the EBA proposed a three-step approach towards harmonisation of covered bonds, taking into account that EU covered bond frameworks differ in particular in regard to legal, regulatory, and supervisory issues, while acknowledging that the final framework should build on the strengths of existing frameworks. This would still leave room for varying national implementation. This was in line with the industry’s preference that any convergence of national frameworks should be principle based.

Overall, the EBA proposes a three-step approach to harmonisation:

The final proposals of the EC have taken into account all the above-mentioned reports, putting most weight on the recommendations of the EBA. Furthermore, it also took into account a report of the EU Parliament outlining its position on the harmonisation of covered bond frameworks. In fact, the EU Parliament supported the EBA proposals as well.

The EC proposal consists of a new Directive and Regulation. The Directive will replace the current UCITs definition of covered bonds (in line with the EBA proposal), becoming the new single reference point for regulation related to covered bonds. The Directive will provide a common definition of covered bonds, while defining all core features of covered bonds, as well as defining the tasks and responsibilities of supervisors. Overall, it regulates the covered bond product with a focus on protecting investors. Having said that, the Directive has remained of high-level and principle based, on the one hand strengthening the definition of covered bonds, while on the other hand preventing to harm the existing well-functioning market.

The main elements of the Directive include:

The articles of the Directive start off by defining the dual recourse principle and bankruptcy remoteness of covered bond, also noting that covered bonds can only be issued by EU credit institutions. The Directive continues by subscribing what type of assets can be allowed in cover pools. It notes that only high-quality assets can be used as collateral for covered bonds, referring to points (a) to (g) of CRR Article 129 (1). This includes public sector loans, residential mortgages, commercial mortgages, and ship loans. However, the Directive leaves room for other high-quality assets as long as their market value can be derived, while they should also be enforceable in one way or the other. This raised some questions from the covered bond industry, and the EC has indicated that it will take this feedback on board.

Having said that, there should be sufficient homogeneity of the cover assets regarding for instance their lifetime and risk profile. The EC has already indicated that SME loans as well as infrastructure loans are unlikely to meet the requirements, but it is currently assessing the merits of a new instrument called European Secured Notes (ESN), see chapter 1.10.

Furthermore, the Directive includes articles addressing assets located outside the EU, intra-group structures and joint funding, derivative contracts, segregation of assets, and investor information.

The Directive continues with proposals about requirements for coverage and liquidity. It states that the ‘total nominal amount of all assets in the cover pool are at least of the same value as the total nominal amount of the outstanding covered bonds’. This is the so-called ‘nominal principle’. In this context, the Regulation stipulates that a 5% minimum level of OC is required, also based on a nominal calculation. The minimum level of overcollateralisation (OC) is one of the new highlights of the Regulation, which is in line with the EBA proposals.

Furthermore, national authorities are allowed to reduce this level to a minimum of 2% under certain conditions (i.e. the calculation of OC is either based on a model which takes into account the assigned risk weights of the assets or a model where the valuation of the assets is subject to mortgage lending value). The latter seems to be aligned with the German/Austrian situation.

Regarding liquidity, investors will be protected by the requirement for issuers to keep liquid assets to cover the net liquidity outflow for 180 calendar days. This is also in line with the EBA proposals. What is more, the final maturity date might be used for the calculation of the principal payment of covered bonds with extendable maturity structures.

In the previous few years, many banks have changed the structure of hard bullet covered bonds to soft bullet structures, with most allowing the possibility to extend the maturity by maximum 12 months. Meanwhile, conditional pass-through covered bonds, which have a much longer theoretical maturity extension, have seen the light of day (see more in chapter 1.5). The treatment of such extendable structures has been a big topic of debate, with the main focus being on whether the maturity extension can be at the full discretion of the issuer. The EC has now decided that the maturity extension should be based on specific triggers, which are outside the discretion of the issuer.

The new Directive includes many pages about the public supervision of covered bonds. Of course, covered bonds are and need to be subject to public supervision. Furthermore, it should be ensured that supervisors have all the capabilities and means to carry out their role in a proper way. Unsurprisingly, issuers need to register their covered bond programme before getting approval issuing covered bonds. Meanwhile, the articles on public supervision address issues such as reporting requirements, the powers that supervisors have in case of noncompliance of issuers, and the role of the supervisor when an issuer is insolvent or in resolution. The broad coverage of the public supervision stands in stark contrast with the current requirement that in a general way describes that covered bonds need to be supervised. This strengthens the quality of covered bonds, although member states’ supervising authorities still seem to have some room for manoeuvre.

In 2012, the European Mortgage Federation and European Covered Bond Council introduced the EU Covered Bond Label. This label established a clear perimeter for the asset class and has resulted in the introduction of the Harmonised Transparency Template (HTT), which has improved transparency (and reporting standards). The new Directive acknowledges the merits of the label, noting that credit institutions are allowed to use the label ‘European Covered Bonds’ in the Directive. The label should make it easier for investors to assess the quality of covered bonds. The use is facultative though and can also be used alongside national labels.

The EC’s aim is to get a smooth transition towards the new Directive, which should prevent any unwanted market distortions. Therefore, it proposes generous grandfathering provisions. Actually, all existing covered bonds that currently comply with the UCITS Directive and the CRR will be grandfathered, while covered bonds issued before 2007 will also be grandfathered, keeping all existing regulatory benefits. As such, current outstanding covered bonds will not be treated differently, which should indeed result in a smooth transition. Furthermore, there will be a 12-month implementation phase, during which Member States need to adopt the Directive in their national legislation.

Meanwhile, after three years of the implementation the EC will review developments regarding the new Directive, while it will also assess whether an equivalent regime could be introduced for third-country credit institutions issuing covered bonds.

The package also includes proposals to amend article 129 of the CRR. The changes will be two-fold. On the one hand, some parts of the CRR Article 129 will be deleted. This is for instance true for the reporting requirements, which will be shifted towards the Directive. Furthermore, it will no longer be allowed to use as cover assets RMBS/CMBS or senior units issued by French Fonds Communs de Titrisation securitising residential or commercial property exposures. This is in line with the EBA recommendations.

Regarding the inclusion of substitution assets in the cover pool, it will be allowed to use substitution assets qualifying as credit quality step 2 for a maximum of 10% of outstanding covered bonds. Before, only assets with credit quality step 1 were allowed (up to 15%). The latter remains, but increased difficulty to comply with the former stricter rule has resulted in this amendment.

Meanwhile, the minimum required level of OC has also been specified in the CRR (see above). Furthermore, the proposed amendments address the issue of LTV limits. Overall, the authorities stick to the 80% LTV limit for residential mortgages and 60% for commercial mortgages. However, the CRR is more explicit in saying that these are soft limits, implying that a loan in the pool can only act as collateral within the LTV limits.

The next step is that the EC will discuss the text with the EU Parliament as well as the EU Council. They need to agree on a common text. Overall, it is expected that this should be a smooth process, as the EU Parliament’s ideas outlined in its own initiative are roughly in line with the EC’s proposals. The aim is that the current EU Parliament will be able to approve the proposals implying that agreement need to be reached before the end of 2018. The EU Parliament can then adopt the Directive in Q1 2019.

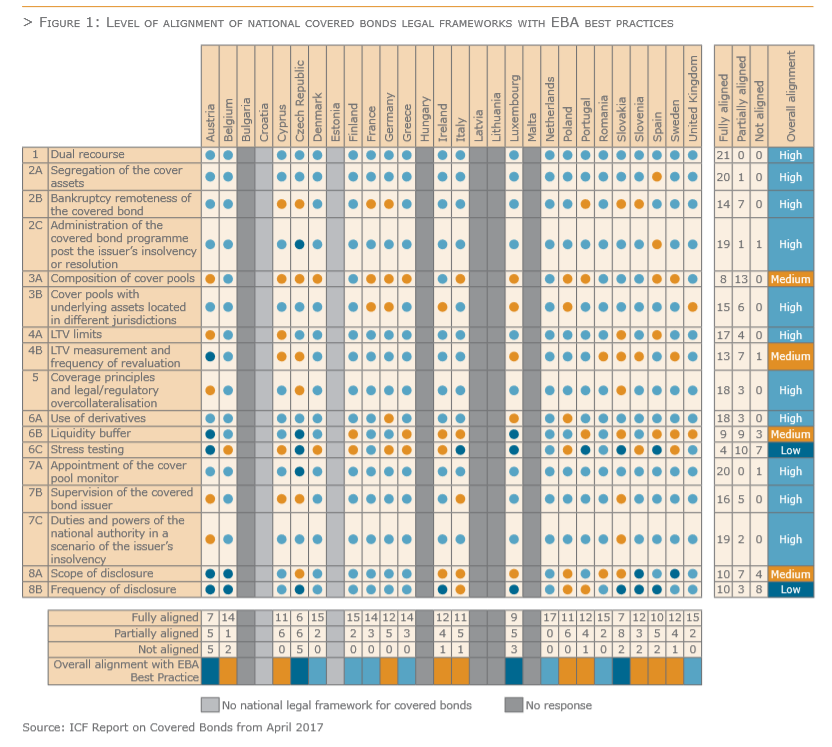

It is likely that most countries need to make some adjustments to their covered bond framework to fully align them with the new requirements. However, already a few countries put the update to their national frameworks on hold waiting for the details of the EC proposals (among others: France and Spain). Overall, no major issues are expected regarding the implementation of the new Directive in different countries. The chart below shows an overview of the EBA in 2016, which shows the degree of alignment of various countries with the best practices on covered bonds (which were used as a blueprint by the EC).

In our view, the new Directive strikes a good balance between strengthening the covered bond product, while also keeping room for national differences. Indeed, we welcome the principle-based approach of the EC. When in place, the Directive is likely to support the covered bond market, offering even more protection to investors. The Directive will probably also result in more issuance of covered bonds, as it will induce more jurisdictions to setup covered bond frameworks, while there will most likely also be new covered bond issuers in existing covered bond jurisdictions. Finally, the Directive can act as a blueprint for countries outside the EU when setting up covered bond frameworks.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.