20 November 2019

By Colin Chen, DBS & Chairman of the ECBC Global Issues Working Group and Maureen Schuller, ING Bank

This article is a summary update of the ECBC Global Issues Working Group Brochure, which was established with special thanks to Elena Bortolotti, Barclays, Thomas Cohrs, NordLB, Sascha Kullig, vdp, Filipe Pontual, ABECIP, Franz Rudolf, UniCredit, Lily Shum, CMHC and Christopher Walsch, Clifford Chance for their support and valuable contributions.

A QUICK GLANCE AT THE GLOBAL PICTURE

For over 200 years, covered bonds have proven to be an efficient debt instrument enabling banks to mobilise private sector means and capital towards long-term investment with a wide public benefit and, in particular, real estate loans and public sector debt. During the years of market turmoil, covered bonds demonstrated a strong degree of resilience. Throughout the crisis, they played a pivotal role in bank wholesale funding, providing lenders with a cost-effective and reliable long-term funding instrument for mortgage and public-sector loans. The Industry continues to build on the lessons learnt from the financial crisis while maintaining a focus on the essential features and qualities that have made the asset class such a success story.

The ongoing EU Capital Markets Union (CMU) and Basel IV discussions are now, more than ever, opening new frontiers for covered bonds at both EU and international levels. The covered bond financing instrument is being exposed to critical evolutions which can bring about both new opportunities but also new risks. The covered bond market is faced with new regulatory, policy and supervisory developments, while market innovation, the continuous process of globalisation and national implementation of the covered bond concept will also leave their mark on the asset class.

In view of these considerations, the covered bond industry believes that there is a clear need to preserve the key nature of the product as a crisis management tool rooted in robust qualitative and macroprudential characteristics which are the basis for ensuring a regulatory recognition at global level.

POLICY DEVELOPMENTS

Looking back over the past months, it is clear that the covered bond space has been fundamentally impacted by major waves of monetary policy, supervisory review and regulatory change which is having a significant impact on the long term financing and housing finance sectors.

This evolution is further evidenced in April 2019, when following the trilogue negotiations with the Council and the European Commission on the proposal for a Covered Bond Legislative Package, the European Parliament’s Plenary adopted the full text as approved by the Council and the European Parliament’s Economic and Monetary Affairs Committee earlier in the year.

The Legislative Package provides for the first time in the history of covered bonds, an enhanced harmonisation of the European Covered Bond market, in line with the objectives of the Capital Markets Union and reinforcing a European common qualitative benchmark for international investors and respecting well-functioning traditional markets. As importantly, it paves the way for the smooth introduction of the covered bond asset class in newer and emerging covered bond markets in the European Union, whilst also serving as an important legislative benchmark on a global level for countries such as Australia, Canada, New Zealand, Singapore, South Korea and Japan.

MARKET DEVELOPMENTS

Covered bonds are at the heart of the European financial tradition, having played a central role in funding strategies for the last two centuries. The strategic importance of covered bonds as a long-term funding tool is now recognised at a global level.

Outside Europe, Australia, Canada, New Zealand, Singapore and South Korea have already implemented covered bond legislation in recent years. Major jurisdictions including Brazil, Chile, India, Japan, Mexico, Morocco, Panama, Peru, South Africa and the United States, are either in the process of adopting covered bond legislation or are investigating the introduction of covered bonds.

LOOKING AHEAD

The Industry has demonstrated that through market initiatives such as the Covered Bond Label and the transparency and disclosures under the Harmonised Transparency Template (HTT), it is possible to build, from the bottom-up, proposals based on market consensus in order to initiate pan-European solutions which enhance transparency, comparability, convergence of markets and best practices.

Taking stock of where we have come from, where we are now and where we are heading, it is clear that the market and the environment in which it operates is constantly evolving and as such the work of the ECBC and its Global Issues Working Group is always in progress. The Industry will continue to lean towards the creation of a common regulatory framework for covered bonds that will enable the market to grow and flourish to the benefit of all its participants on a global level.

The role of the ECBC Global issues Working Group

In order to develop synergies between traditional, new and emerging covered bond markets as the joining of forces should allow the development of a more levelled playing field for all at a global level, the

European Covered Bond Council (ECBC) established its ECBC Global Issues Working Group (GIWG) in 2015. So far, the work undertaken by the GIWG has been instrumental in ensuring a proper recognition of the macro-prudential value of the covered bond asset class while securing an appropriate, homogenous and cross-border regulatory treatment by different jurisdictions at a global level.

To this end, ECBC members have identified an important role to be played by the Working Group as a discussion forum for exchanging market best practices and as an educational platform for issuers and global investor communities. The overarching aim of the Working Group is to enhance transparency and convergence, and to ensure that there is a progressive common understanding of the covered bonds concept, with similar market solutions and infrastructures, and more important comparable regulatory treatments.

The Current State of Play and Outlook for Covered Bonds Outside Europe

Covered bonds represent a €2.6 trillion global asset class. Initially dominated by European issuers, the product is becoming increasingly relevant in many other markets, such as Australia, New Zealand, Canada, Singapore, and South Korea. The global financial crisis proved that covered bonds can be a resilient source of funding in times of wider market turmoil. Even in the European countries most affected by the crisis, such as Italy and Spain, banks were able to tap the covered bond market despite other sources of wholesale funding evaporating.

Issuers and regulators outside the traditional European markets duly noted banks’ ability to issue covered bonds in times of stress, and expedited the approval or the amendment of legislation governing the issuance of covered bonds. Covered bond issuance picked up quickly in most of these countries once the dedicated legislation was approved. Over the past few years, accommodative monetary policies in Europe and the Americas, and the European Central Bank (ECB)’s Covered Bond Purchase Program (CBPP3), have also created favourable conditions to establish covered bond programs in new countries.

Against this backdrop global issuers have, during the past decade, increased their share in the total covered bond print from merely 1% in 2008 to 8% in 2018. They even embody 11% of the EUR benchmark covered bond market and were responsible for 15% of the EUR benchmark issuance in 2018. We believe that market conditions will remain supportive for covered bonds in new jurisdictions in the next few years, despite the diminishing monetary support from central banks and the end of the ECB’s net asset purchases. Moreover, an expected increase in mortgage lending will drive bond supply by increasing lenders’ need for wholesale funding and the availability of eligible collateral. Finally, the legislative and regulatory environment remains favourable to covered bonds.

REGULATORY TREATMENT ON DIFFERENT TRACKS

Nonetheless, while the use of covered bonds as a source of funding is expanding across the globe, their regulatory treatment continues to differ. The preferential treatment of covered bonds for risk weight purposes or within the scope of the liquidity coverage and net stable funding ratio requirements is still largely a European phenomenon. Outside Europe, the treatment of covered bonds remains mostly aligned with the Basel stipulations, meaning that covered bonds are barely treated more favourably than senior unsecured instruments. Even the eligibility of covered bonds for central bank collateral purposes is not common place and typically restricted to national currencies.

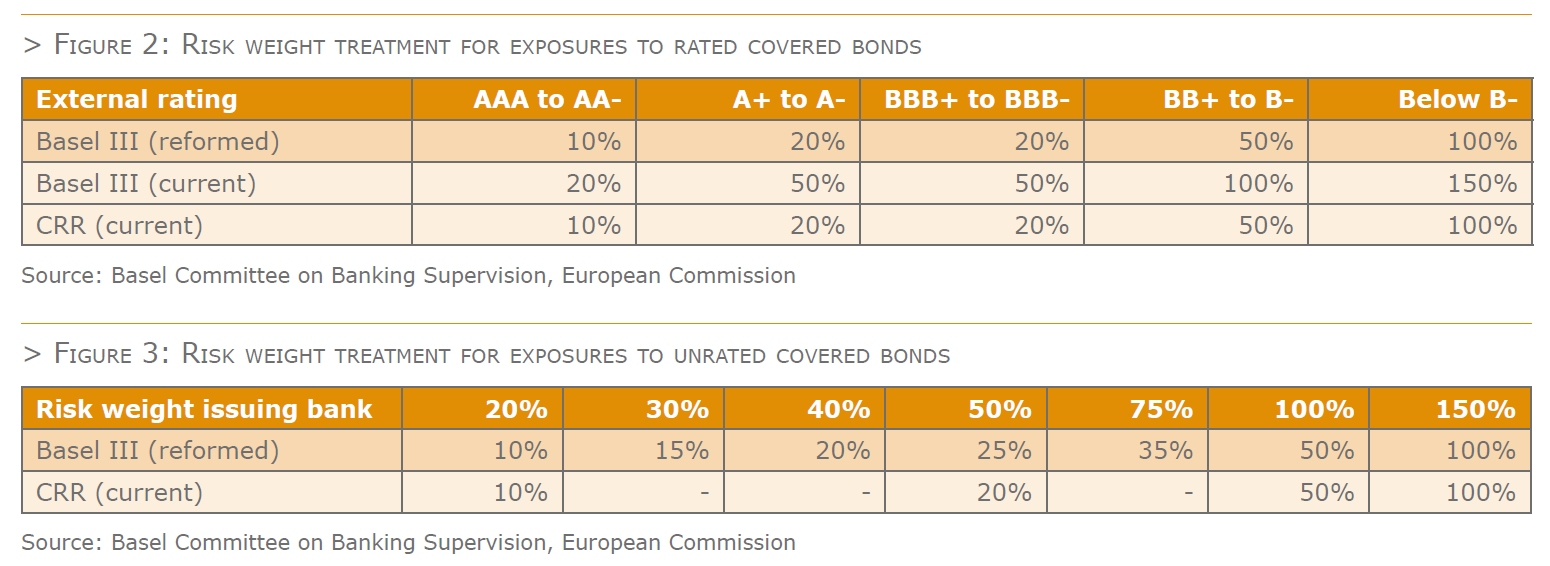

Nonetheless, the recognition and protection of the secure nature of covered bonds seem to be spreading beyond Europe. For instance, the Canadian regulator explicitly decided to shield secured liabilities such as covered bonds from the bail-in tool applicable to domestic systemically important banks (D-SIBs) under the Canadian resolution regime effective since September 2018. Furthermore, the Basel III reforms announced at the end of 2017 do provide for a more favourable risk weight treatment for covered bonds, paving the way for a preferential treatment of covered bonds on a global scale.

Basel III reforms pave the way for preferential risk weight treatment on a global level

In December 2017 the Basel Committee on Banking Supervision (BCBS) finalised its post-crisis regulatory reforms. These include preferential risk-weights for covered bonds on global level for the first time as of 1 January 2022. The requirements set by the Basel Committee are founded on the more general conditions according to Article 52 (4) of the UCITS-Directive and similar to the additional requirements according to the current Article 129 of the CRR.

Covered bonds are defined as bonds issued by a bank or mortgage institution subject by law to special public supervision designed to protect bondholders. Proceeds of bond issuance must be invested conform the law in assets that are, during the whole period of validity of the bonds, capable of covering claims attached to the bonds. In the event of a failure of the issuer these proceeds would be used on a priority basis for the reimbursement of the principal and the payment of accrued interest.

The eligible cover assets are restricted to public sector assets and to claims secured by residential and commercial real estate subject to LTV cut-off percentages of 80% and 60% respectively. Claims on banks (A- or better rated) are eligible up to 15% of outstanding covered bonds. Additional collateral may also include substitution assets and derivatives entered into for the purpose of hedging risks related to the covered bond programme. In contrast to Article 129 of the CRR, ship mortgages do not qualify as eligible assets.

While the transparency requirements are more or less in line with Article 129 of the CRR, Basel requires a nominal overcollateralisation of 10%, which goes beyond the requirements at European level. The European covered bond Regulation agreed earlier this year asks for a minimum nominal level of overcollateralisation of 5% on statutory, contractual or voluntary basis. Hence even where national legislations may not provide for the minimum (statutory) overcollateralisation level required for a preferential risk weight treatment, issuers themselves may decide to either contractually commit to or voluntarily hold sufficient overcollateralisation to meet the requirements. The Basel reforms do require issuing banks to publicly disclose on a regular basis that the 10% overcollateralisation target is met in practice.

The status on third country equivalence within the EU

In Europe, the equivalent treatment of covered bonds issued by non-EEA credit institutions was left outside the scope of the covered bond Directive and Regulation. Instead, the European Commission will submit a report on third country equivalence to the European Parliament and Council within two years after the provisions of the Directive have to be applied. This report may be accompanied by a legislative proposal on whether or how an equivalence regime should be introduced. However, EU member states are given 18 months to transpose the Directive into national law after it enters into force (expected September/October 2019), while the provisions of the Directive and Regulation will not have to be applied until twelve months after this transposition deadline at the latest. Hence, the timespan for the third country equivalence discussions in Europe may even stretch two years beyond the date the Basel III reforms should enter into force in January 2022.

Albeit one year shorter than the deadline initially proposed by the European Commission for the third country equivalence report, the two-year outcome is still less favourable than the European Parliament’s stance ahead of the trilogue negotiations. The European Parliament was of the view that the Commission is already able to start adopting delegated acts on third country equivalence to supplement the Directive. These acts would determine that “the legal supervisory and enforcement arrangements of a third country are I) equivalent to the Directive’s requirements on the structural features of covered bonds and covered bond public supervision, and II) effectively applied and enforced in an equitable and non-distortive manner in order to ensure effective supervision and enforcement in that third country”. The Parliament also argued that the Commission should, in cooperation with the EBA, monitor the effectiveness of the structural covered bond requirements in third countries and regularly report on this to the Parliament and Council. If the equivalent requirements would be insufficiently applied by third country authorities, or if there is a material regulatory divergence, the Commission could consider withdrawing the equivalence recognition based upon a pre-defined transparent procedure.

Even though the third country equivalence discussions will have a longer-term horizon, European regulators do seem committed to consider an equivalent treatment of third country covered bonds. Judging the European Parliament’s proposals for earlier adoption of delegated acts on third-country equivalence, the Directive’s structural requirements for covered bonds will probably be an important reference point for the equivalence assessments. Baring this in mind, the next paragraph provides some insights in the alignment of global covered bond regimes with the European covered bond Directive, building upon the work of the ECBC Global Issues Working Group.

Global Best Practices – To what extent are global regimes aligned with the EU Directive and Regulation proposals?

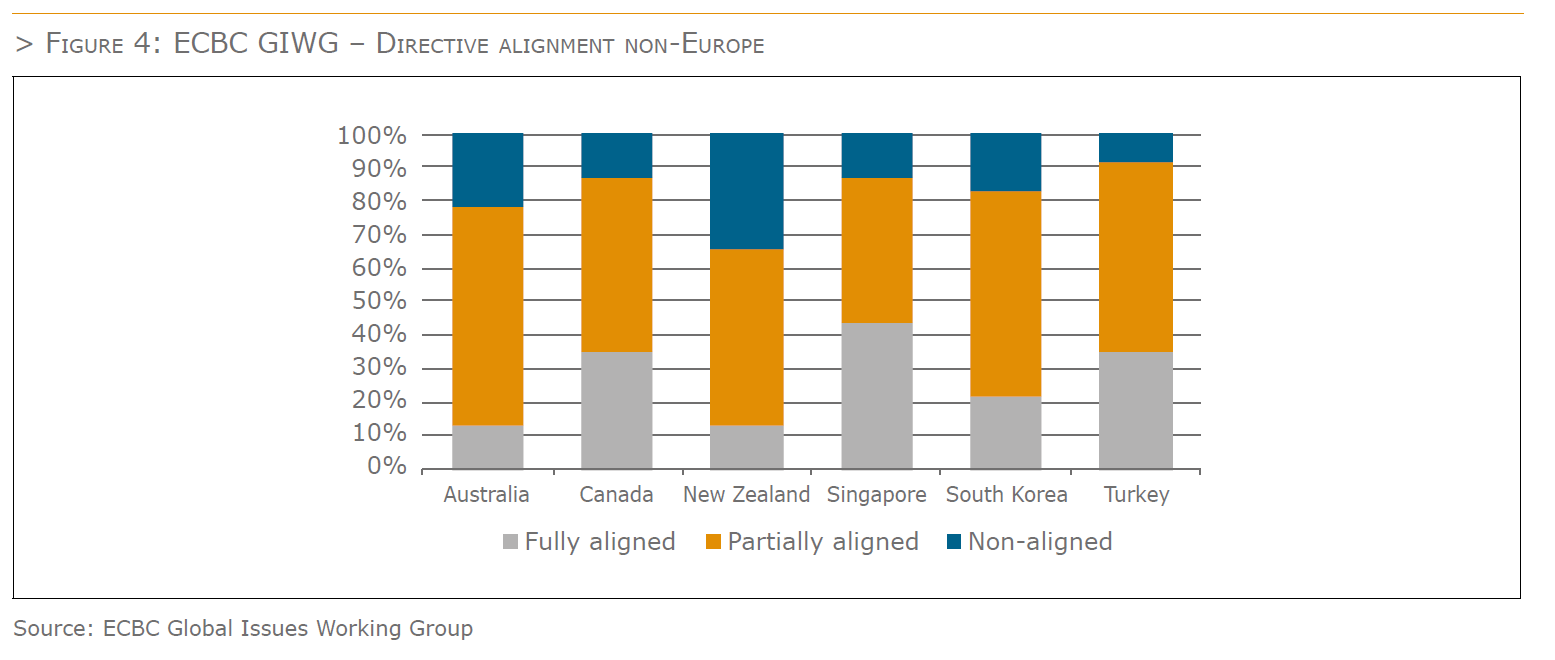

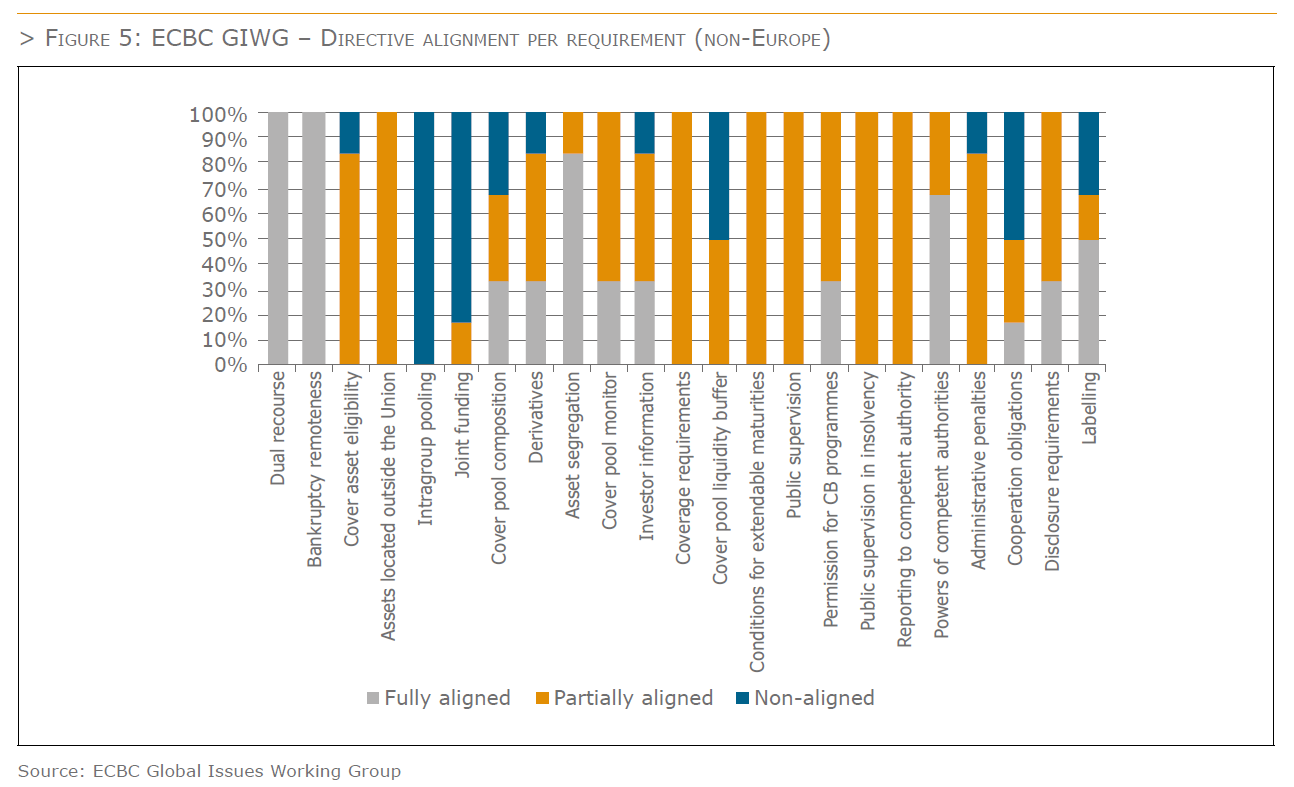

In the past few years, the ECBC Global Issues Working Group analysed on several separate occasions how different global covered bond regimes meet the proposals for covered bond harmonisation in the EU. The focus has been solely on the legal frameworks of the global jurisdictions with benchmark covered bond debt outstanding. In this section we provide an update of the most recent analysis based upon the EU covered bond Directive and Regulation in Europe as agreed in April 2019.

The results of the analysis reveal that most global covered bond regimes are fairly strongly aligned with the principles based EU Directive proposals. This is an important observation in light of any future EU third country equivalence assessment. Importantly, there is full alignment with the Directive’s dual recourse and bankruptcy remoteness requirements and almost all countries fully meet the asset segregation requirements. On the other hand, virtually none of the global regimes provide for intragroup or joint funding options. The non-alignment in this field is not particularly relevant, especially since for example the intragroup covered bond funding is just an option for national legislators. Hence there is no obligation to implement it.

Global covered bonds are for obvious reasons typically secured by assets located outside the Union. The Directive allows for inclusion of these assets in cover pools if these assets meet the Directive’s eligibility criteria and realisation of the assets is legally enforceable in a similar way to assets located in the EU. Most global covered bond regimes have established asset eligibility criteria and as such partially meet the Directive’s requirements.

For example, residential mortgage loans would generally be eligible up to the soft LTV limit of 80% specified in the (amended) CRR. However, not all frameworks explicitly provide for credit quality restrictions on exposures to institutions or third country public sector exposures, or provide for the required legal certainty or property valuation in line with the CRR language.

Global covered bond regimes do provide for nominal coverage, but are not always as detailed as the Directive with reference to the type of cover assets that should contribute to the coverage requirement, i.e. being the primary assets, substitution assets, assets held for liquidity buffer purposes or payment claims related to derivative contracts.

The minimum required nominal overcollateralisation level of 5% as specified in the covered bond Regulation, is only met by one country on the level of the legal framework (statutory). It is often met on an issuer-by-issuer basis on a contractual level. When the voluntary overcollateralisation is considered too, all jurisdictions would meet this requirement. According to the Regulation a lower overcollateralisation requirement of at least 2% may also be applied if the calculation of the overcollateralisation is either based upon a formal approach that takes into account the underlying risk of the assets, or on a formal approach where the valuation of the assets is subject to the mortgage lending value.

None of the global covered bond jurisdictions explicitly provides for a 180 days liquidity rule, even though other types of liquidity provisioning can often be found in global frameworks. Also, the use of extendable maturity structures is not specified by law. That said, while global legal frameworks lack objective extension triggers, maturity extension triggers are, where applicable, generally specified in detail in the contractual terms and conditions.

Global covered bond regimes are subject to covered bond public supervision, but would for instance not explicitly require, by law, that competent authorities should have the expertise, resources, operational capacity, powers and independence necessary to carry out the function of covered bond public supervision. Global covered bond regimes require permission from the competent authority to issue covered bonds, but some countries lack detailed requirements for permission. Provisions for supervision in insolvency or resolution are also often not as detailed as stipulated in the Directive, while there are notable differences between the global frameworks on the reporting requirements to the competent authorities. Not all global covered bond regimes fulfil the requirements for an independent covered bond monitor. But since this feature doesn’t have to be implemented by EU Member States, this should not be regarded as a misalignment with the EU Directive.

IN SUMMARY

The past decade’s growth of covered bond markets outside of Europe underscores the global recognition of covered bonds as a secure and important funding tool for banks, serving economic purposes. Nonetheless, the alignment of the regulatory treatment of EEA covered bonds and their comparables outside the block remains important work in progress. The introduction of preferential risk-weights for covered bonds in the Basel framework is a great success and could potentially further boost the use and investment in covered bonds worldwide. In Europe, it was decided to leave the potential equivalent treatment of non-EEA covered bonds outside the scope of the covered bond Directive, but not without commitment to assess the relevance hereof within two years after the Directive’s provisions have to be applied. The decent alignment of global regimes with the requirements of the EU covered bond Directive provides an encouraging starting point for a more harmonised regulatory treatment of covered bonds across the globe.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.