26 October 2023

The rapid monetary tightening implemented by the European Central Bank starting in the summer of 2022 is having its expected effects on the most interest rate-sensitive component of economic demand, and in particular the residential real estate market and housing loans. The purpose of this article is to provide a preliminary assessment of the impacts of the monetary policy turnaround on the housing market and the trend in residential mortgages, which are the main collateral for covered bonds. In the second part of this article, we take a closer look at the cover pools in different covered bond jurisdictions and analyse them in terms of various characteristics. This in-depth analysis allows us to elaborate on the impact of rising rates and the weakening of the real estate market on cover pools.

The increase in policy interest rates since July 2022 is unprecedented in the history of the euro, in terms of speed and scale. From July 2022 to April 2023 policy rates were raised by 375 basis points, bringing the deposit facility rate to 3.25%.

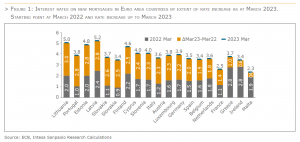

Due to the turn in monetary stance, credit access conditions have tightened, albeit moderately, and demand for loans decreased. Interest rates on mortgages went up significantly following the sharp rise in monetary policy rates. The cost of borrowing for house purchases increased by 2 percentage points in 2022 and 1Q2023 in the Euro area, to 3.4% in March. Several countries recorded a stronger rise, up to 3 percentage points, and reached a higher level, peaking at 5% in the Baltic countries. In some major countries, such as Germany and Italy, the average cost of borrowing for house purchase stood at about 4% in March 2023 (figure 1).

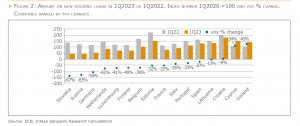

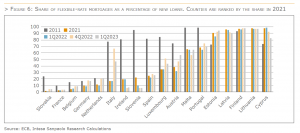

Rising rates, in turn, have contributed to a reduction in debt financing flows to households for house purchase. New production started decreasing among European countries, with just a few exceptions, while the stock of outstanding mortgages has been slowing down. In 1Q2023, in 14 countries the amount of new mortgages decreased, from -67% yoy in Slovakia and -63% yoy Austria to -9% yoy in Croatia. In just two cases, Ireland and Cyprus, new mortgages continued to grow in 1Q2023, posting double-digit increases (figure 2). Note that these countries were the only ones, among those under review, that in 1Q2022 had a lending volume in line with the pre-pandemic figures (measured by the 1Q2020 average in the absence of prior data for some countries). All other countries experienced strong growth in new mortgages over the two years up to 1Q2022, followed

more recently by a decline.

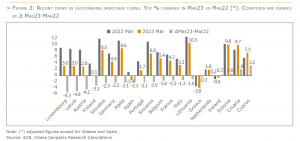

As a consequence of lower new gross production, the strong dynamics of outstanding mortgages started slowing down, from mid-2022 in a few countries and more clearly in the first months 2023 overall across the board. Nevertheless, mortgage stocks remain on the rise in most countries, by 3.3% yoy in March on average in the Euro area, down from 5.4% yoy in 1Q2022. On the contrary, deceleration led to a decline in Spain, by -1,4% yoy in March, after only returning to slight growth in mid-2021. Countries where the deceleration has been the most pronounced are Luxembourg, Latvia and Austria.

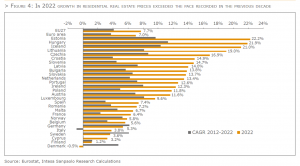

The moderation in the trend of housing loans is consistent with a weakening in the residential real estate market, where the long positive cycle is coming to an end as a consequence of much higher borrowing costs. In 2022 as a whole, house prices still showed strong growth, generally faster than in the previous ten years on average (Figure 4). Growth in house prices slowed down in the last quarter 2022 and there was a widespread reduction quarter on quarter. In countries reporting figures on transactions, the number of home sales started reducing in the last quarter 2022. Within this general picture, differences can be observed between countries. Where increases in house prices signal a risk of overheating, recent correction has been considerable, such as in Germany (-5.0% qoq in the last quarter 2022). Significant price reductions also occurred in the Nordic countries in the last quarter 2022 (figure 5). Based on preliminary data released in some countries and with reference to major cities, the downward price trend became more evident in 1Q2023.

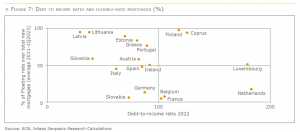

In this context, debt service and loan affordability are put under strain. Indeed, the sharp increase in interest rates could negatively impact the ability of households to repay their debts, especially those most affected by the reduction of real disposable income due to high inflation. In this sense, greater vulnerabilities could arise where the degree of household indebtedness is higher and/or the incidence of variable-rate mortgages greater. Over more than a decade of very low rates, in most countries the share of new variable-rate mortgage loans has fallen significantly, with a radical shift in preferences as a result of the smaller spread between fixed and variable rates. Due to the lower share of flexible-rate mortgages accumulated over a decade, households’ exposure to increases in debt service burden is limited overall. On the contrary, in 2022, as interest rates rose, household started to increase their recourse to floating-rate mortgages (figure 6), including those with a rate cap. This was especially the case during the first part of the upswing cycle in 2022, when the spread between fixed and floating rates widened due to the different speeds at which the two rates rose, the former faster and the latter slower. Recourse to flexible rates generally began to decline or almost stabilised in the first part of 2023, thus limiting the potential risks to the debt service capacity of European households. Moreover, in relation to income, debt generally remains lower in the euro area than in the United States. Very few countries record a combination of high indebtedness and high vulnerability to increasing rates (figure 7), measured by the share of floating-rate mortgages.

The developments on the real estate markets described above have the potential to affect covered bond issuers on various levels. On the asset side, the effects can be felt in relation to both existing and new business. The sharp rise in interest rates is leading to higher burdens for borrowers. This particularly affects jurisdictions with a high proportion of floating-rate loans or loans with a short fixed-rate period. The focus is also on jurisdictions in which borrowers primarily take out interest-only loans. Due to the lack of a repayment component, these loans are significantly more sensitive to interest rate hikes than financing with a regular repayment component. As described earlier, price corrections for residential real estate have so far been limited in most countries. High real estate price levels, combined with increased financing costs, are thus leading to lower affordability. Added to this are increased ancillary costs in the wake of energy price inflation in recent months. As a result, demand in the residential real estate sector has declined significantly, with a corresponding impact on new business. Moreover, the commercial real estate segment is also affected by a noticeable decline in demand. Thus, from a real estate investor point of view, alternative investments once again appear more interesting in the increased interest rate environment. In addition, structural changes in office and retail properties, for example, are having a lingering effect as a result of the Corona pandemic. On the liabilities side of the covered bond business, the focus is on issuing capacity and refinancing costs. The lack of a supply of newly originated mortgage loans limits the potential for new issues. Higher borrower risks could also have a negative impact on refinancing spreads.

Below, we take a closer look at selected cover pool characteristics in a wide variety of covered bond jurisdictions. The aim is to analyse in more detail the initial situation of the individual countries in the light of the rapidly changing real estate market environment. In our analysis, we have limited ourselves to ECBC label issuers that report their cover pool composition based on the ECBC Harmonised Transparency Template (HTT). From Austria and Germany, we have included a broader range of issuers. In total, the following analysis is thus based on 179 mortgage covered bond programs from 20 different jurisdictions.

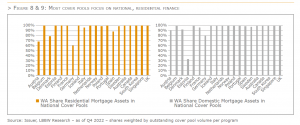

With regard to the type of mortgage financing, most covered bond laws do not contain any specific requirements concerning the composition between residential and commercial cover assets. Exceptions to this are, for example, the legislation in Sweden, Finland or Estonia, which impose a percentage restriction on the commercial share. In Canada, commercial real estate financing is generally not permitted in the cover pool. Also, in terms of regional focus, there are only a few jurisdictions that apply a purely domestic restriction. At European level, cover assets are mostly limited to countries in the European Economic Area.

In practice, however, it turns out that, with the exception of a few countries, most cover pools are purely residential. Residential cover pools are generally characterised by a broad spread of risk across a large number of borrowers and thus by a high degree of granularity. Larger commercial shares are found in German Pfandbrief cover pools. Here, the average share of commercial real estate financing is around 40%. However, the conservative mortgage lending value approach of the German Pfandbrief Act should be emphasised here as a risk mitigant. According to this, real estate financing may only be taken as cover up to the lending limit of 60% of the mortgage lending value. The mortgage lending value itself, in turn, only takes into account long-term, sustainable features of a property, leaving speculative elements out of the equation. As a result, the valuation of German cover pool assets has built up high valuation buffers against a potential decline in real estate prices, especially in recent years. Other jurisdictions, such as France, Austria, Poland or Spain, also apply conservative valuation principles for the real estate valuation of cover pool assets.

When looking at the regional distribution of cover assets, it is noticeable that most cover pools are characterized by a pure focus on domestic financing. Larger shares of foreign financing can be found in Germany, for example (∅ 20%). Usually, this relates to commercial real estate financing. In Denmark and Sweden, issuers also have isolated separate covered bond programs outstanding with financing from other Scandinavian countries. In France, the covered bond program of Axa Bank Europe SCF is an exception, which focuses purely on Belgian cover assets. In Estonia, on the other hand, Luminor Bank’s covered bond program stands out. The program reflects the efforts of the Baltic states to establish a pan-Baltic covered bond market. In the course of this, Luminor Bank also has financing from Lithuania and Latvia in its cover pool in addition to Estonian cover assets.

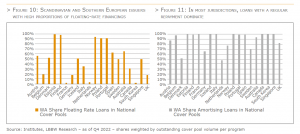

The sharp rise in interest rates in recent months has led to a particular focus on jurisdictions with a high proportion of variable-rate financing. In the covered bond context, floating rate loans should be viewed from two different perspectives. On the one hand, the sharp rise in interest rates is leading to a higher interest burden and thus to a higher expenditure burden for borrowers. The consequences could be a deterioration in portfolio quality at the financing banks with a view to rising NPL ratios and higher risk provisioning requirements. From a refinancing perspective, on the other hand, a mortgage portfolio with a high proportion of variable-rate loans is positive after an issuer insolvency, since – assuming that borrower payments continue to flow regularly – the portfolio is valued more closely to the market.

Jurisdictions with a high proportion of interest-only loans also experience greater burdens, as these are subject to higher interest rate sensitivity. Accordingly, a rapid and sharp rise in interest rates for interest-only loans leads to noticeably higher interest charges than for loans that provide for regular repayment of the loan amount.

Cover pools with a high proportion of variable-rate loans are particularly common in Scandinavian countries such as Finland (consistently with above-mentioned figures on mortgage flow composition), Norway, Denmark or Sweden. However, higher levels can also be found in Portugal, Spain and Austria, for example.

With regard to repayment terms, it is clear that most covered bond jurisdictions provide for regular loan repayments. Countries with higher shares of interest-only loans are mainly located in Northern Europe with Denmark, Finland and Sweden. The Netherlands also stands out. In German cover pools, higher proportions of interest-only loans are predominantly associated with commercial real estate financing.

In the jurisdictions concerned, the risks arising from the rise in interest rates are cushioned by a wide variety of measures or basic prerequisites. In many countries interest rate stress tests are already carried out when loans are granted, simulating a sharp rise in interest rates of 5 percentage points for example. In addition, macroprudential instruments have been used in some countries in recent years to encourage banks to limit the granting of loans with variable interest rate structures or interest-only repayment structures. In addition, low unemployment and strong economies mean that borrowers in the Nordic countries in particular are able to shoulder higher burdens.

A look at the non-performing loan ratios in the mortgage sector also reveals a comparatively comfortable starting situation. At the European level, a steady downward trend has been observed in this area in recent years. Accordingly, the EBA Risk Dashboard shows an average NPL ratio of 1.5% for European residential real estate financing for the end of 2022. For commercial real estate financing, this figure recently averaged 3.7%. In terms of cover pools, NPLs mostly play a negligible role. Our evaluation shows an average NPL ratio of just 0.06% across all covered bond programs analysed.

In order to ensure that covered bonds are risk-privileged for investors, issuers must, among other things, comply with certain regulations with regard to LTV limits as well as overcollateralisation levels. The relevant requirements for this can be found in Article 129 CRR.

With regard to LTV limits, most national covered bond laws have aligned themselves with CRR requirements, which set a maximum limit of 80% for inclusion in the cover calculation for residential loans and 60% for commercial loans. A sharp decline in real estate prices could lead to a reduction in the eligible portion of the cover pool, which would subsequently limit the issuance potential. An analysis of the average (indexed) LTVs for the residential portion in each jurisdiction shows that comfortable buffers are generally available. Accordingly, average indexed LTV levels of around 50% can be observed in most cases. It should also be noted that in some jurisdictions the underlying assets are valued on the basis of the mortgage lending value, which offers additional buffer for potential further devaluations.

As part of EU covered bond harmonisation efforts, a specific overcollateralisation requirement was included in the CRR. In principle, a nominal overcollateralisation of 5% is provided for here. A lower overcollateralisation requirement may be established by national legislatures if the calculation either incorporates the underlying risk of the assets or the valuation of the assets is based on the mortgage lending value. In this context, a nominal overcollateralisation level of 2% must be met. Additional overcollateralisation requirements may also arise according to requests from rating agencies. A concrete look at individual jurisdictions shows that in most cases comfortable overcollateralisation levels are in place that go far beyond the statutory requirements. However, there are wide ranges among the individual issuers. The management of the overcollateralisation can be assured via a wide variety of measures. For example, in addition to the inclusion of further primary cover assets, the overcollateralisation can also be managed to a limited extent by the addition of substitute cover assets.

Liquidity risks are also dealt with by maintaining a 180-day liquidity buffer. This mandatory buffer is part of the covered bond definition under the EU Covered Bond Directive, the requirements of which have had to be applied at national level since July 8, 2022.

Covered bonds are typically structured as dual recourse instruments. Thus, the investor benefits from the dual recourse to both the issuer and the cover pool. As long as the issuer is not insolvent, covered bond payments are made from the cash flows of the issuing institution. Irrespective of the cover pool characteristics described above, the credit quality of the covered bond is therefore also highly dependent on the issuer’s credit rating. A look at the rating landscape in the covered bond universe shows that across all rating agencies covered bond issuers mostly have a stable or even positive rating outlook, with a share of more than 90%. For additional rating stability, corresponding notches provide buffers against a downgrade of the issuer rating.

Conclusion

Central banks’ quantitative tightening measures – and in particular the sharp and rapid interest rate hikes – led to an abrupt interruption in the dynamic development of the European real estate markets in recent years. As a result, there was a sharp drop in transaction volumes. In recent quarters, the first effects on price developments have also been observed. The issuing capacities of covered bond issuers and the asset quality in the cover pools are closely linked to real estate market developments. However, not least specific national covered bond legislation ensures that the covered bond programs have a wide variety of safeguards that can cushion negative developments on the real estate markets. These include, for example, requirements for overcollateralisation, LTVs, liquidity buffers and the valuation of the underlying mortgage collateral. The specific analysis of individual cover pools in various covered bond jurisdictions also shows that numerous buffers are currently available, e.g. in the form of comfortable overcollateralisation and low LTV ratios. Increasing regulation and the higher capital requirements often associated with it have also ensured that issuers are in a comparatively comfortable position to weather the current stormy real estate market environment.

by Elisa Coletti, Intesa Sanpaolo, Karsten Rühlmann, LBBW

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.