13 September 2017

Société Générale conducted an investor survey in May/June 2017 among covered bond investors. Our survey results show that although the investor base remains loyal to covered bonds – 63% of respondents state they plan to keep their CB holdings unchanged – the decreasing liquidity in the market is a big challenge and many real money investors are much less active in secondary. All in all, the results are encouraging, although investors are concerned about the effects the prolonged ECB QE programme will have in the market and most respondents expect a widening of spreads in 2H 2017.

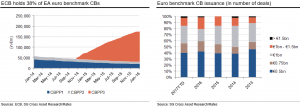

Given the continued CBPP3 purchases, secondary market liquidity has all but dried up and investors are crowded out. As can be seen from the charts below, the allocation to central banks continues to increase, including for longer-dated EZ covered bonds. Although ECB CB purchases have fallen since early-2016, the reinvestment of maturities and the fact that the ECB continues to focus on primary given the lack of liquidity in secondary means we expect further crowing out of investors.

63% of the investors surveyed plan to keep their allocation to covered bonds in 2H17 unchanged, compared with 21% who intend to decrease their CB holdings and 16% who expect to increase holdings. Most will try to replace redemptions via primary – when possible given price inelastic central bank demand – if the levels look attractive, because holding cash is costly.

With regards to swap spreads, most investors feel spreads have reached a very tight level in ASW terms and believe they will widen by year-end, although many believe periphery EA CBs will underperform core EA CBs. That said, a number said periphery EA CBs – trading at wider ASW levels than core EA CBs – could tighten further and outperform EA CBs, particularly in a context where the macro environment is still as supportive, and the pace of inflation allows the ECB to take its time on its next move.

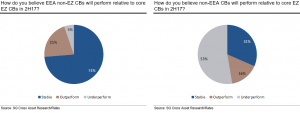

When analysing the potential performance of non-EZ CBs, respondents believe EEA CBs will perform stable to core EZ CBs, whereas they believe non-EEA CBs will be stable/slightly underperform.

With low yields, ongoing CBPP3 purchases and bank deleveraging, liquidity is still a major cause of concern for investors. The survey results confirm what investors have been telling us in recent meetings: liquidity has worsened significantly vs one year ago and the ticket sizes are becoming smaller, making switches difficult. There are a number of reasons for this. Firstly, the investor base in covered bonds has changed, with more buy-and-hold type investors (central banks, bank treasuries), affecting liquidity conditions. Secondly, with bank deleveraging and increased regulatory requirements (capital constraints, NSFR, LCR…), dealer’s covered bond trading books have shrunk significantly compared to a few years go. And thirdly, the ongoing pace of the ECB’s CBPP3 purchases, particularly in primary, together with a lower pace of issuance than last year and a relatively high share of €500m issues, does not help matters.

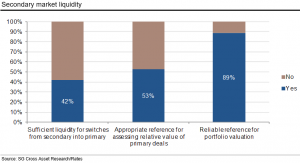

According to our survey, 42% judge secondary market liquidity to be sufficient for switches from secondary to primary, 53% consider it an appropriate reference for assessing relative value of primary deals. That said, 89% believe it is a reliable reference for portfolio valuation.

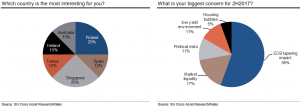

Despite the difficulties in sourcing paper in primary, investors remain confident that once the ECB’s QE ends, liquidity will improve. When asked which country is the most interesting from a risk/reward perspective, responses varied from well-established jurisdictions (Spain, Ireland, Australia), to new CB jurisdictions (Poland, Singapore, Turkey).

Most investors we surveyed – as well as those whom we have spoken to recently – are concerned about the crowding out effect of QE and the potential repricing that may ensue once the ECB stops dominating the covered bond market. Others are worried about the decreasing liquidity in the market due to continued CBPP3 purchases and decreasing supply expectations for 2H17 given: 1) bank balance sheets continue to decrease, 2) cheap central fund options available, and 3) the focus by banks on MREL/TLAC eligible debt. Investors surveyed also mentioned political risks as the biggest concern this year, given elections in some countries, Italian politics and ongoing Brexit negotiations. Finally, other challenges mentioned were the low yield environment and the fact that risks are not correctly priced in at the current squeezed spread levels and potential housing bubbles (Australia and Canada were specifically mentioned). Contrary to the responses we received a year ago when we conducted this survey, none of the respondents cited negative yields as a concern.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.