12 July 2016

By Ane Arnth Jensen, Managing Director, Association of Danish Mortgage Banks

By Ane Arnth Jensen, Managing Director, Association of Danish Mortgage Banks

In Denmark transparency plays a key role on the housing and mortgage markets – including the market for covered bonds, where two thirds of all outstanding lending are funded.

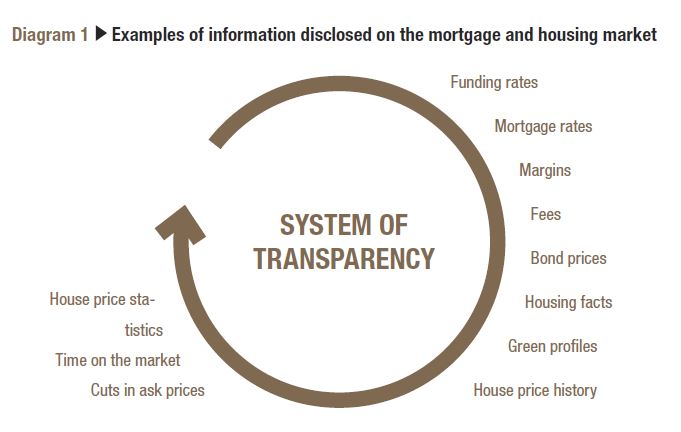

Many places mortgage and housing markets are to some degree characterised by asymmetric information as one party has more or better information than the other. In Denmark, the mismatch of information is minimised due to an ecosystem of transparency and digitalisation.

The system involves home-buyers, real estate brokers, mortgage banks, investors and authorities. The high degree of transparency and digitalisation is part of the explanation for Denmark’s high degree of mortgage financed home-ownership, mobility and the extremely low – and in some cases negative – mortgage rates.

All properties in Denmark are registered in a public data repository available online. The register contains detailed information on age, size, building materials, renovations, utilities, trade information, etc. On top of that, real estate brokers are required by law to provide data in a standardised manner for all properties that are listed for sale. The Association of Danish Mortgage Banks also publishes a number of market statistics. Among these especially the Housing Market Statistic serves as a useful tool for potential home-owners as it compares actual prices with listed prices.

Together with other available online information, it makes it easy for potential home-owners to access whether or not the asked prices are fair, because it can be compared with prices on similar properties, price history, differences in size, quality characteristics, etc. The information can also be used for potential buyers to bargain a lower price. If a property for sale has been on the market for long with significant price cuts, it indicates that the potential seller would be more willing to negotiate.

The high level of digitalised accessible information creates competition and gives sellers an incentive to invest in improvements that make the property more attractive. As the property is listed for sale, the seller has a possibility to supply three technical reports conducted by specialists on the property. One reports the current upkeep of the property, and points out deficiencies which should be addressed. The second report attaches an energy efficiency grade to the property, and the third is a report on the electrical installations in the property. Combined with relatively high taxes on energy, this gives a potential seller an incentive to make green improvements to obtain a higher grade. In other words it could be good business for a potential seller to invest in energy improvements that are not visible (ex. insulation), because it is most likely it would result in a higher price.

When buyers and sellers have found each other, and agreed on a price, the property typically has to be financed. The Association of Danish Mortgage Banks hosts a price comparison portal showing mortgage rates, fees and margins on loans in all mortgage banks in Denmark offering residential loans. The rates are to some degree indicative, because the actual rates are market based as mortgage banks issue bonds to fund the mortgage loans. The bonds are then sold to investors at the prevailing market price. The borrower receives the proceeds from the bond sale and uses it to buy the property.

Borrowers are certain that they will get a fair price on the bonds sold as there is full disclosure on post-trade information. In the new MiFIDII (Markets in Financial Instruments Directive) that comes into effect in January 2018, similar rules will apply for bond markets in other EU countries. In Denmark, all post-trade information has to be reported to the Danish stock exchange – also the many trades carried out over-the-counter. Most information is reported three minutes after the trades are closed. Information on big trades exceeding approximately EUR 14 million can be postponed to the end of the day. This option is only used for four out of ten times a big trade hits the market.

Borrowers can redeem their loans by having the mortgage bank buy back the same bonds issued when the loan was granted. The bonds can be bought back anytime also for refinancing purposes. Since the Danish covered bond market is highly liquid, borrowers can follow prices on the bonds funding their loans on a daily basis. If prices are lower than the initial price when sold, borrowers can cash-in the price difference. If prices are higher than the initial price, borrowers are protected by a price ceiling of par.

The interest rate payments and repayments from the borrower are passed directly through to investors. Danish mortgage banks are merely intermediaries and require a fee from the borrower. The fees are denoted in percentage points and can be interpreted as mortgage banks’ margins. This model of transparency creates competition: Mortgages banks can compete on margins to attract costumers who are certain to get the full benefit of changing market conditions due to the market-based principles with 100 per cent pass through.

When a property has been sold and financed, deeds and loans are registered to the authorities through a digital application process. The public registration does not require any physical signatures, as the application is processed online. It only takes the authorities one day to process the applications – and for the property to officially have a new owner.

The ecosystem of transparency ends when all the information is aggregated into market statistics, many of which the Association of Danish Mortgage Banks publishes. This gives policy makers and analysts a good picture on variables like mortgages rates, the supply of credit, demand for housing, the green profiles on housing, etc.

In the same way that the high degree of transparency minimises the costs of asymmetric information, the high quality of statistics enables policy makers to take informed decisions. For instance, analyses – partly made on mortgage data – have concluded that Danish households have robust finances and are resilient to an interest-rate hike or a prolonged period of unemployment. Previously it was a common perception that the high household debt made Danish households vulnerable.

On top of that, the Danish authorities have taken measures to counter risks. The measures include a supervisory diamond with five macro-prudential requirements governing mortgage banks, a requirement of a 5% down payment and guidelines to ensure sufficient caution is taken in the loan-granting process in metropolitan areas.

The Association of Danish Mortgage Banks will continue to work for as much transparency and digitalisation as possible, because it reduces the cost of asymmetric information and strengthens competition both between sellers, mortgage banks and investors. In the end it contributes to maintaining a model of cheap and flexible mortgages in Denmark.

This article was first published in the EMF-ECBC newsletter Market Insights & Updates in June 2016. Please note that any views or opinions expressed in this article are those of the authors and not necessarily those of the EMF-ECBC. This article does not constitute investment advice.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.