29 January 2016

By Luca Bertalot, Secretary General, EMF-ECBC

By Luca Bertalot, Secretary General, EMF-ECBC

Investment in energy efficiency is one of the most cost-effective ways to reduce the EU’s reliance and expenditure on energy imports, costing over €400 billion a year. While energy efficiency investments have been occurring gradually for decades, today the EU finds itself in a situation where these investments have become of strategic importance due to the high level of energy imports required by the EU bloc, energy price instability and the need to transition to a competitive low-carbon and resilient economy.

Indeed, the energy efficiency debate is knocking at the front door of every European citizen’s house and it is also taking centre stage in institutional and capital market debates. It is clear that investment in energy efficiency has a fundamental and beneficial role to play in the transition towards a more competitive, secure and sustainable energy system with an internal energy market at its core. Nonetheless, in our view, a crucial question remains open and difficult to answer for the European Institutions: how can a bridge be built between the energy efficiency investments required and the private capital markets financing these? Should the EU rely only on fiscal support to boost energy efficiency investments or is there a role to be played by private finance?

Particularly since the COP21 Agreement in Paris in December 2015, it is clearly of strategic importance for the EU to engage multiple stakeholder groups and scale-up the use of several financial instruments within a clear and enforced “carrot and stick” legislative framework. However, this might not be sufficient: we also see the need to engage the financial services sector to trigger a mechanism according to which each and every EU citizen is incentivised to adopt energy efficient behaviour, and to trigger the market consensus of a broad spectrum of stakeholders and institutional support with a pan-European scope of action.

Against this background, is there a role to be played by the mortgage industry? Is it possible to incentivise a capital markets-based financing system which would help the EU to meet the requirements agreed in December in Paris? What are the energy efficiency parameters which should be adopted in order to ensure simplicity, materiality and to avoid the speculative trends associated with “green washing”? Do we have the pillars with which to build a business case for the financing of energy efficiency? These are questions which are currently being discussed by the major mortgage lenders of the Old Continent, which are in the midst of one of the most important phases of transition perhaps ever experienced, reorganising their business models as a result of the massive regulatory changes implemented in the years since the crisis. In addition, and perhaps more importantly, they are also facing high market volatility and fundamental demographic changes with unprecedented macroeconomic and social implications.

The energy efficiency debate presents two major challenges for the mortgage industry: firstly, how to contribute to the long-term financing of energy efficiency solutions for housing; and secondly, how to adopt a harmonised approach within the EU against a background of heterogeneity of housing markets and of citizens’ behaviour and expectations towards both housing and the energy efficiency debate.

Almost one third of the EU’s energy consumption is attributed to households. Consequently, a reduction in the energy consumption of housing units would enormously facilitate compliance with the COP21 Paris Agreement. The barriers to renovating buildings for energy efficiency purposes are well known and require multiple solutions that should be implemented consistently and in a coordinated manner. Unlocking financing in order to render the EU’s residential building stock more energy efficient will require not only a long-term vision but also policy breakthroughs to allow for more than one barrier at a time to be overcome.

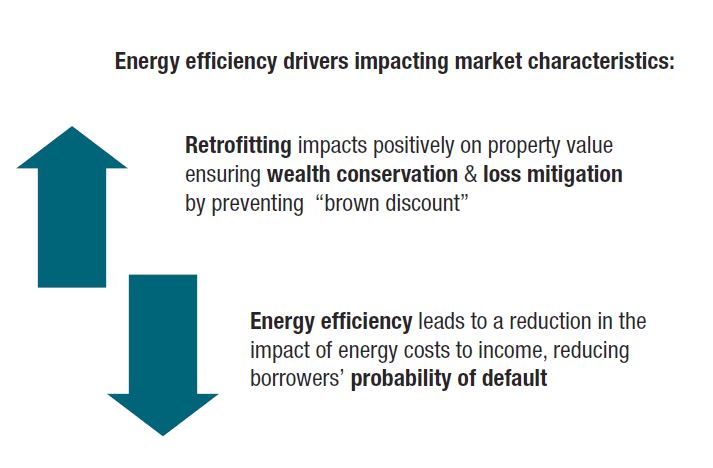

We are also all aware that the long-term lack of energy efficiency investments could have a detrimental impact on property values in the future.

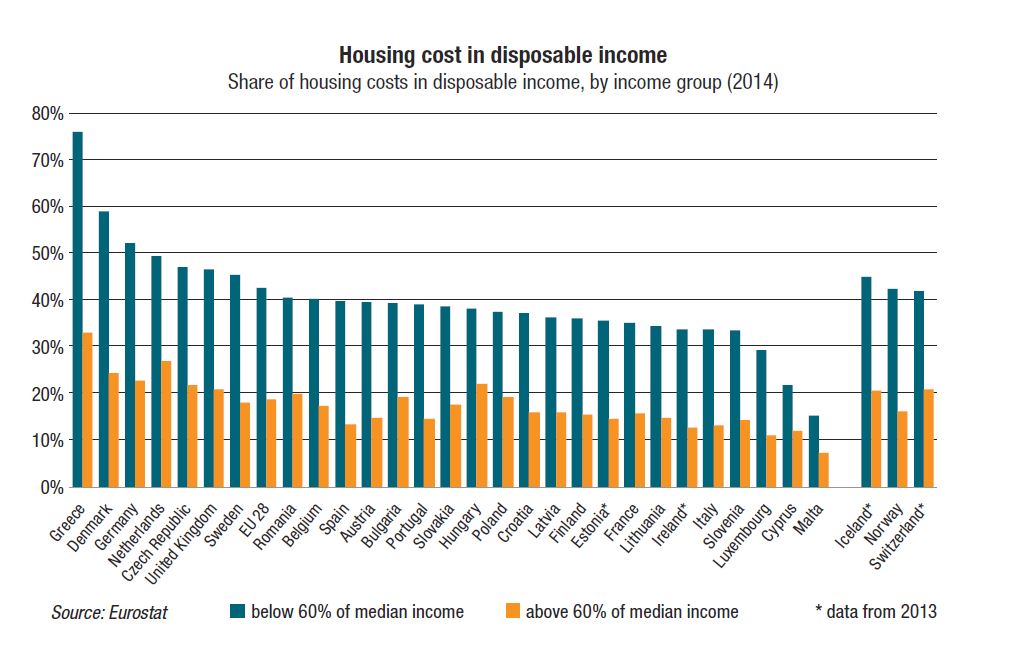

We consequently have to factor-in a potential “brown discount” element when analysing future values and the impact on banks’ loss mitigation capabilities. With public finances under pressure and a low spread and high market volatility environment, this consideration could be particularly relevant for the due diligence of investors and issuers, especially when monitoring nonperforming loans, property values and, from a more political point of view, when analysing housing cost impacts on disposable income or citizens’ capability of wealth conservation.

As such, a financing initiative in this area could entail the following: a borrower willing to retrofit his/her housing unit in an energy efficient manner would have access to a preferential channel of financing, which would provide a “green discount” to be factored into the mortgage, providing the retrofit works fulfil a series of material energy saving parameters. From a practical and material perspective, an improvement in energy savings due to retrofit works in a “ménage” would improve the capacity of the household to meet its financial commitments, thereby reducing the associated risk for the lender. This causality emerges from analysis carried out in the US market, which indicates that the default risk of the “energy efficient” borrower declines progressively as the energy efficiency rating of the home is improved. If this trend were to be confirmed in the EU, conceivably this could trigger an institutional reflection at European Commission and Basel Committee level with regard to a discount in the capital charge for an “energy efficient” mortgage.

In the spirit of developing a common understanding, specific competence and synergies amongst stakeholders involved in energy efficiency, and also its financing, the EMF-ECBC is organising a stakeholder and institutional Roundtable in Brussels on the 26th of February 2016, the objective of which will be to analyse the potential creation of an Energy Efficiency Label for mortgages and a related data “warehouse”. In this context, the EMF-ECBC will bring together the European Commission, the Basel Committee on Banking Supervision, the United Nations, the World Bank, energy efficiency specialists, building constructors, energy efficiency contractors, the valuation profession, property owners, issuers, investors and lenders from Europe and beyond.

The EMF-ECBC, for its part, is committed to analysing this issue very carefully from a market perspective according to a holistic and gradual approach. The Industry is keen to understand the feasibility of building a business case for the financing of energy efficiency, on the basis of a clear incentive chain, which would generate benefits for the borrower, the lender, the investor and, ultimately, the environment.

This article was originally published in the EMF-ECBC Market Insights & Updates newsletter in January 2016. More information on the EMF-ECBC’s Initiative on Energy Efficient Mortgages can be found here.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.