28 June 2018

Introduction

2018 started in the same manner that 2017 ended. According to the European Commission’s forecast, growth rates for the EU and the Euro area beat expectations in 2017 to reach a 10-year high at 2.4% with unemployment rates continuing to fall, now even below pre-crisis levels. Consumer price inflation weakened in Q1 2018, but it is expected to pick-up slightly in the upcoming quarters. In this overall favourable environment, the mortgage and housing markets in the EU continued, on average, to grow, but different dynamics in the various EU Member States need to be considered. Macroprudential tools and government-led decisions in general tend to counterbalance the growing lending dynamics through new recommendations on LTV and DTI, and to stimulate appetites for more fixed rate mortgage loans. House prices are generally increasing, although in some countries clear shifts towards a deceleration or even contraction can be seen. Mortgage rates seem to have reached their floor and, in several countries, the overall trend is of a timid increase coupled with more interest for longer initial fixation periods in new lending deals.

1.1 Market development

In the first quarter of 2018, the outstanding mortgage loans in our EU sample[1] reached EUR 6.8 tn. and increased by 1.9% year-on-year (y-o-y). On the other hand, gross lending figures decreased by 2.1% y-o-y to EUR 263 bn. These dynamics build on the heterogeneous developments experienced by the various countries. The overall positive trend of new mortgages is principally due to the ongoing improvement in economic fundamentals, low interest rates and an increase in consumer confidence.

Gross lending overall increased y-o-y in all but three countries, namely in Belgium, France and Italy. In Belgium, the contraction can principally be explained by the 47% contraction of re-mortgaging with respect to Q1 2017. Moreover, once re-mortgaging is excluded there has been a slight increase, principally due to the 2.3% increase in loans for house purchase and, considering the volume of mortgages granted, the Q1 2018 figures reached with EUR 7.8 bn., an all-time high for the first quarter. In France, there has been a contraction of 16% with respect to the same quarter in the previous year due to a contraction in new lending for both the existing and the new housing markets, the latter of which is expected to face a further contraction in the upcoming months due to the phasing-out of an individualised housing assistance for new housing purchases. In Italy, a contraction of around 20% y-o-y has been registered in Q1 2018, which is principally due to the very high number of new lending granted during the beginning of 2017.

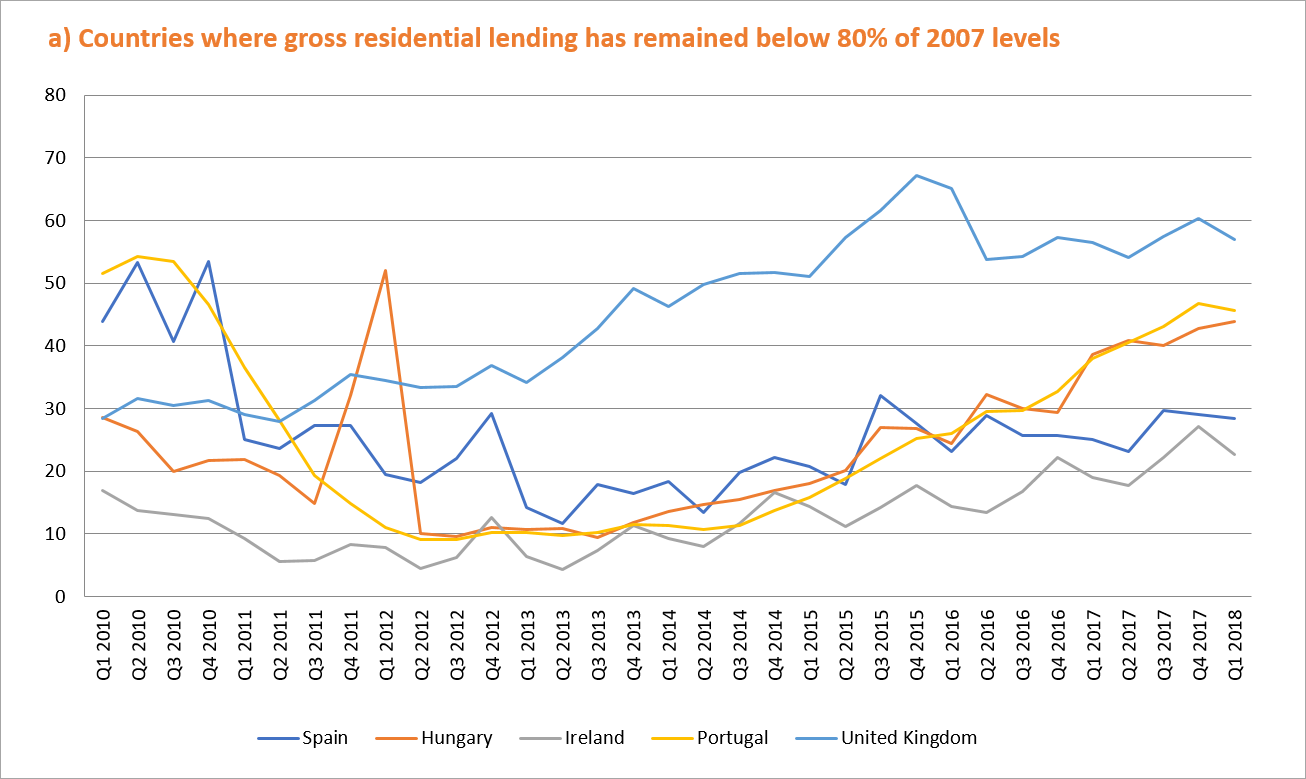

On the Iberian Peninsula, gross lending is increasing by double-digits, but the figures for the outstanding mortgage market are slightly contracting. In Portugal, new bank loans for house purchase increased by over 20% y-o-y to levels approaching those of 2011, although they are still only around 40% of the pre-crisis peak reached in Q3 2007. Even if there has been a 5.3% contraction with respect to the previous quarter, mainly due to lack of new listings, in y-o-y terms new loans continue to show a growing trend since Q2 2013. In Spain, both transactions and gross residential lending volumes increased by 8% and 13.2% y-o-y respectively, which have almost stopped the ongoing contraction of the mortgage outstanding figures.

Ireland, with over a 22% increase in y-o-y gross lending, has expanded its volumes the most in the Euro area. Data also shows that mortgage drawdown volumes grew by 13.5% y-o-y to 7,900 and that purchase mortgage drawdowns rose to 6,402, the highest Q1 level in the last 10 years. Mortgage approval volumes rose by 1.9% y-o-y to almost 9,600. Mortgage-holders are free to switch lenders and they account for 12.3% of approvals, almost four times their share in Q1 2015, while mover purchasers dropped to 27.1% from 33.2% over the same period.

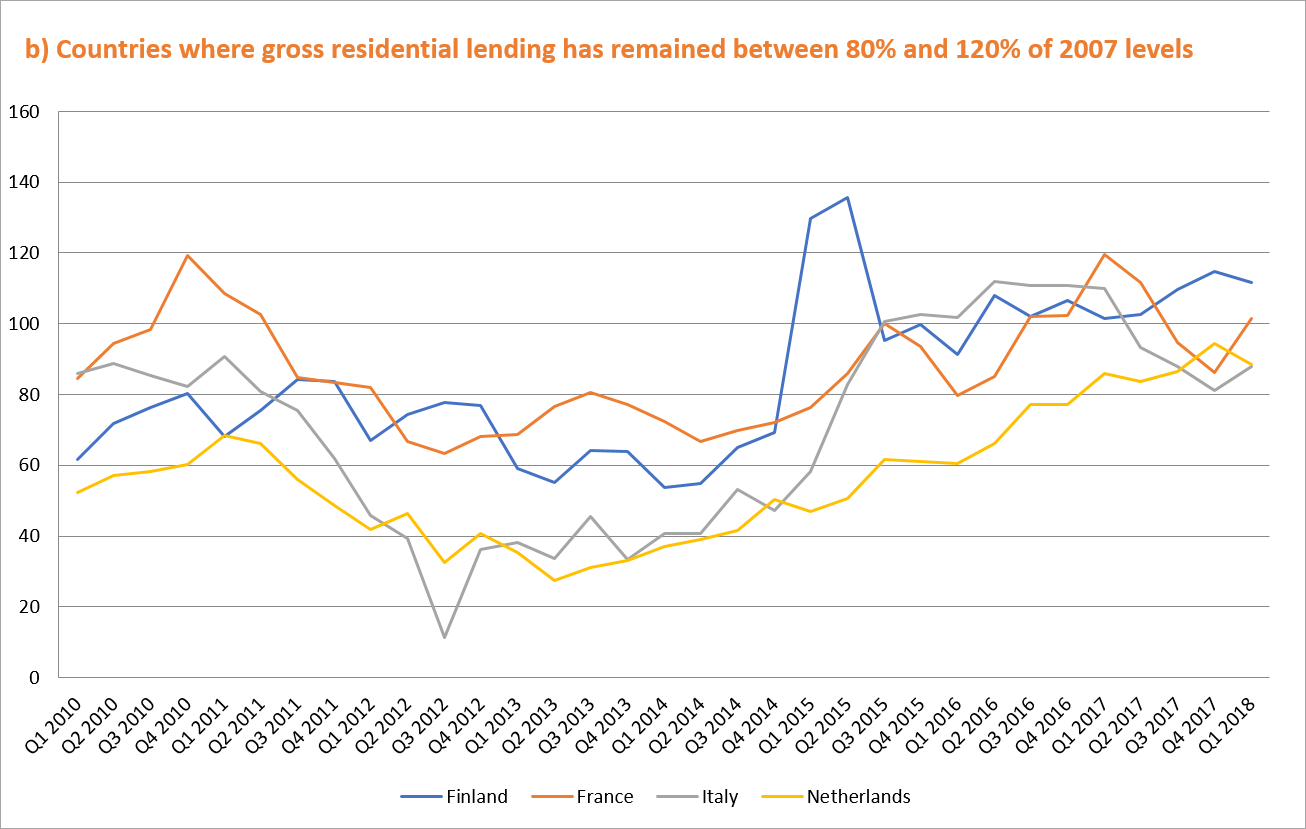

Both in Germany and in the Netherlands steady gross lending and outstanding mortgage lending increases y-o-y were registered in Q1 2018. A similar picture is seen in Finland, where housing loan demand has increased by 1.2% y-o-y. Likewise, construction activity is still strong due to high demand from investors. Foreign investors in particular have recently purchased large residential portfolios both in Helsinki and in other large cities.

Outside the Euro area, the mortgage market picture show an overall expansion which has been slightly dampened in EUR terms by the depreciation of domestic currencies.

In Sweden, in Q1 2018 the outstanding mortgage growth was 7.1% in SEK terms on a y-o-y basis (0.7% contraction in EUR terms), due to the well-known improving economic fundamentals but also due to a dysfunctional rental market which is subject to a general rent control in the growth regions. In the UK, overall outstanding and gross lending increased by respectively 3% in Pound terms and by around 0.7% in EUR terms with respect to Q1 2017. However, the different sections of the housing market are currently following rather different paths. First time buyer numbers (FTB) continue to hold up well, supported by a continuing range of government schemes to boost affordability. But the number of home movers, in the absence of any such assistance schemes, remains at depressed levels and buy-to-let (BTL) purchases, already at much lower levels than in recent years following a number of tax and regulatory changes designed to dampen activity, are still on a downward trend as the full effect of the removal of mortgage interest tax relief has yet to feed through fully. Re-mortgaging, however, is very strong, both in the residential and BTL spaces. This is a product of large volumes of fixed rate mortgages becoming available for refinancing, coupled with the continuing prospect of a Bank rate rise this year. In Denmark, while long-term mortgage rates scaled up in the early part of Q1 2018, subdued re-mortgaging activity dampened the overall new lending figures. Transaction activity in the housing market remained solid keeping overall demand steady.

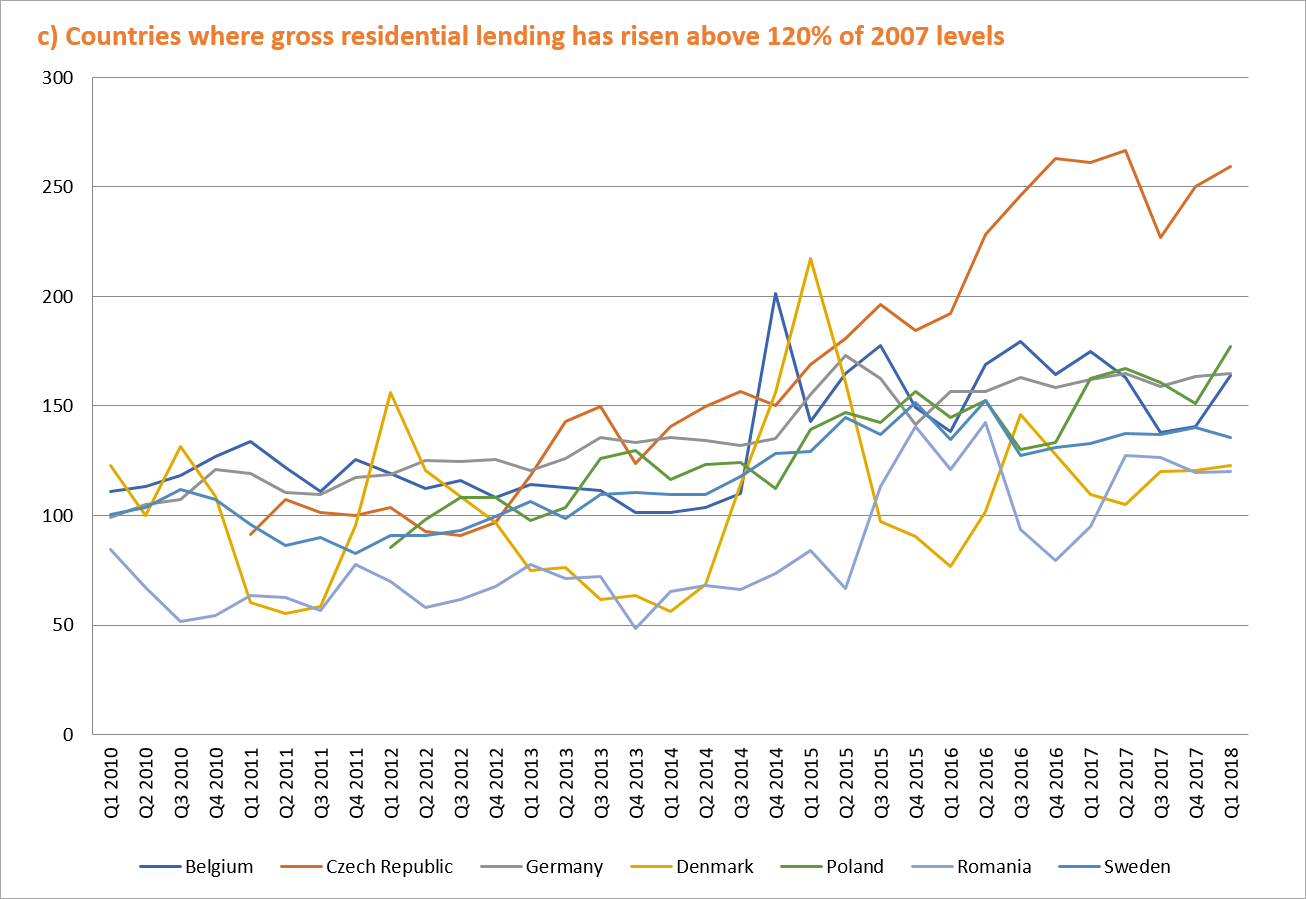

In Central and Eastern Europe, the mortgage market shows expanding y-o-y figures. In Romania, mortgage credit grew by 14% y-o-y and by 2.2% quarter-on-quarter (q-o-q). NPLs reached 3.2% in Q1 2018, decreasing by 0.05 pps compared to end 2017 and by 1.5 pps with respect to Q1 2017. In the first months of 2018, local credit institutions marginally tightened their credit standards on loans for house and land purchase, and left unchanged those for consumer credit. In Poland, 2018 began with a large increase in mortgage lending. The total number of new loans exceeded 55,000, a 23% increase with respect to end 2017, marking the largest figure since 2011. The average amount of mortgage credit in Q1 2018 was around PLN 235,000 (nearly EUR 56,000), which marked a 4% increase with respect to end 2017. It has to be remembered that in larger cities around 70% of residential property purchases was financed by cash. The surge in mortgage lending can be explained by the phasing-out of the government backed “Flat for Youth” plan in January 2018, which encouraged potential buyers to take out mortgage loans. Similarly, in Hungary, the volume of newly issued mortgage loans grew by 40% in HUF terms (28% in EUR terms) in 2017 with respect to the previous year and in Q1 2018 the growth was of 17% in HUF terms (15% in EUR terms) y-o-y. In the Czech Republic, the mortgage market confirmed sizeable cooling that started in mid-2017 after the Czech national Bank’s tighter limits on LTV started to bite and, at the same time, frontloading to escape these limits ended.

[1] In Q1 2018 the sample for the Quarterly Review included BE, CZ, DE, DK, ES, FI, FR, HU, IE, IT, NL, PL, PT, RO, SE and UK. (i.e. around 95% of the total outstanding mortgage lending in the EU28 in 2016).

In general, the interventions aim to counterbalance the pace of mortgage lending expansion by using either LTV or DTI caps, or by steering prospective mortgage holders to more fixed rate mortgage loans. In parallel, they try to support certain categories of prospective buyers to set their first foot on the housing ladder.

In Portugal, in order to counterbalance less restrictive lending criteria of issuers due to fiercer market competition fuelled by increasing demand for mortgage financing, the Central Bank has issued macroprudential measures which will enter into force on 1 July 2018 and which introduce caps in LTV, DTI and the original maturity of the loans, which have to be observed simultaneously. The measure is adopted as a Recommendation based on the “comply or explain” principle.

In the Scandinavian countries, stricter lending and amortising rules are being discussed or have been implemented in Q1 2018. In Sweden, a new regulation which suggests stricter amortisation requirements on housing loans for households with a high loan-to-income (LTI) ratio entered into force on 1 March 2018. The new requirements imply that new borrowers whose LTI exceeds 450% must amortise an additional 1% to prior amortisation requirements, which required an amortisation for loans with an LTV above 50%, a minimum 1% annual amortisation for loans with an LTV between 50% and 70%, and a minimum of 2% annual amortisation for loans with an LTV above 70%. In Finland, there are ongoing discussions to address household indebtedness. At its meeting on 19 March 2018, the Finnish FSA decided to lower the housing loan cap to 85% (from 90%), leaving the one of FTBs untouched at 95%. This decision will enter into force on 1 July 2018 and is expected to have a mild overall effect. In Denmark, on 1 January 2018 a tightening of existing consumer protection legislation entered into force. The stricter requirements are a direct consequence of recommendations from the Danish Financial Stability Board stating that households with large loan exposures should be limited to loans with longer rate fixation, combined with an amortisation requirement. Households having a DTI of more than 400% will be limited to safer mortgage products including an amortisation requirement and a fixed or longer-term rate fixation. It is expected that the new legislation will dampen the overall demand for mortgage loans and that the existing market will move towards fixed rates, and amortisation will be consolidated by the new rules.

A similar approach to Denmark has been chosen by Hungary, where the National Bank (NBH) has introduced two new monetary instruments. Firstly, it concludes long-term interest rate swap transactions with partner commercial banks for 5 and 10 year maturities at regular tenders, and secondly, it also started to buy fixed rate mortgage bonds at preferential rates. In this way, with the participation in the bond purchase programme, the NBH helps banks to issue more fixed rate mortgage loans at better rates. A third regulatory instrument was announced by the NBH in June which addresses the monthly maximum DTI figures. The new rule sets a maximum of 25% DTI for variable rate mortgages, 35% for mortgages with a 5-10 year initial fixation period and an unchanged maximum 50% DTI for mortgages with a fixed interest rate or with a fixation period of more than 10 years. This new standard will be applied only to mortgages with maturities of more than five years and is expected to enter into force next October. In Poland, the end of the government-backed programme “Flat for Youth” was phased out in Q1 2018 and a new, upcoming support schemes will focus more on rental market.

In Ireland, the Central Bank revised its macroprudential mortgage measures at the beginning of 2018. The proportion of loans permitted to exceed the LTI threshold was changed for FTBs and second and subsequent home buyers. The Central Bank of Ireland also prescribed how lenders should assess the value of collateral for purchase-to-renovate mortgages. In the UK, there have been no new interventions in the first quarter of 2018. However, the effect of phased removal of tax relief for BTL mortgage interest has yet to fully work through. This contributed to very weak BTL purchase numbers. As a result, BTL, which has been a key driver of growth in the mortgage book in recent years, is currently making only a negligible contribution to net lending.

In Belgium, additional macroprudential measures entered into force from 30 April 2018 to limit the risks of residential real estate as identified by the National Bank of Belgium. It applies to loans granted to retail clients of banks using an internal model based (IRB) approach to calculate their capital requirements. This measure is applied at portfolio level and consists of two components: the first is a linear increase of 5 pps of the risk weight on the IRB model outcome, while the second is applied on the average risk of each bank’s portfolio. Moreover, from 1 June 2018, the registration duty in Flanders decreased from 10% to 7%, and even 6% below a certain threshold of housing price (EUR 220,000 in the larger cities and in some cities around Brussels, EUR 200,000 elsewhere). This latter rule might have skewed the acquisition of real estate for the upcoming months.

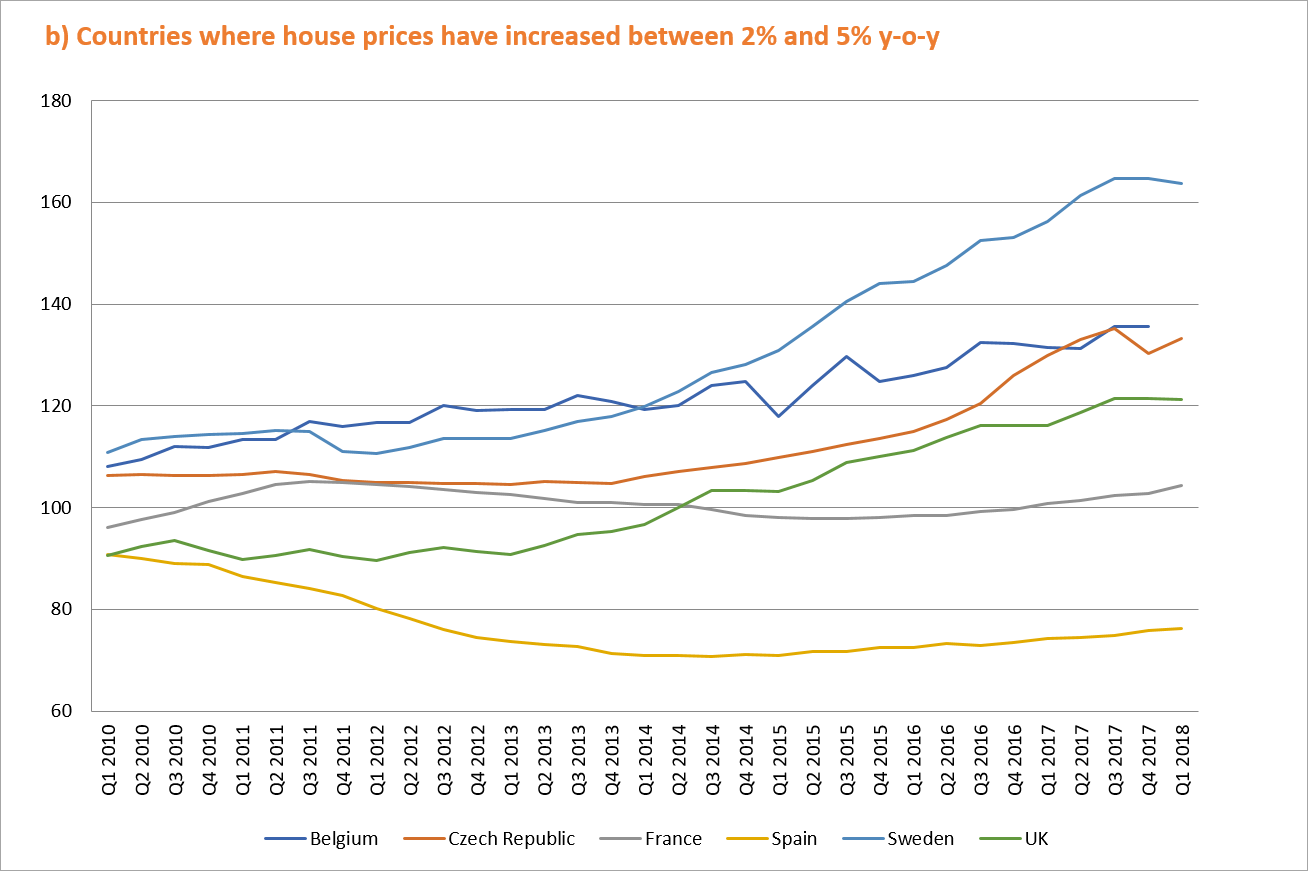

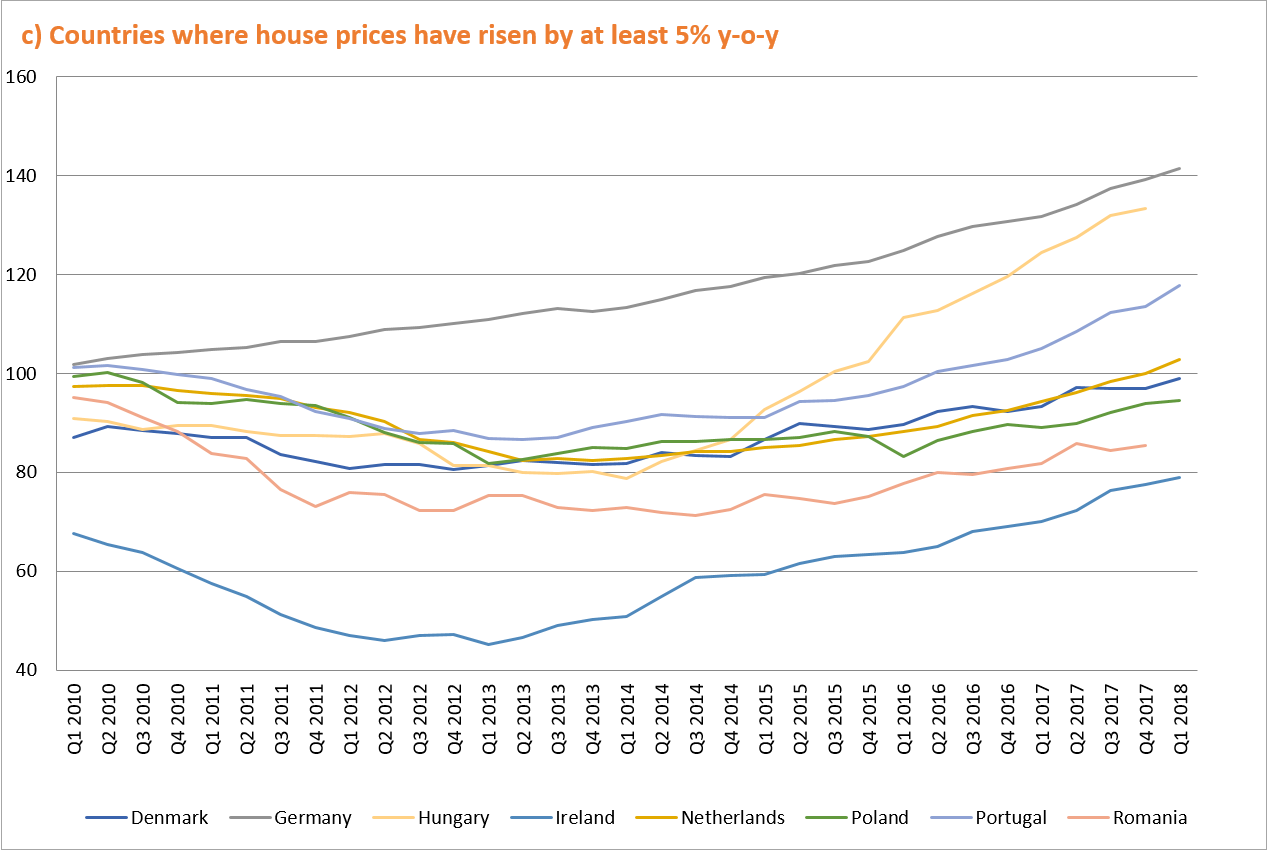

As a general trend, house prices continued to increase with some notable exceptions. The main underlying supply and demand imbalances are still in place, although shifts can be spotted here and there. The majority of the countries of our sample in Q1 2018 saw house price growth of more than 5% y-o-y, with three greater than 10% y-o-y, while only two were below 2% y-o-y. Looking at the price evolution with respect to the previous quarter, countries well-known for their significant price increases have shown a trend inversion.

The country with the highest y-o-y house price increase in Q1 2018 was Ireland at 12.7%. The Residential Property Price Index level reached is the highest since March 2009. The national annual rate of increase has accelerated in each of the past seven quarters. In Dublin, residential property prices increased by 12.1% in the year to December, whereas prices in the rest of the country rose by 13.4%. This was the twelfth consecutive quarter in which prices outside Dublin rose faster than prices in the city. The housing market statistics on completions and commencement increased by 26.7% and by 13.3% respectively, but both are still well below the levels needed to meet demand. The number of residential properties sold increased by 2% y-o-y to about 9,800 in Q1 2018, according to the Central Statistics Office (CSO). Some 16% of residential property bought at market prices was sold to non-household buyers. About 19% of properties sold in the quarter were new properties. Hungary closely follows with growth of 11.5% y-o-y and 1.2% q-o-q. Construction statistics also show an expanding market, with a 3% increase in building permits issued and 60% more buildings completed in Q1 2018 with respect to Q1 2017. Portugal closes the podium with 10.5% y-o-y, which can be explained by a shortage of supply of both units for sale and for rent. This remains a challenge throughout the regions and goes hand in hand with an increase in the number of sales. In the rental and sales market, the scarcity of new listings continues to push prices up and no relevant changes are expected.

In Central Europe, house prices continued their increasing path. In Germany, house prices increased by 7.4% y-o-y in Q1 2018, mostly due to the excess in demand for owner-occupied houses and condominiums, especially fuelled by the low interest rate environment. Although purchase prices are quite high, many market participants still consider home ownership to be a sound investment. Broken down by property type, prices for condominiums are 6.3% higher than in the first quarter one year ago, while those for single family houses are 7.8% more expensive. In the Netherlands, house prices increased at a national level by 8.9% y-o-y in Q1 2018. An increased regionalisation can also be detected. The number of sales in cities is stabilising and in more rural areas the number of sales is growing, whereas house prices increase mostly in the larger cities. In Belgium, house prices on average contracted slightly in Q1 2018 with respect to the previous quarter. Regional differences can be spotted with Flanders and Wallonia contracting by 2% and 1.6% respectively, while the region around Brussels saw house prices increase by 2.9%. A different picture can be seen for apartments where, in Flanders, prices increased by 0.6%, while in Wallonia and Brussels, they contracted by 2% and 2.1% respectively.

In Scandinavia, house prices do not follow the same path in the various countries. In Denmark, prices are increasing across the country and market conditions are accommodative of further increases. In Finland, prices remained relatively stable with a 1.3% y-o-y increase in Q1 2018, with the region around Helsinki increasing by 2.1% while elsewhere there has been a 1.9% contraction. In Sweden, there has been a shift in the housing market since end 2017, which was already anticipated in Stockholm. Price increases have cooled-off considerably with apartment prices contracting by 7% y-o-y in April 2018, while prices for one-family homes increased by 4.6% y-o-y in Q1 2018 with respect to a 7.6% increase in the previous quarter. Since October 2017, there has been a quick shift in the price development and the expectation of future price increases. Lending figures have still not reacted to this change in dynamic. Construction figures increased in 2017 and are expected to follow the same path in 2018, thus reaching the former record level from the 1990s. However, a shortage of supply is still felt in every city of the country. It is noteworthy to point out that several newly-built apartment blocks are proving hard to sell due to their too steep price tag, which is simply not affordable to many people in Sweden. Several reports have highlighted this problem and housing constructors plan to reduce the pace of new construction.

In the UK, while overall price inflation remains in positive though decelerating territory, the housing market in London, which is often a lead indicator of wider UK housing trends, has hovered just above zero price growth since Q1 and dipped briefly into negative territory in February. The central scenario remains one of low single figure growth, but there is a material risk that house prices could see a modest decline, especially if there are further negative shocks to the housing market or wider economy.

In Romania, house prices continue to follow an upwards trend of around 5.6% y-o-y in Q1 2018 and in Poland too prices continue to grow at a national level by on average 6.2% y-o-y. Both primary and secondary markets depict an increase with smaller figures in Warsaw than with respect to other large cities such as Gdansk, Bydgoszcz, Katowice and Lodz. Spain also saw an overall house price increase of 2.7% y-o-y, but contrary to the case in Poland, in the capital city, Madrid, prices grew by 8% – more than most other regions and cities, such as the Balearic Islands with 7% or Barcelona with 5.3%.

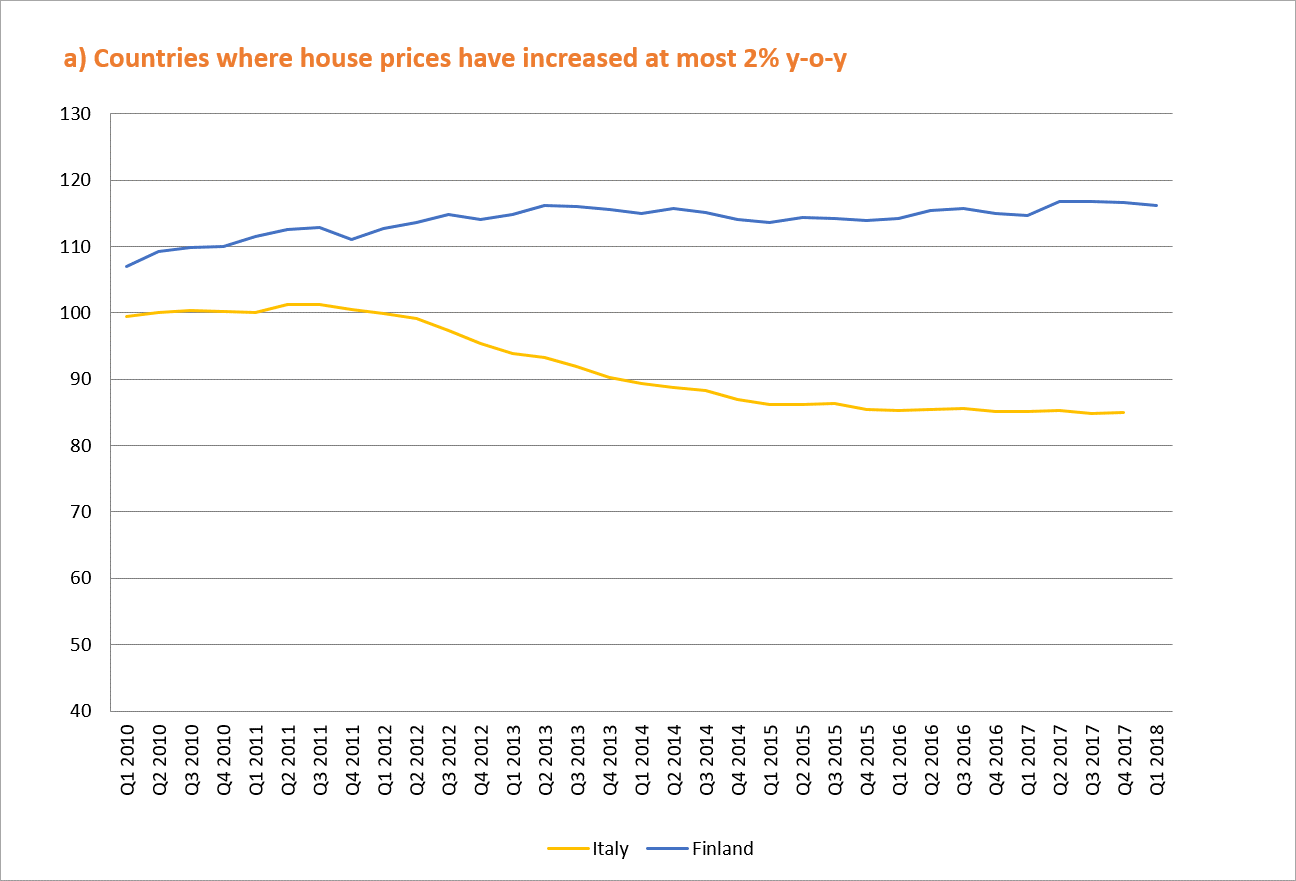

In France, house price increases were at around 3.5% y-o-y in Q1 2018, with the existing home market depicting a slightly larger price increase with respect to new homes, where the market contracted by 8.3% y-o-y in Q1 2018. This dynamic is expected to continue in the upcoming months due to the phasing-out of a housing assistance programme in favour of new-build homes. After the peak observed in sales figures in 2017, in Q1 2018 sales of existing homes fell slightly. Both building permits and housing starts increased by 3% and 9.3% y-o-y respectively. Developers’ sales figures decreased by 1.2% y-o-y in Q1 2018, while individual house builders saw an 8% increase over the same period, but the curve could be reversed in 2018. In Italy, at end 2017, the last available figures, house prices showed the first marginal q-o-q increase since Q3 2016 with new dwelling prices growing by 0.7% q-o-q, while y-o-y there was a slight contraction of 0.5%.

Overall, in Europe the decline in mortgage interest rates seems to have reached a halt and nearly half of jurisdictions in our sample have seen increases in the average mortgage interest rate, thus slightly increasing the average interest rate in our sample by 0.1 pps to 2.3% with respect to end 2017. It is also interesting to note that the dispersion of the various interest rates continued its upward path started in Q2 2016 and reached the levels of Q1 2015. Bearing in mind the different structure of mortgage market breakdown in the various countries, another overall trend noticed in half of the sample is an increase of the initial fixation period in new mortgage lending deals, primarily in order to benefit from the still extremely low interest rate environment.

In Scandinavia, mortgages depict some of the most accommodative interest rates, with both Denmark and Finland offering mortgages for less than 1%, with the latter reaching an historic low at 0.92%. Moreover, in Denmark long-term mortgage rates scaled up in the early part of Q1 2018, but since then have returned to the level observed during the latter part of 2017. Similarly in Sweden, longer initial fixed interest rates increased to slightly less than 30% of new mortgages in Q1 2018.

In the UK, interest rates remain at attractive levels, despite the rate rise of the Bank of England in November 2017 and the prospect of a further hike in the coming months. This has supported the strong re-mortgage numbers and will continue to provide further incentive for re-mortgage activity in the coming months. Furthermore, over the past year longer-term fixed rates (fixed for 5 years or more) became more popular among mortgage holders, which was helped by the widespread availability of longer-term fixed rate deals at historically attractive rates. In Ireland, variable rate mortgages accounted for 46% of new mortgages issued in Q1 2018 and 46% of outstanding mortgages, excluding securitised loans, were on ECB base rate-linked tracker mortgage rates in Q1 2018.

In Southern Europe, for Portugal and Italy interest rates continued their downwards path with more mortgages having a longer initial fixation period. In Portugal, variable rates benefitted from a historic low Euribor and reached 1.51% in Q1 2018. For Italy, short-term interest rate loans are available at 1.54%, while those with an initial fixation period of 1 year or more decreased by 0.05 pps to 2.07%. There is a slightly different picture in Spain, where the weighted average interest rate slightly increased by 0.03 pps to 1.60%, but here too the shift to a more fixed rate environment continues, reaching 62.6% of new lending in Q1 2018.

France saw a slight increase in its average interest rate by 0.09 pps to 1.55% in Q1 2018, an increase which in real terms is carved out by the relative inflation increase. In the Netherlands, notwithstanding the ongoing interest rate decrease, researchers are looking for the impact of a future interest rate increase. They conclude that the expected economic growth and income increase will compensate for the negative effect of rising interest rates. In Belgium, interest rates are continuing their downward path. It is interesting to note that the share of new loans with initial fixed rate periods for 1 year amounted to almost 5%, double the share of Q1 2017. Since 2015, the number of overdue contracts shows a positive evolution with non-regularised defaults reaching 1% from the long-term share of 1.1%. In Germany, the average interest rate has slightly increased by 0.02 pps to 1.85%. Nevertheless, here too more new mortgages have a longer initial fixation period.

In Hungary, variable rates linked to the three month BUBOR (Budapest Interbank rate) are no longer the most popular instrument among borrowers. As elsewhere, loans with longer fixed interest periods are becoming more popular. A similar picture is visible in Romania, where the increase in the representative mortgage interest rate to 4.78% has decreased the appetite for more variable mortgage rates and increased the share of fixed rates, especially the 10y plus fixation period, which jumped from 0.5% to 5.3% of new loans in just one year. Finally, in Poland, where all mortgages are granted at a variable rate, no particular changes are seen on the horizon, even though the inflationary pressure continues to grow. In the Czech Republic ,interest rates grew slower than the relevant reference market rates.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.