27 September 2018

Introduction

In this second quarter of the year, the economic momentum in the European Union continued with positive GDP growth, falling unemployment rates – which are now at pre-crisis levels or just slightly above them, and expanding private consumption. Following the same path, consumer inflation accelerated in the three months of Q2 2018 and a further increase is expected until the end of the year according to the European Commission’s forecast. Overall, the positive environment has favoured the housing and mortgage evolution. Nonetheless, different trends among countries are still observed.

In a nutshell, three main features characterised the evolution of the market in this second quarter. First of all, we observed the positive growth of gross lending in aggregate terms for the EU countries of our sample. Secondly, a slight increase in the average interest rate for the EU has been perceived along with a remarkable increase of its variance, a sign of the increasing differences amongst countries. And finally, house prices have started to cool-off or decelerate their growth.

1.1 Market development

The overview of the mortgage market in aggregate terms is the same as in the previous quarter. The value of outstanding mortgage loans in our EU sample1 is over EUR 6.8 tn. and it has increased 2.4% year-on-year. Despite the continuing positive trend overall, a few countries have started to show downward trends in their mortgage markets.

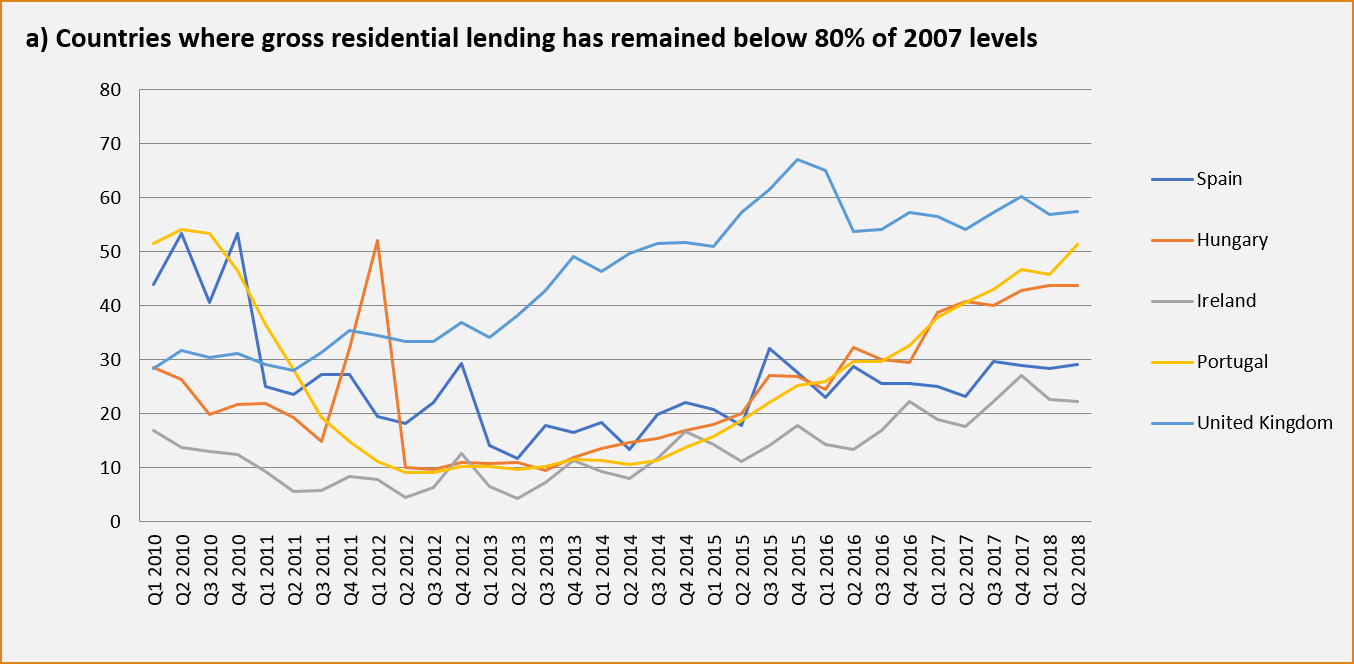

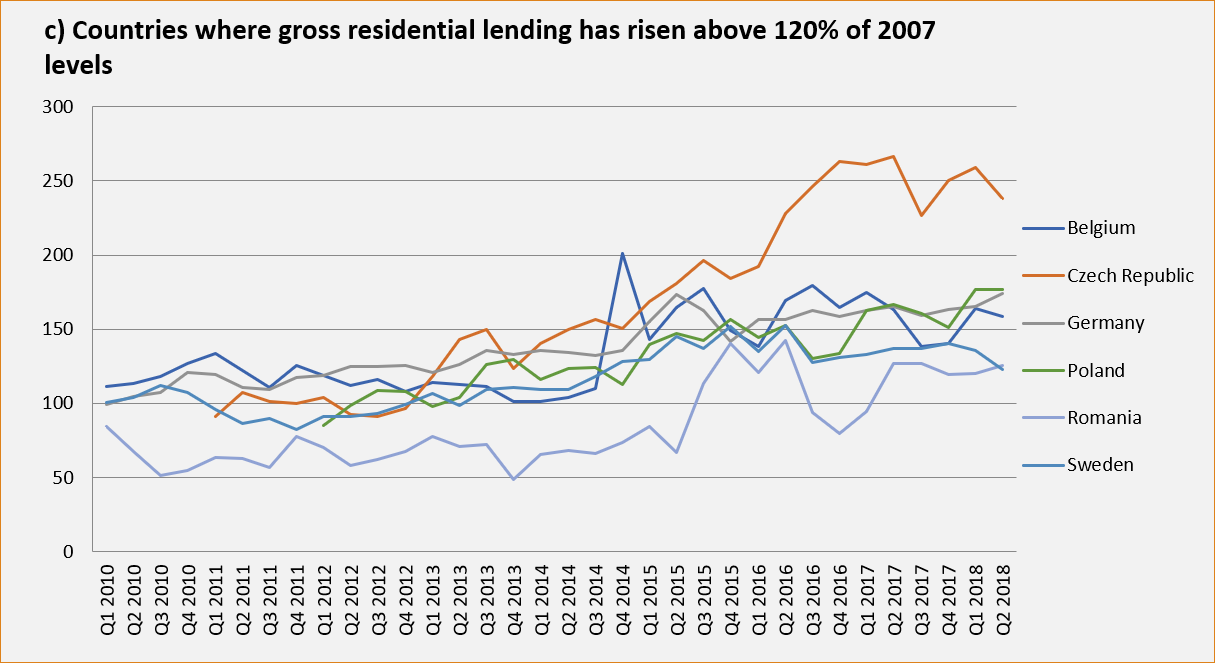

Whilst in the first quarter of 2018 there were four countries in which gross lending deviated from the general positive trend and saw their y-o-y figures declining, in the second quarter there were five, namely Belgium, Italy, Denmark, the Czech Republic and Sweden.

Among the countries in South Europe, we can observe different trends. In Italy, the evolution of gross lending with respect to the same period last year continues to contract, but when looking at the figures from the second quarter compared with those from the first quarter a positive evolution is observed. Outstanding residential mortgages continued to grow to around EUR 376.6 bn. On the other hand, Spain has experienced an important increase in residential gross lending, which has grown by 18.4% y-o-y. Nevertheless, the outstanding residential loan amount has decreased in this last quarter by 2.5% y-o-y. For Spain, the main depressors of the market have been the deleveraging process and the suspension of foreclosure processes for vulnerable groups addressed in the Code of Good Practice. Despite this, credit performance continued to show clear signs of recovery. In Portugal, total outstanding residential loans decreased by 0.9% y-o-y, following a descending path since Q4 2011. Nevertheless, new loans continue to show a growing trend with an exceptional 18.4% increase in the Q2 reaching EUR 2.6 bn. The results of the June 2018 Portuguese Housing Market Survey showed growth in demand and sales, although at a slower pace, while forward looking activity indicators have eased in recent months.

Heading North and into Central Europe, we observe that Belgium continues to be an exception to the positive trend followed by most of the European countries. As in the previous quarter, a contraction continues with a decrease in the number of credits granted compared to the last year, which was noticeable on almost all levels. The number of refinancing loans also went down by about 22% y-o-y. If refinancing deals are excluded, mortgage credit contracts were granted for a total amount of almost EUR 8.3 bn. Despite this downward move in the number of contracts granted, refinancing operations excluded, in the second quarter of the year, the amount of mortgage credit granted reached an all-time high level.

In the East, the Czech Republic and Hungary differ in terms of the evolution of the gross lending figures. The former left the path of growth and experienced an important mortgage market decrease of 7.4% y-o-y, which was in many ways expected considering growing interest rates, the tightening of rules for granting loans for housing and the low real estate offer. In Hungary, the total outstanding loans for residential mortgage lending was diminished by 3.8% y-o-y and by 0.6% with respect to the previous quarter; however, gross lending

increased on quarterly terms. Romania was another of the countries with an increase in its mortgage market. Mortgage credit grew at a faster pace compared to the previous quarter with 3% growth q-o-q. New mortgage loans were almost entirely granted in local currency.

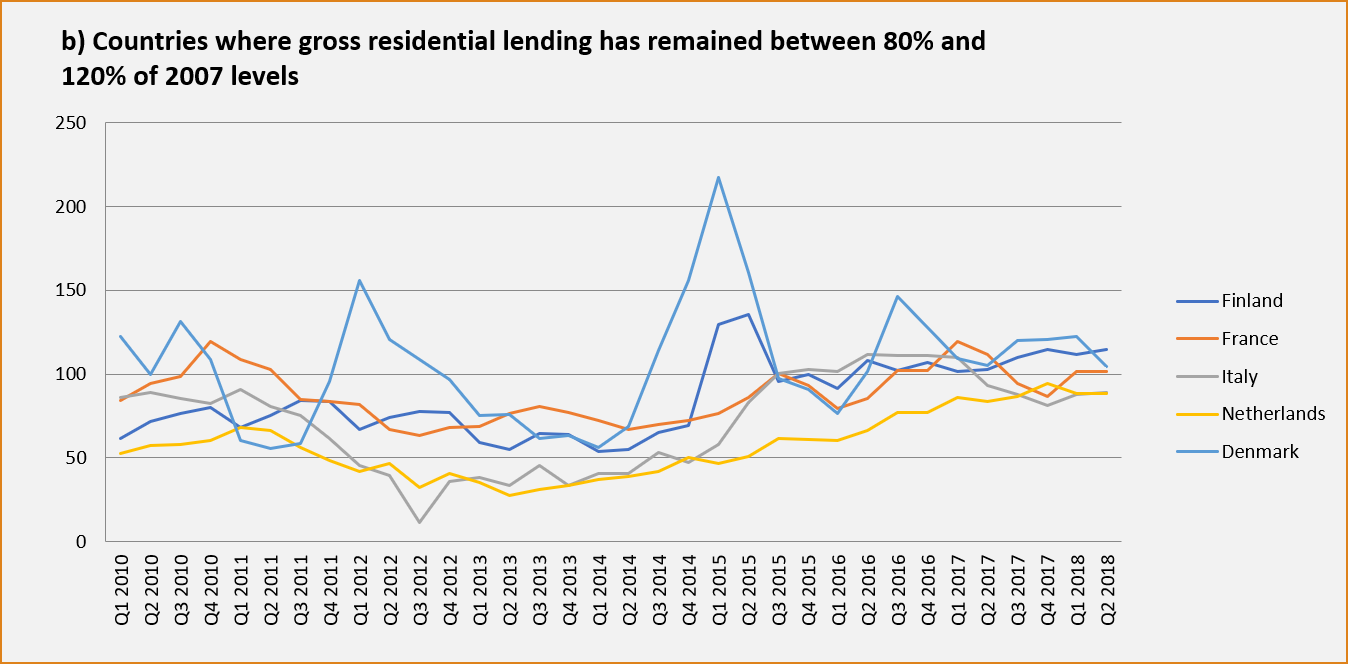

In the Scandinavian countries a mixed picture is noticed with regards to the pace of mortgage market dynamics. In Denmark, total outstanding residential mortgage loans increased at a moderate quarterly pace of 0.7%. Sweden follows the same path with a modest increase of 0.9% compared to Q1 2018. In Sweden, net mortgage lending growth is stable at around 7% for two years now, but it has started to slow down. This can be explained in part by the fall in housing prices which started in autumn 2017. The expectation is that construction figures in 2018 will be lower than in 2017, which almost reached the record level of 1990. There is still a relative lack of supply of dwellings, especially in larger cities. However, the high selling prices leave newly built dwellings hard to sell, thus slowing down the construction pace in the next quarters. In Finland, the growth in gross residential mortgage lending was more significant, growing by 12.4%, thereby becoming one of the countries with highest growth in our sample. The economic boom and improved employment environment, together with low interest rates, fuelled demand here.

In Ireland, mortgage approval volumes rose by 7.7% y-o-y in Q2 2018. This increase was mainly driven by mortgage switching, but purchase mortgage drawdowns rose by 9.2% y-o-y as well. New dwelling completions rose by 34.1% y-o-y in Q2 2018 to more than 4,400 units, with almost half of them in Dublin. Multi-unit housing schemes, rather than apartments or one-off houses, accounted for 62.5% in Q2 2018, up from 17.4% in Q2 2012. Despite these figures, supply is still far from meeting for the estimated demand.

In the UK, residential house purchase lending fell by 1.3% in Q2 compared to the same quarter of 2017. This is the second consecutive quarter of decline, which is driven by weak home mover numbers. House purchase activity in the buy-to-let (BTL) sector continues to fall y-o-y, with tax and regulatory measures reducing the returns on investment and raising the bar for mortgage affordability. However, re-mortgage activity continues to grow in both the residential and BTL sectors. The number of residential re-mortgages rose by 16% year-on-year in Q2 2018.

[1] In Q2 2018 the sample for the Quarterly Review included BE, CZ, DE, DK, ES, FI, FR, HU, IE, IT, NL, PL PT, RO, SE and UK. (i.e. over 95% of the total outstanding mortgage lending in the EU28 in 2017). For FR, HU, NL and PL the last available data provided in Q1 2018 has been used.

During the second quarter of 2018, there were no significant changes relating to regulation concerning the mortgage market in European countries. This being said, two countries proceeded to implement new measures domestically.

As announced in the previous Quarterly Review, the macroprudential measures adopted by Banco de Portugal have entered into force during this last quarter. These measures affect all credit institutions and financial companies which have their head office or a branch in Portugal. They establish three types of limits: a cap on the ratio between the loan amount and the value of the property pledged as collateral; a cap of 50% on the ratio between the monthly instalment amount calculated with all the borrower’s loans and his/her income with some exceptions; and finally, a cap on the original maturity of the loans. The limits applying to the LTV and DSTI ratios, and to the maturity must all be observed simultaneously. Also, it is important to highlight that the measure is adopted as a Recommendation.

The Czech Republic is the other country introducing important changes to its regulation. Here, the Recommendation on the management of risks associated with the provision of retail loans secured by residential real estate was updated. The new Recommendation is focused mainly on confirming existing rules of LTV limits and newly defined maximum values of income indicators that have to be fulfilled by customers. The limits must be applied when granting all housing loans secured by real estate and non-purpose consumer loans granted to customers already having mortgage loans as of 1 October 2018.

This modification is expected to have a significant impact on production, with a 10-20% drop in sales expected across the market. On the other hand, there is not expected to be any impact on the Real Estate market, where the demand for housing will still exceed the offer of real estate.

In addition to these two new announcements, some effects from previously announced measures are also worthy of mention.

In Spain, the active policy of divestment of Non-Performing Loans (NPLs) and Real Estate Owned (REOs) properties implemented by financial entities to foreign investors continued its acceleration. Moreover, Spanish financial institutions have improved their profitability fuelled by both lower loan loss provisions and reduced expenses’ based on the branch network reduction strategy. For future quarters, the Bill regulating real estate credit contracts is expected to be approved by the Spanish parliament.

The UK has continued to suffer the negative impact on new business due to the removal of tax relief for BTL mortgage interest. The Irish market has continued with the adaptation to the macroprudential mortgage measures introduced by the Central Bank of Ireland from 1 January 2018.

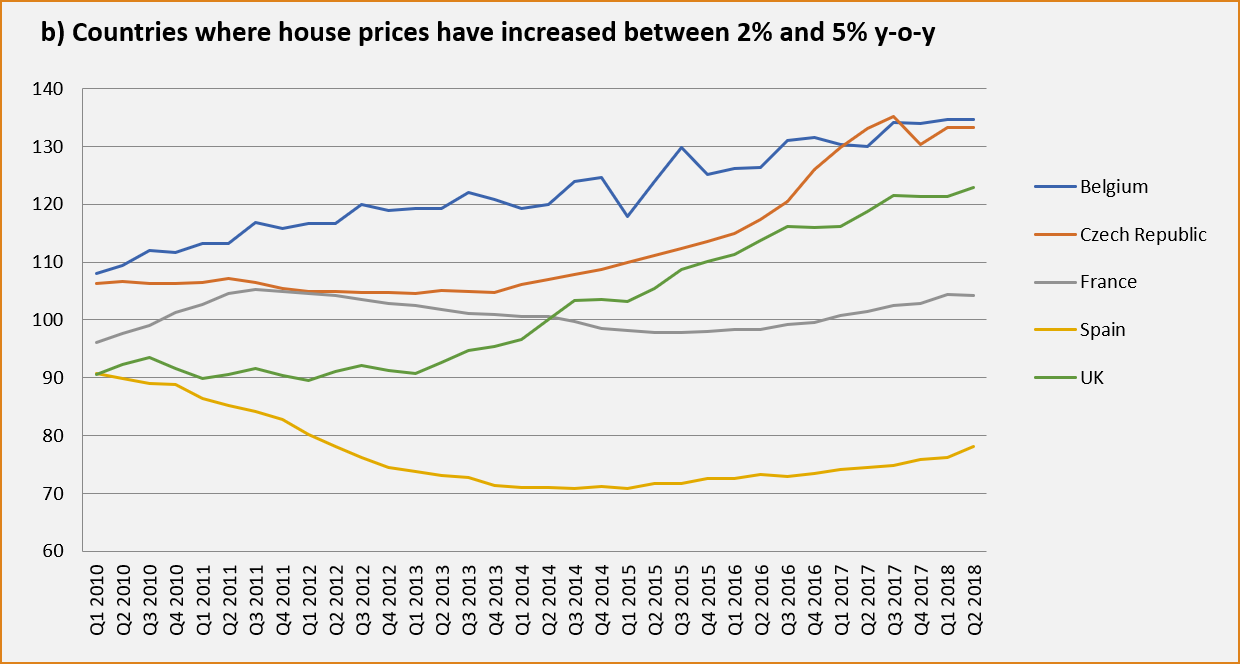

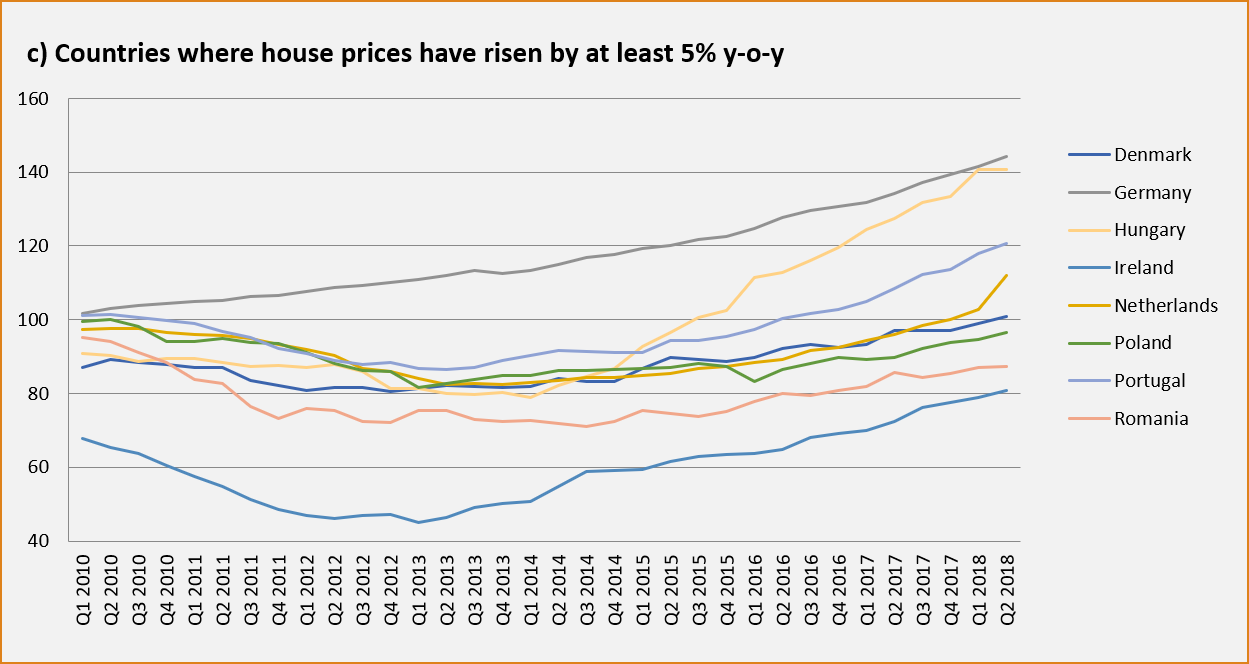

As was the case in the previous quarter, house prices continued to increase in almost all European countries of our sample in Q2 2018. However, we can identify some significant exceptions since supply and demand are still not completely balanced.

Ireland remains the country witnessing the highest growth in house price increase. The country has experienced a 11.9% increase on house prices in Q2, which is slightly less than the quarter before and the first slowdown in price rises since June 2016. Prices in Dublin rose by 9% y-o-y, the lowest rate of increase since March 2017. Prices outside the capital rose by 15.2%, the joint-fastest growth rate since the series begin in 2005. This was the 13th consecutive quarter in which prices outside Dublin have risen faster than prices in Dublin. Ireland was closely followed by Portugal which experienced a 11.24% y-o-y rise. In Portugal too this growth rate is lower than the previous quarter. In Central Europe house prices continued to follow the positive trend of past quarters. In Germany, once again residential properties were in very high demand and, as a consequence, prices increased by 7.5% compared with the second quarter of 2017. In Belgium, the average price of a house went up by 4.1% compared to the average price in the first quarter, reaching EUR 250,735. In the first quarter of 2018 price differences among the three regions of the country were observed; however, in this quarter house prices went up in all of them. In Flanders, average house prices went up by 3.7% (to EUR 276,393), followed by Wallonia with a 4.1% increase (to EUR 189,484) and finally, by Brussels, with a rise of 1.6% (to EUR 450,906).

Moving to the East, in the Czech Republic, the trend for house prices has not changed compared to the first quarter of the year. Prices grew for both new housing projects and for existing real estate, exceeding the dynamics of income growth. This trend is also expected to remain in the following months of the year. In Romania, house prices continued to follow an upwards trend in line with the assessments made in the previous quarter, despite the fact that final figures are not available at this stage.

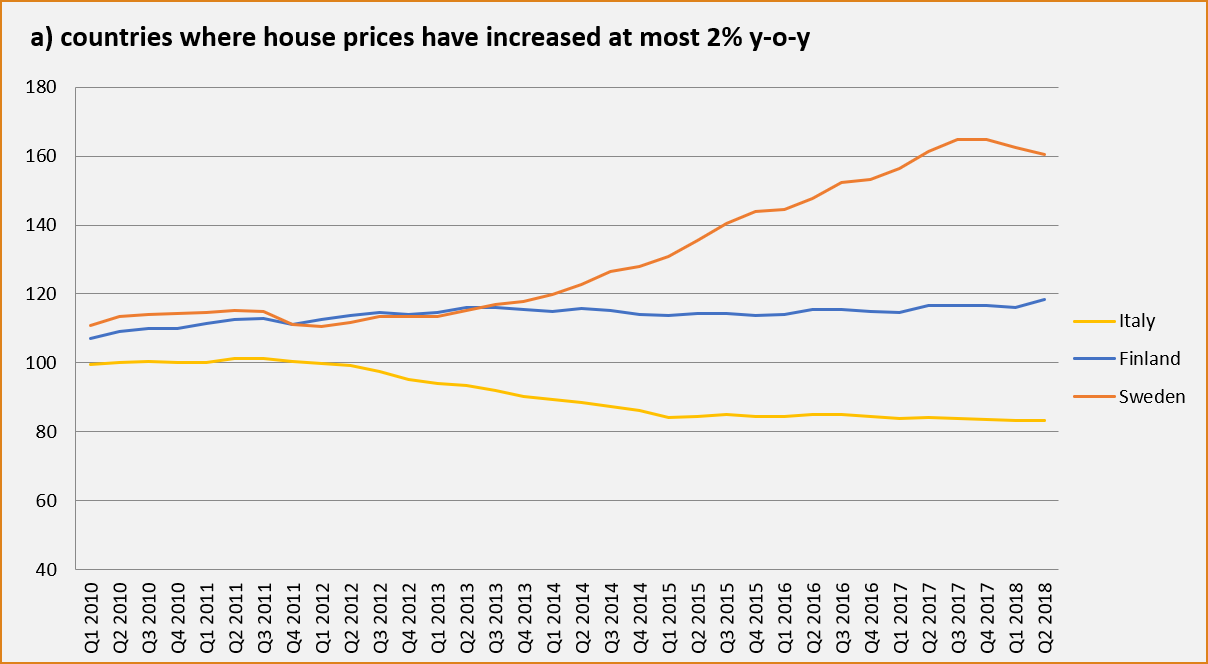

In Scandinavia, countries followed different paths. Denmark experienced stable development throughout the country. House prices rose by 4% compared to the previous year, an increase mainly due to the accommodative conditions that have characterised the country over recent years. In Finland, house prices rose moderately by 1.3% compared to Q2 2017. This moderate growth was due to the strong supply in the national housing market that keeps prices under control. Finally, Sweden followed an opposite trend. House prices have cooled off considerably, especially in Stockholm. Apartment prices in Sweden have fallen by 6.7% on an annual basis.

In the South of Europe, Spanish house prices increased by 5% compared to Q2 2017. On the other hand, in Italy, house price inflation continued on a downward, though decelerating trend. Prices of new dwellings decreased by 1.3% compared to the previous quarter.

Finally, the UK’s house price inflation continues to decrease, but remains positive at a national level. In London, prices have been falling faster than elsewhere in the UK and dipped into modestly negative territory in Q2, when they went down by 0.2% y-o-y. The London housing market often leads the rest of the country and it is therefore possible that we could see price falls spread across the country during the next few quarters if the current trend continues.

Overall, mortgage interest rates remain at historically low levels due to the competitive supply that characterises the market along with the ECB’s monetary policy. However, as started a few quarters ago, the weighted average interest rates of some European countries continue experiencing moderate rises in Q2 2018.

This is the case of Spain where, despite interest rates remaining at low levels, the weighted average interest rate this quarter has shown the first marginal increase in a y-o-y basis since Q1 2014 having risen by 1 percentage point y-o-y. The still low interest rate environment confirmed the observed preference for fixed rates as a solution for consumers’ risk aversion.

Continuing with the South of Europe, Portugal and Italy have kept the same trend as at the beginning of the year with an ongoing decline. In Italy, the interest rate on short-term loans fell to 1.4%, from 1.5% in the end of the previous quarter, and interest rates with maturity over one year also decreased from the previous quarter. Overall, the average rate on new transactions for house purchases reached a new record low of 1.79%. Portugal is also experiencing historically low interest rates and ended the second quarter with an average interest rate of 1.41% for new loans. These low rates have contributed to the increase of new gross residential lending and to the reduction of household debt. Furthermore, an increase in loans with a fixed interest rate to avoid an interest rate rise has been noticed.

Scandinavian countries continue to have mortgage loans with some of the most accommodative interest rates. In both Denmark and Finland the interest rates remain very low. Indeed, the average interest rate decreased for both countries during the second quarter of the year reaching record low levels. The average interest rate for Finland in Q2 2018 was 0.87% and for Denmark it was 0.88%, positioning them as the countries with the cheapest mortgage loans in Europe. In Sweden, interest rates are a little higher than in the rest of the Nordic countries, but they also have slightly diminished during the quarter, reaching an average of 1.51%.

Ireland also confirmed the prevailing trend in interest rates. The weighted average mortgage interest rate has increased from 3.02% to 3.15% in the second quarter, increasing by more than 4% q-o-q. Across the Irish Sea the UK also experienced an increase in interest rates, with short-term fixed rates showing the largest increase. The weighted average interest rate for the UK reached 2.09%. The interest rate for short-term loans increased by 3.5% with respect to the last quarter, while that for medium-term loans remained unchanged at 2.63%.

Germany is another of the countries experiencing increasing mortgage interest rates. The average interest rate grew from 1.85% in Q1 2018 to 1.90% in Q2 2018. This increase was common to short-term, medium-term and long-term loans.

Moving to Central and Eastern Europe, the Czech Republic has experienced an increase in its average interest rate rising to 2.5%, which is almost 50 percentage points higher than a year ago, when the average interest rate was slightly above 2.0%. For long-term loans this trend is driven by the increase of the basic interest rates offered by the Czech National Bank at the very end of the quarter. A fuller picture of the effect of the monetary policy change is expected to be visible in Q3 2018.

The Romanian representative mortgage interest rate stood at 5%, increasing by 0.23 percentage points compared to the level from the previous quarter and by 1.7 percentage points compared to Q2 2017. Following the trend of the other European countries, in Romania the share of loans granted with a variable interest rate in total mortgage loans decreased significantly compared to the same period of the year before. On the other hand, the share of new mortgage loans granted with a fixed interest rate followed an upwards trend.

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.