26 April 2019

Key Takeaways |

|

|---|---|

|

|

Market conditions should remain favorable for covered bond issuance in new markets in 2019, backed by positive, albeit softening, global economic growth and a more dovish stance from the Federal Reserve and the European Central Bank.

A key development this year will be the finalization of the harmonized covered bond legislative framework proposed by the European Commission, European Parliament, and European Council, which Parliament is expected to vote on in early April. The legislative package provides a common definition of covered bonds, defines the product’s structural features, and clarifies the responsibilities for supervising the product. It also amends the Capital Requirements Regulation with the aim of strengthening the conditions for granting preferential capital treatment.

A harmonized framework should boost development of covered bonds in Europe by raising the standards for asset quality, disclosure, and supervision, particularly in some Central and Eastern European jurisdictions. At the same time, the European benchmark should encourage legislators and regulators in other regions to align their frameworks to the same standards.

In this report, we take a closer look at the key characteristics of emerging covered bond frameworks in new markets, focusing on regulation, as this theme is likely to dominate throughout 2019.

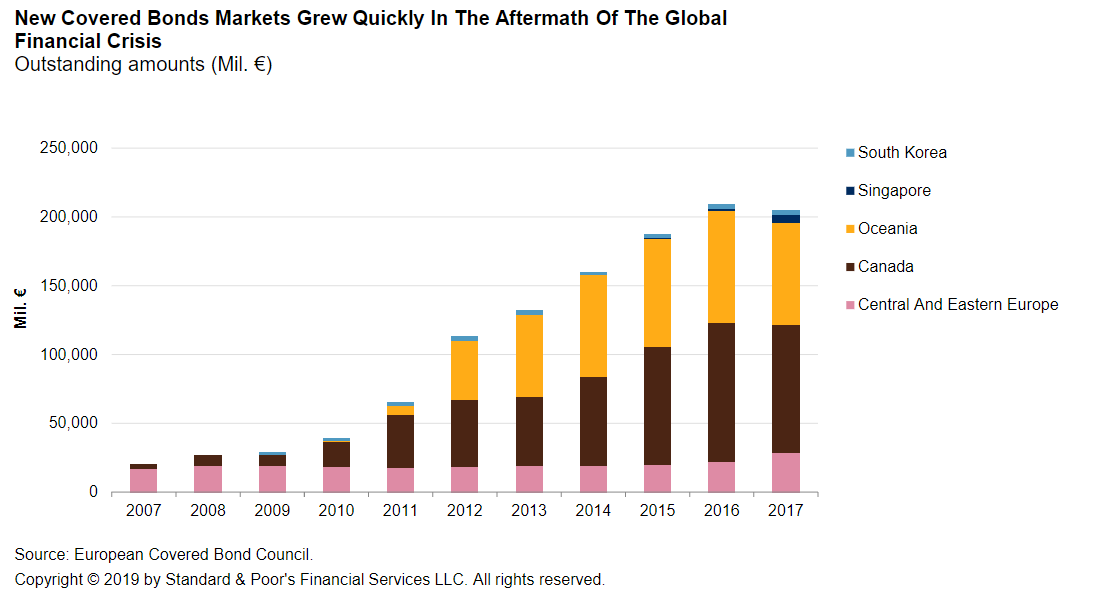

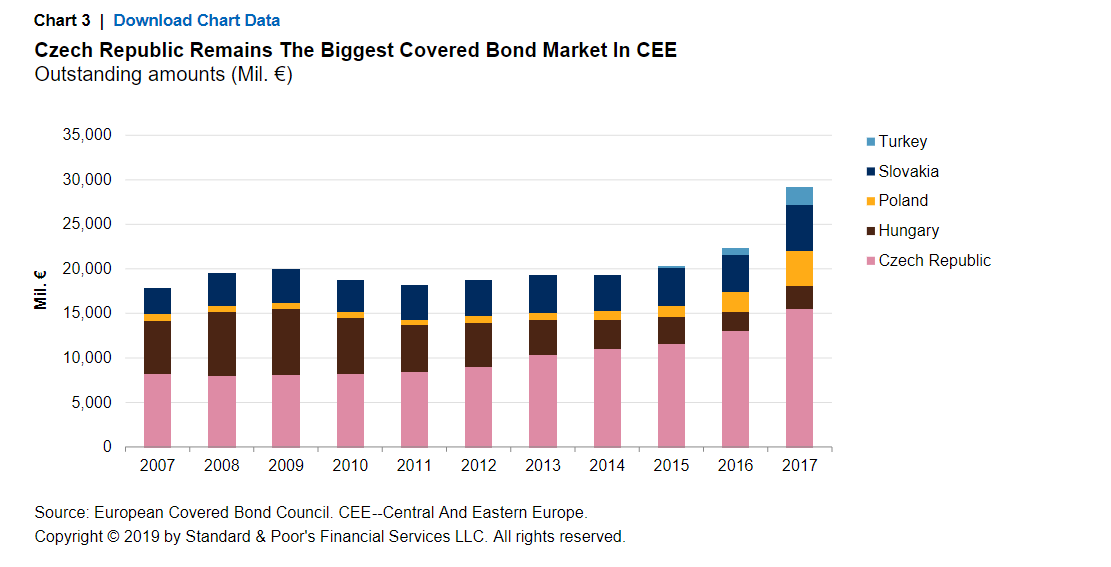

Covered bonds are expanding in Central and Eastern Europe, with increased volumes, notably in Poland, and improvements in some of the legislative frameworks. We expect this trend to continue in the near future, with new issuers accessing the market for the first time and further enhancements to some of the local frameworks.

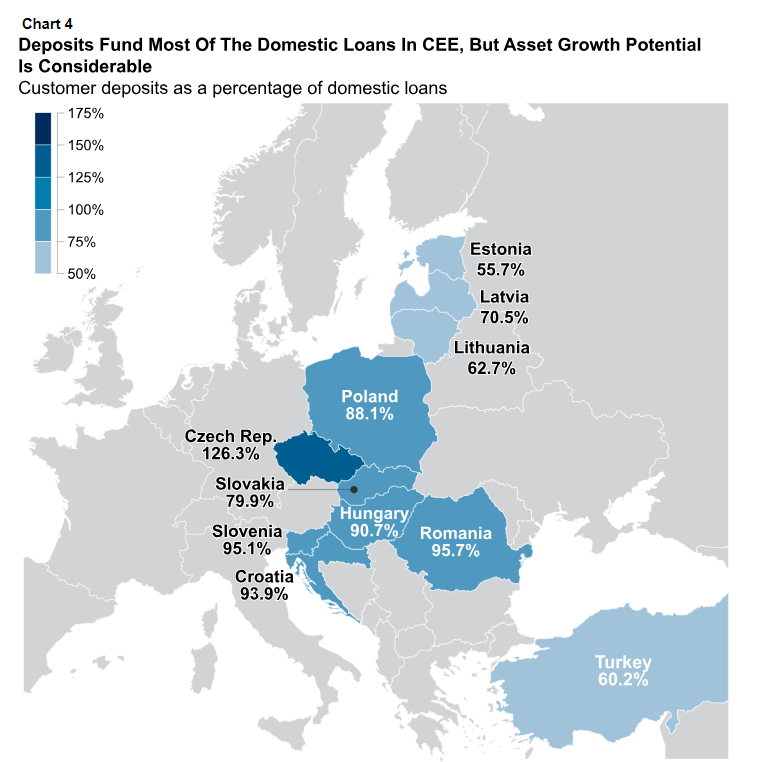

Issuers in the region have traditionally funded themselves with customer deposits. In a few countries, banks had been reliant on parent support from foreign banks to meet their funding needs. However, following changes in banks’ business structures and regulatory initiatives in recent years, banks primarily need to finance loan growth with domestic funding sources. At the same time, we expect solid growth in mortgage lending in the region. When mortgage lending growth outpaces customer deposits, lenders typically access the wholesale funding market and can use mortgage loans as collateral for issuing covered bonds.

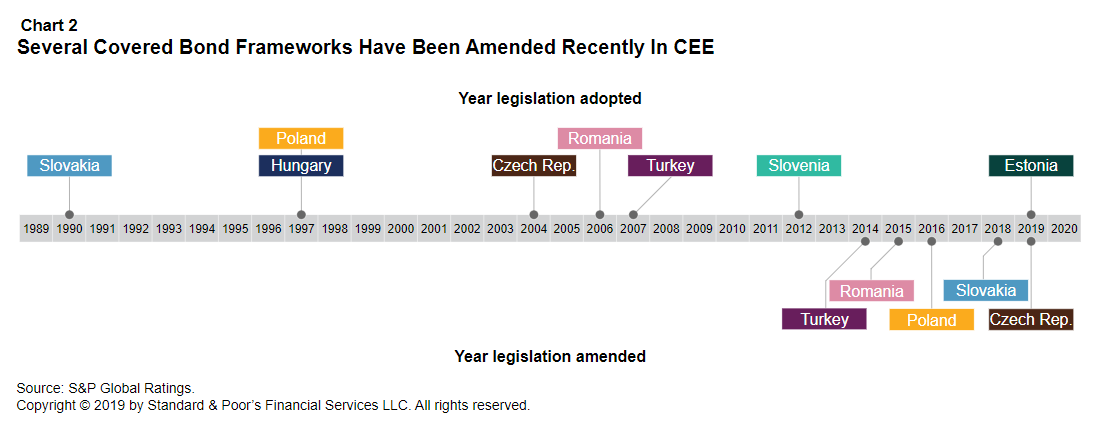

Several countries have also recently amended or approved covered bond legislation. The Slovak parliament has amended its existing framework to align it with the European Banking Authority’s (EBA) best practice recommendations. The new law became effective on Jan. 1, 2018, and we expect that it will spur the issuance of covered bonds in the country. Likewise, the Estonian parliament approved a covered bond legislation in February 2019, allowing local banks to issue covered bonds starting from October. Estonia is also working with Lithuania and Latvia to create a pan-Baltic legal framework for the issuance of covered bonds.

We expect the European Commission’s recent legislative initiative on European covered bond harmonization to further encourage local legislators to amend or approve frameworks aligned to best practices in established markets.

The Jan. 1, 2016, amendments to the covered bond framework address the main aspects that we assess in a covered bond’s legislation as part of our rating analysis (see “A First Look At How Poland Might Amend Its Covered Bond Framework,” published Nov. 13, 2014).

Customer deposits represent the main source of funding for domestic banks. However, some lenders have decided to issue covered bonds to reduce the structural mismatch between long-term mortgage assets and short-term liabilities. Moreover, some subsidiaries of Western European banking groups have historically relied on cross-border parental funding. As Polish banks are increasingly financing their operations themselves, we believe that covered bonds will become a more relevant alternative funding source for mortgage lenders.

Powszechna Kasa Oszczednosci Bank Polski S.A. sold its first euro-denominated benchmark covered bond notes in 2016 and remains the only Polish issuer to have sold euro benchmarks. It has also diversified its funding basis with a zloty-denominated covered bond issuance. In July 2016, mBank established a €3 billion international program and issued its inaugural euro-denominated covered bond in April 2018. We understand that other lenders, including local subsidiaries of foreign banks, are also setting up local mortgage banks to issue covered bonds.

On Jan. 4, 2019, an update to the Czech Republic’s Bonds Act (No. 190/2004 Coll., on Bonds; as amended by Act No. 307/2018 Coll.) became effective (see “S&P Global Ratings Comments On The Czech Republic’s Revised Covered Bond Framework,” published March 5, 2019).

The Czech banking sector is mainly funded through customer deposits, which provide a competitive and stable funding source for banks. As a result, Czech banks have limited incentive to diversify into more expensive funding sources such as longer-term debt issuance. However, within wholesale funding, mortgage bonds are dominating.

The Bonds Act amendment of August 2012 allowing Czech banks to issue mortgage bonds governed by a foreign law opened the market to foreign investors, and since then various Czech banks (including UniCredit Bank Czech Republic A.S. and Raiffeisenbank A.S.) have placed euro-denominated mortgage bonds with investors.

We believe that the Jan. 4, 2019, amendments to the Bonds Act, which addressed certain shortcomings of the previous legal framework, such as the automatic acceleration of the covered bonds following issuer bankruptcy, will further promote the relative attractiveness of the Czech covered bond market.

The issuance of mortgage covered bonds in Hungary is governed by Act No. XXX of 1997 on Mortgage Banks and Mortgage Bonds (Mortgage Bank Act). The Mortgage Bank Act addresses the main legal aspects that we assess when looking at covered bond legislation (see “Hungarian Mortgage Covered Bond Framework Allows For Rating Covered Bonds Higher Than The Issuer,” published Aug. 24, 2018).

In Hungary the largest portion of mortgage loans is deposit-funded, but covered bonds are increasingly used as a source of mortgage finance. After a slump following the 2008 crisis, the Hungarian mortgage bond market is recovering with increased issuances over the past two years. We attribute this to the mortgage funding adequacy ratio (MFAR) requirement introduced by the Central Bank of Hungary (Magyar Nemzeti Bank; MNB), which demands that banks finance at least 20% of outstanding household mortgage loans with mortgage-backed bonds, and the MNB’s mortgage bond purchase program introduced in 2017 until the end of 2018.

In addition, the credit quality of mortgage assets originated in the current credit cycle has improved because of tighter lending and underwriting standards, including loan-to-value and payment-to-income (PTI) caps. Contrary to pre-crisis mortgage loans, loans in the current credit cycle are almost exclusively in HUF with an increasing share having fixed rates and longer terms. The share of outstanding residential loans compared to GDP in Hungary is still relatively low compared to other European countries. Therefore there is further growth potential in residential mortgage lending and consequently mortgage bond issuance, both of which should be further supported by the Hungarian economy’s continued recovery (see “Hungary Ratings Raised To ‘BBB/A-2’ On Solid Growth And External Resilience; Outlook Stable,” published on Feb. 15, 2019).

To increase transparency from a rating perspective we have recently published a credit FAQ on how we analyze Hungarian covered bonds (see “How We Analyze Residential Mortgage Loans Backing Hungarian Covered Bonds” published on Feb. 20, 2019).

In September 2014, the Capital Markets Board of Turkey amended its covered bonds communiqué, paving the way for the first issuance of mortgage covered bonds in February 2015 (see “Standard & Poor’s Comments On Revised Turkish Covered Bond Framework,” published on May 20, 2015).

Turkey has generally low household and residential mortgage debt, and we expect to see sustained loan growth once the economy recovers from the recent slump. This will increase the pool of assets that issuers could use as collateral for covered bonds. However, market volatility and political uncertainty has slowed down the development of a covered bond market. Despite several Turkish banks establishing covered bond programs after the revision of the legal framework, so far only Turkiye Vakiflar Bankasi TAO (Vakifbank) has issued euro-denominated mortgage-backed covered bond benchmarks, in April 2016. In 2017, Vakifbank also placed the first Turkish lira-denominated covered bond away from development banks, which has opened the market for privately placed covered bonds in local currency. Other issuers have placed their issuances with supranationals and development agencies that can invest in bonds denominated in Turkish lira.

A revised law on mortgage bond issuance was approved at the end of 2015 and became effective on March 3, 2016 (see “New Romanian Law May Support Higher Ratings For Covered Bonds Than On Issuers,” published on Jan. 4, 2016).

Although no program has been established so far, we believe that local banks may try to issue in the domestic market, particularly if supranational institutions decide to support this product, and Alpha Bank Romania recently announced its intention to set up the first covered bond program in the country.

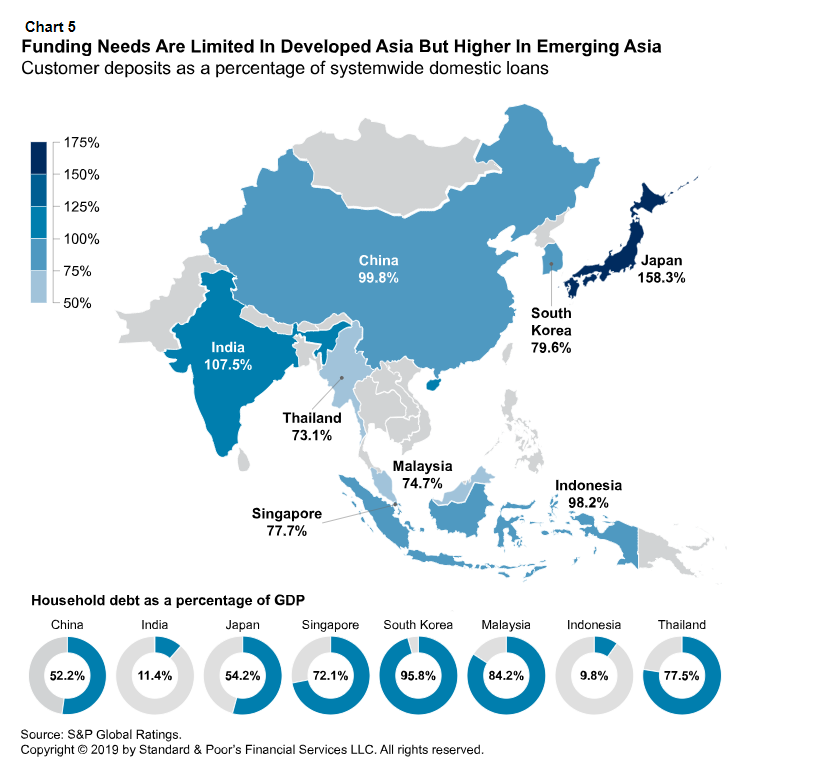

South Korea and Singapore pioneered covered bond issuance in Asia. As local banks have ample liquidity, their primary motivation in establishing covered bond capabilities was to have another risk management tool, rather than funding.

Other Asian countries could benefit from funding diversification through covered bonds. While issuers in certain countries will wait for the approval of a dedicated covered bond legal framework, we believe that in other jurisdictions covered bonds will be at least initially issued under a general-law framework with an appropriate supportive regulatory framework. For example, Sumimoto Mitsui Banking Corp. (SMBC) issued the first Japanese covered bond in November 2018. Because there is no dedicated covered bond legislation, SMBC based its program on a contractual structure. We believe that other lenders may follow suit due to the Japanese mortgage market’s size and local lenders’ funding needs in foreign currencies.

The regulatory framework for the issuance of covered bonds by banks incorporated in Singapore was established on Dec. 31, 2013, and refined on June 4, 2015, through the Monetary Authority of Singapore (MAS)’s Notice 648.

We believe the combination of Singapore’s regulatory framework, the country’s common law framework, and programs’ contractual documentation allows for effective isolation of the cover pool from the risk of an issuer’s insolvency (see “Singapore’s Covered Bond Framework Supports Higher Ratings On Covered Bonds Than on The Issuer,” published on Feb. 23, 2016).

With the legislative framework in place, the three major domestic banks have already set up their programs and issued cumulatively the equivalent of €8.46 billion as of the end of 2018. A few larger foreign banks are also considering the product, so more covered bond programs may be set up in the near future. However, the overall supply will likely be limited because banks in Singapore are mostly funded by depositors and because of the regulatory limit for cover pool assets that may amount to more than 4% of the issuer’s total assets.

Covered bonds in South Korea can be issued through the Covered Bond Act and the Korea Housing Finance Corp. Act. For South Korean banks, customer deposits remain the main funding source, and currently there are only two active covered bond issuers: Kookmin Bank and the Korean Housing Finance Corp., which last year issued the first social covered bond from Asia and the first Korean euro-denominated covered bond. However, the Korean Financial Services Commission has recently adopted a number of measures to encourage covered bond issuance, including reduced registration fees for bond issuances and lower capital requirements for covered bond investors. While such measures prove the regulatory support for the product, we nonetheless expect covered bond issuance from South Korean banks to be limited and opportunistic.

Issuers and regulators in Greater China have increased their interest in dual-recourse issuance in the past few years. Among the many market discussions and inquiries, some issuers have tried issuing instruments backed by loans or bonds. Structure-wise, these issues are similar to typical covered bonds. The bonds have fixed maturity dates, the issuers bear the repayment obligation, and some collateralized assets will provide a repayment source if the issuers cannot repay the bonds upon maturity. However, there could be differences in the selection of collateralized assets and the arrangement of covered assets’ segregation in these trials compared to covered bonds in other markets.

Larger banks in the Greater China area benefit from abundant liquidity and strong deposit bases. Therefore, the appetites and market trials for covered bonds issuance in this region mainly reflect increasing risk awareness–specifically, the importance of having alternative tools for banks to plan for rainy day funding, rather than current funding needs. Aside from limited issuers’ supply, the incumbent asset issue is another primary challenge for covered bond issuance in the region. All three markets in Greater China have regulations on the protection of depositholders, and the arrangement to ringfence specific banks’ assets to benefit covered bondholders could be complicated without a dedicated legal framework. Moreover, legally, depositholders enjoy a very high ranking in the allocation waterfall after banks’ liquidation in the region. Because these assets’ ringfencing and deposit ranking relate to the sovereign banking laws, regulators may find it difficult to have flexibility, even if they support the development of covered bond issuance. The so-called structured covered bonds that may achieve assets ringfencing and segregation, yet comply with all legislation, is an alternative option, but the market’s momentum will largely be limited by the higher operating cost of these structures. So while banks in this region are likely to investigate covered bond options, it would take regulatory and deal-arranging efforts to see issuance in the near future.

India has a significant shortage in affordable housing and a young and growing population. Moreover, household debt as a percentage of GDP is below that of other emerging markets. These factors suggest there could be significant growth in the housing finance sector in the future. Currently, customer deposits predominantly fund banks in India, but issuers and regulators are considering alternative sources of wholesale funding, including covered bonds. Similar to other Commonwealth countries such as Australia and the U.K., India does not have specific legislation governing securitization. Rather, the legal framework for India’s securitization market is based on existing trust, contract, and property law, and a series of guidelines issued by the Reserve Bank of India.

We anticipate that covered bonds in India may at least initially be issued under a general-law framework with an appropriate supportive regulatory framework. Structured covered bonds may be issued without European-style special covered bond legislation, but regulators’ guidance is likely to be needed. In our view, key clarifications required will include whether the issuance of covered bonds is permitted under Indian legislation generally, whether existing securitization guidelines can be applied to covered bonds, how asset segregation can be achieved, the treatment of assets in an issuer insolvency scenario, and whether there are any challenges from a tax perspective, including stamp duty and withholding tax (see “India’s Pathway To Establishing A Covered Bond Market,” published Sept. 12, 2017).

Covered bonds in this region have a short and limited track record. Panama was the first country to see a covered bond issuance in October 2012, now matured. Panama does not have a specific legal framework for covered bonds, and covered bonds are based on contractual agreements. Chile is the other only covered bond market in the region, with a limited and locally distributed covered bond issuance.

One factor preventing financial institutions in the region from issuing covered bonds is the lack of a dedicated legal framework. However, things may change thanks to the legislative developments in Brazil. If covered bonds prove successful there, we may see other countries in the region follow its lead.

In October 2014, Brazil enacted Provisional Measure No. 656, which outlined a framework for Brazilian local covered bonds (“letra imobiliária garantida”; LIGs), and which became Law No. 13,097 in January 2015 (see “A Closer Look At The Brazilian Covered Bond Framework,” published on Dec. 6, 2016). From the standpoint of the legal protection afforded to covered bondholders by the Brazilian framework in case of issuer insolvency, we believe the new regime could allow a covered bond program to be rated above the issuer credit rating under our covered bonds criteria.

Although Brazil’s National Congress passed a dedicated covered bond legislation in 2015 and related regulation was approved by the central bank in 2017, banks only began testing this new instrument after the 2018 presidential election, with private domestic placements. Santander was the first bank to issue LIGs in November 2018, followed by Banco Itau S.A., Bradesco, and Banco Inter.

We understand that the Brazilian Securities Exchange Commission is drafting regulations regarding public placements for LIGs, which will lead to the first public placement.

Moreover, we believe that banks are willing to issue cross-border covered bonds targeting dedicated European investors. However, the market is still waiting for legal and regulatory clarification on how these issuances could be done. Once this clarification is obtained, we believe that Brazilian banks will try to issue LIGs offshore targeting foreign investors (see “New Year, New Bank Debt Instrument: Brazil Welcomes Local Covered Bonds,” published on Jan. 22, 2019.)

Morocco was the first country in the region to release draft covered bond legislation (see “Morocco Looks To Covered Bonds To Support Housing Finance,” published on May 8, 2013). However, it has not yet approved the final law, which is a testament to the difficulties that can be encountered in the legislative process.

Similarly, in 2015, South African regulators considered allowing banks to issue covered bonds, in the context of a broader discussion regarding resolution regimes and the anticipated introduction of retail depositor guarantees. However, domestic investors remain resistant to the idea of covered bonds, due to their concerns about the potential pressure on the pricing of their senior unsecured debt, the losses if an issuer becomes insolvent, and what could happen to the ratings on this debt. As of today, banks are still not allowed to issue covered bonds, and we don’t expect any market development in South Africa in the near future.

For additional information on this report, please visit S&P Global Market Intelligence

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.