3 July 2018

The issuance of “green” covered bonds–backed by assets that are considered to have a positive environmental impact–grew strongly in the first half of 2018. As market activity increases, investors are inquiring more about green covered bonds and the nature and challenges of green finance. In this credit FAQ, we address questions we frequently receive on this topic, including what is driving green covered bond issuance, how our credit analysis could reflect green factors, and how we assess the environmental quality of financings through our Green Evaluation.

| Recent Green Covered Bond Issuance | |||

|---|---|---|---|

| Issuance date | Issuer | Maturity (years) | Size (bil.) |

| June 2018 | DNB | 7 | €1.5 |

| June 2018 | LBBW | 5 | €0.5 |

| May 2018 | Landshypotek | 5 | SEK5.25 |

| January 2018 | Sparbol | 7 | €1.0 |

| November 2017 | Deutsche Hypo | 6 | €0.5 |

| June 2017 | Berlin Hyp | 6 | €0.5 |

| SEK–Swedish krona. | |||

Despite the recent rise in issuance, there is still plenty of scope for growth. The volume of green covered bonds only represents a fraction of the broader covered bonds market. S&P Global Ratings expects that the proportion of green covered bonds could rise significantly as regulators push for greener finance and banks focus increasingly on underwriting the financing of green assets (see “A Look At Banks’ Green Bond Issuance Through The Lens Of Our Green Evaluation Tool,” published March 2, 2018).

In our view, the emergence of green covered bonds highlights the growing prominence of green finance in the traditional area of covered bonds and offers an alternative mechanism for banks to contribute to financing global climate commitments.

The increased interest in green lending in recent years, and the subsequent rise in green funding by banks, reflects three main factors:

How will these driving forces affect the issuance of green covered bonds?

Projects driven by political initiatives, such as the Energy Efficient Mortgages Initiative (EeMAP), all but guarantee increased growth in green covered bonds. EeMAP is a mortgage-financing mechanism that promotes the green tagging of mortgages, incentivizes building owners to improve their building efficiency or acquire new green properties at preferential interest rates, and collects data through a systematic framework.

Identifying the green credentials of existing assets and efforts to expand covered bond funding to new green asset classes will likely reshape the focus of loan underwriting. It will put more emphasis on green attributes and create further requirements for program documentation and public disclosure, while allowing issuers to attract new investors.

In turn, new investors may increase total demand or generate more-stable demand, influencing bond pricing and liquidity in green covered bond series. Given the relatively small number of green covered bonds issued to date, we expect the demand for green covered bonds to continue to outstrip supply in the near term.

Green cover pools have largely comprised green mortgages. These types of green properties, whether new or refurbished, residential or commercial, offer significant potential to improve energy efficiency since the building sector accounts for over 30% of all global energy-related CO2 emissions (Source: UN Environment, “Global Status Report 2017”).

However, the concept of a green asset extends beyond green mortgages. While there is no common definition of what constitutes a green asset, projects involving assets for generating renewable energy (solar, wind, hydro, landfill gas, geothermal, and biomass), sustainable transport methods (rail infrastructure and electric vehicles), buildings with green certifications, and water conservation equipment are generally considered green. Other assets such as efficiency improvements to fossil fuel-based power plants and nuclear plants in some cases qualify as green, but this categorization is sometimes disputed.

The prime focus for green cover pools has been on green mortgages. It is hard to say what proportion of traditional covered bond mortgage assets are green, as issuers have previously had difficulty identifying the green loans they have already underwritten–both commercial and residential. The current set of green covered bonds use different eligibility criteria for green buildings, which range from financing or refinancing new energy-efficient buildings to refurbishing existing commercial or residential properties.

To identify green loans, banks use certain recognized building certifications, including Energy Performance Certificates (EPC), building codes, analysis from independent consultants, and standards such as the Building Research Establishment Environmental Assessment Method (BREAM) or Leadership in Energy and Environmental Design (LEED). However, identification is made difficult by certification definitions and methodologies varying across countries, resulting in a lack of comparability. Additionally, exacerbating these issues are challenges accessing the energy performance of buildings and EPCs due to privacy concerns and data access constraints in certain countries, which further limit banks’ abilities to differentiate their green mortgage lending.

The Energy Efficient Data Portal (EeDaPP), under the EeMAP initiative, is aiming to address this by developing a standardized European framework to capture technical and financial data related to mortgages on energy-efficient properties and to utilize this data to assess the correlation between energy efficiency and financial risk.

Covered bonds backed by public sector debt may offer an attractive source of green finance, particularly if political will supports the public sector (municipalities and regions) to playing larger role in encouraging green investment. Issuers of public sector covered bonds could use their loyal investor base to offer attractive funding for future public sector green projects such as renewable energy-generating installations on public sector facilities or funding for other green infrastructure.

Traditional cover pools consist of a mix of green and brown assets of different maturities. The dynamic nature of cover pools makes the documentation of the use of proceeds a key focus for green covered bond investors to ensure the assets backing the green covered bond remains green. Green covered bonds are associated with a sub-pool of the cover pool that is made entirely of green assets and relies on these assets for the green ranking. To our knowledge, there is currently no cover pool consisting entirely of green assets. Credit ratings consider all assets in the issuer’s cover pool, and assign the same rating to all covered bonds issued from a cover pool program. While green covered bonds encourage green investments and specific issuances are backed by sub-pools that are entirely green, cover bond programs may be relying on brown assets for the necessary credit enhancement for the assigned credit rating.

In an effort to expand the covered bond setup for alternative green assets, legislative reviews are underway to broaden covered bond issuance beyond the existing framework–which focuses mainly on mortgages and public sector lending–to new asset classes, such as renewable energy. A notable example is the Luxembourg covered bond law to finance renewable energy infrastructure loans.

Our ratings criteria (see “Methodology And Assumptions: Assessing Pools Of European Residential Loans,” published Aug. 4, 2017) make no direct references to green factors for the assessment of credit risk, and a green borrower profile is unlikely to mitigate credit fundamentals such as unemployment, divorce rates, and death. In addition, the limited availability of historical performance data has provided no evidence of lower risk and therefore has not allowed us to make a green adjustment to other credit factors in our criteria.

Our residential and commercial credit criteria do specify factors that may already indirectly consider the impact of green borrowers and collateral on overall credit performance. One such factor is property valuations, which drive loan-to-value adjustments in our criteria. If green attributes lead to higher valuations, the result is credit-positive. In our opinion, valuations should only reflect green attributes if they offer a permanent improvement to the value of the property.

For residential borrowers, affordability at origination (a key indicator of propensity to default), the type of loan amortization, and general underwriting standards are examples of other credit factors that our criteria already consider and which may reflect a green impact or incentives for residential borrowers to take out a green mortgage.

We rank green quality using our Green Evaluation tool, which we developed to help investors understand the environmental contribution of financings (see “Green Evaluation Analytical Approach,” published April 26, 2017). The Green Evaluation is separate to a credit rating. It is an asset-level credential that assesses the relative environmental impact of a financing on a global basis. The assessment takes into account the net environmental benefits associated with the technology utilized over its full lifecycle relative to a local baseline and adjusted based on the sector’s overall contribution to avoiding and coping with climate change, combined with our review of governance and transparency protocols.

The overall score provides a benchmark of green quality that investors and issuers can use to understand not just whether a transaction is green or not, but how green it is relative to other financings globally. The final score is expressed on a scale of 1 to 100 and further broken into quartiles, where E1 (100-75) reflects the greatest positive environmental impact.

The Green Evaluation is applicable to any green financial instrument, including green covered bonds. When assessing a green covered bond pool, our Green Evaluation considers the net environmental attributes associated with the underlying assets that generate the cash flow in the cover pool based on the total collateral value. Our assessment can cover the entire pool or a portion of it. The green assessment is independent of the rating assessment and does not affect key credit rating measures such as the target credit enhancement for a given rating. For green buildings, which have served as the chief asset for green cover pools, we differentiate the assets on the basis of whether they are new buildings or a refurbishments. Moreover, our analysis considers the type of building–residential or commercial–and the building’s location to estimate the net benefits associated with each of the underlying assets.

The Green Evaluation is a point-in-time assessment and captures the environmental impact at the time the evaluation is complete. For cover pools, which are dynamic in nature, we consider the transaction’s eligibility criteria to confirm that the proceeds will be reinvested in green assets and look for annual reporting that tracks proceeds allocation and the environmental impact of the pool. For an example of how we’ve applied our Green Evaluation to a securitization, see “Green Evaluation: Ygrene Energy Fund Inc.’s GoodGreen Series 2018-1 Notes,” published April 10, 2018.

We believe that transparency, governance, and credibility are critical elements in assigning environmental value to green investments. There is an ongoing and widespread debate concerning what qualifies as green for the purposes of a green bond, including green covered bonds, and whether there is a need for a set of standards to improve the integrity of the green bond market. Currently, there are a number of taxonomies globally that vary in terms of which assets they classify as green. This lack of standardization has prompted efforts to develop a common taxonomy for green finance, such as the European Union Action Plan for Sustainable Finance. However, investors’ individual philosophies and investment goals complicate this effort.

Rather than define what green means, our Green Evaluation captures the fact that country-specific standards may differ from industry-accepted taxonomies and that investor preferences may also vary. In our assessment, we refer to the issuer’s own definition of what constitutes a green use of proceeds, so long as we believe the project (or a discrete component of it) falls within the scope of our published approach. Importantly, we do not exclude technologies, but we differentiate between technologies that provide long-term systemic green solutions versus a reduction in environmental impact.

The green covered bond market is relatively new, fast-growing, and innovative. In such a burgeoning marketplace, there is a concern that green covered bonds might fall prey to greenwashing–in other words, that proceeds from green covered bonds will be misallocated to non-green projects.

The Green Bond Principles (GBPs) have become the established process guidelines that the majority of self-labeled green bond issuers use and that green investors around the world refer to (see “Green Evaluations And Transaction Alignment With The Green Bond Principles,” published on April 6, 2018). The GBPs encourage issuers to obtain an external review to confirm that the bonds align with the principles. S&P Global Ratings can provide such a second-party opinion, when requested, through our Green Evaluation.

We believe that an independent, second-party opinion reflecting alignment with the GBPs, including a detailed review of the transaction documentation, should help alleviate fears of greenwashing.

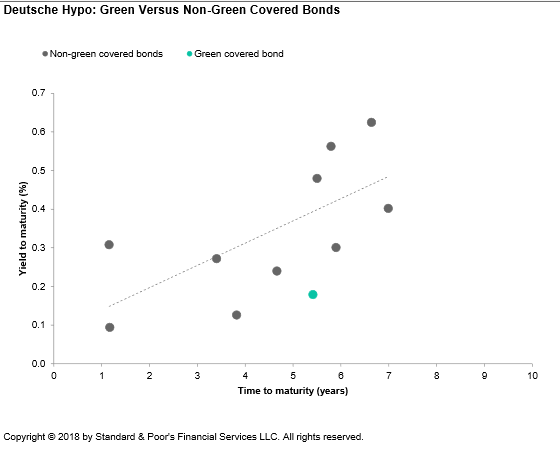

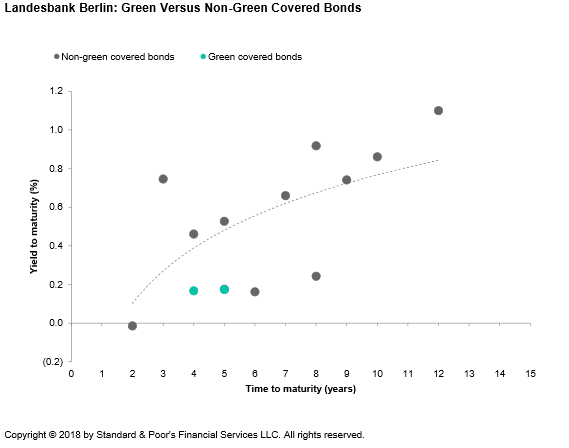

Across the green bond market, there have been a number of studies that point to a slight pricing advantage for issuers of green bonds, particularly in the corporate sector. To understand whether the value of “green” has had an effect on covered bond pricing, we compared the features and performance of green and non-green covered bonds issued by the same entity. We plotted the green covered bonds relative to each issuer’s interpolated yield curve based on mid yield to maturity at issuance. We chose issuers with a sufficient sample size to plot a curve, Deutsche Hypothekenbank and Landesbank Berlin, and we selected comparable bonds on the basis of similar credit characteristics.

We found that, for both banks, the green covered bonds priced inside the issuer’s interpolated yield curve. In the case of Deutsche Hypo this was by around 30 basis points (see charts below). The “greenium” (green premium paid by investors) detected is likely due to the mismatch in the demand-supply dynamics of the overall green bond market at present and to the large green covered bond issue size. In the case of Landesbank Berlin, its first green covered bond priced around 30 basis points tighter than its interpolated yield curve. We do however note that the second green bond issued by Landesbank Berlin priced only 0.2 basis points lower than a comparable non-green bond issued around the same time, suggesting that a second green issuance may not maintain a pricing differential or that prevailing market characteristics at issuance could have a greater impact on pricing than the green features of the covered bond, among other factors. In the corporate sector, the pricing advantage for green bonds relative to non-green bonds is around 2-3 basis points on average.

We note that this analysis is limited by the fact that only Landesbank Berlin has completed two green covered bond issuances. Indeed, the lack of data points and relevant comparable non-green bonds across green covered bond issuers makes interpretation challenging. Overall, we caution that these findings are based on a small sample size, which precludes us from being able to draw a firm conclusion over whether a “greenium” exists. It nonetheless provides additional case studies for green covered bond issuers.

The green covered bond market remains relatively small, but the growth potential is significant, in our opinion. We expect that green covered bond issuance will rise thanks to continued efforts to improve the identification of the green assets in bank lending, legislative initiatives to improve transparency and disclosure around green lending, and the expansion of the covered bond model to new asset classes. Some market participants believe that investor demand for green issuance could help compensate for some of the effect of the slow but sure exit of the European Central Bank from the covered bonds market.

As the market becomes more sophisticated, we anticipate that investors will increasingly look to assess green covered bond issuances not only for credit risk, but also for their relative environmental contribution.

To read the full article, click here

Established in 1967, the European Mortgage Federation (EMF) is the voice of the European mortgage industry on the retail side of the business, representing the interests of mortgage lenders at European level.